VIP Call Girls Service Cuttack Aishwarya 8250192130 Independent Escort Servic...

User research

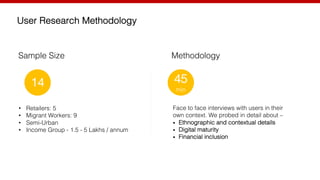

1. 14

User Research Methodology

• Retailers: 5

• Migrant Workers: 9

• Semi-Urban

• Income Group - 1.5 - 5 Lakhs / annum

Face to face interviews with users in their

own context. We probed in detail about –

• Ethnographic and contextual details

• Digital maturity

• Financial inclusion

Sample Size Methodology

45

min

3. End User (Migrant Worker)

Almost all users had

access to a bank

account in their

village

Most users did not

own the bank

account

Most users do not

know how to

operate an account

Banking

Cash is very often

stored in a safe

place at home

Informal and Inter-

personal borrowing

& repaying is a

norm

There is a general

trust in the bank,

but no first-hand

experience

Trust

4. End User (Migrant Worker)

ABPB’s

competition

seems to be with

“cash” rather

than banks

It was generally

observed that

there is a “low

motivation” for

creating and

managing a bank

account.

Group financial

schemes are

trusted more

than ‘Chit funds’

or ‘Loan

schemes’

From the study, 2

users (women)

did not even care

about starting a

bank account

Younger

generation, of

course, was

more savvy.

It was observed

that 80% of users

used feature

phones

They consume

entertainment

content like

music and

videos

Banking

Maturity

90% of usage is

to make &

receive voice

calls

Mobile

Usage

5. Pictures from field research:

Getting deeper insights from Retailers’ business

7. Retailer/Agent

Brand influences Working methods

• Although there is no

single service provider

that dominates the

market, 2 out of 4

retailers said that Idea

sold better than the

other service providers

and were pushing Idea.

• 50% retailers used

phone recharge, which

they felt was the easiest

and fastest method

• The retailers used a

third party application

for recharges. They

definitely see value in a

one stop solutions for all

their business needs

• Nobody reported facing

any problems in the

KYC process for their

customers

Banking Service

Experience

Effort vs. Revenue

• None of the retailers had

any experience of

selling banking /

financial products

• For the retailer segment,

the prime motivating

factor is to expand their

business, with minimum

effort and capital

8. Why do they use 3rd party applications for recharges & money transfer?

“The earlier process was more cumbersome, I

had to keep money for individual operators in

their respective e-wallets which all had minimum

top-up requirements, they were done by the

distributors of the operator who used to travel to

my place and so the days they didn’t come I

couldn’t recharge, I also had some friction with

them. My current service provider has only one

minimum top-up limit, I visit their center instead of

them coming to my place and so I feels my

dependency is lesser.“

9. Matching Need with Capabilities

I want a single window from where I can

do recharges, banking, on boarding

customers, cross selling banking

products etc

Offers a single window recharge process

for customers. Its a no brainer that it will

be for retailers as well.

11. Total Registered Customers

(Mn)

8 2.1 122

Total Active Customers (Mn) 2.4 0.33 70

Average Transaction Value (Mn) 200-400 200-500 200-600

USP Good deals and incentives

Large urban merchant Base

Strategic Tie-ups with GoI

(MNREGA)

Facility of Cash-out through

agent network

Large urban, semi-urban & rural

merchant base

Simple UX

Attractive deals

Marketplace

Payment Gateway

Large merchant base

Customer Segments Urban Urban

Semi-urban

Rural

Urban

Overview

14. Pushpa

Kumari

Flower seller

35

Married

Chennai

NEEDS

• Receiving/sending money from her family in

an easy manner without any middlemen

• Tracking and managing her day-to-day

expenses

• Saving her earnings for the future of her two

children, their education and marriages

• Not have to borrow money in emergencies

PAIN POINTS

• Unable to trust easily

• Lack of financial know-how

• Inconsistency in savings

• Inability to perform electronic

financial transactions independently

• Safe guarding the secret savings

• Effort in accessing financial services

MOTIVATIONS

• Safety of her finances

• Saving to tide over a rainy day

Financial awareness

Digital comfort

Life stage

“Only flower in hand, no money!”

Hard working Not a financial decision makerBelieves in integrated community living

15. Financial Behavior - Pushpa

Saving behavior No loans taken No insurance

88% 47% 53%

Source: www.finclusion.org

16. Crowdfunding

Instant Account Activation

Upliftment through 3rd Party Tie-Ups

Assisted Engagement

Door Step Banking

Uberization of Agents

Group SavingFingerprint Authentication

Savings

Loans

Insuranceicro

18. “I wish I had ten hands!”

NEEDS

• Quick and easy management of documents

• Synergy between various tasks

• Grow his business, increasing product line

• To be well informed so that he can earn the

trust of his customer

• Maintaining his reputation in his community

PAIN POINTS

• System outages

• Handling liquid cash

• Handling the shop alone

• Educating the customers

• Missing out on family time

• Documenting KYC is a hassle

• Afraid of dealing with local

authorities

MOTIVATIONS

• Incentives from the providers

• Any service that helps broaden his mind

and reduces effort

Financial awareness

Digital comfort

Life stage

Senthil

Kumar

Retailer

30

Married

Chennai

Influencer Multi-lingualMulti-tasker Entrepreneurial Action hub Hustler

Trusted by the community

19. Centralized Dashboard

Easy Digitized KYC

Single Window for all Business Needs

Financial Profile Management with ‘My Universe’

Gamification of Targets

Retailer Tool-Kit

Harnessing the Power of Community

Ability to Recharge Using Incentive Returns

20.

21. Would Pushpa be comfortable in opening an

account at Senthil’s shop & handing over her

life savings?

22. Would Senthil have the time to educate each

customer according to their needs?

25. Raghu

Nathan

Shop Assistant

21

Single

Chennai

NEEDS

• To get his sister married

• Plan for higher studies

• To buy an android mobile ASAP

• To save a little money “on the side” to live in

the city with dignity

• To be an important person in his peer group

• To take his girlfriend out for a movie once in

a while

PAINPOINTS

• Employer’s inconsistent

payment pattern

• Hardly able to save any money

for himself

• Getting the right opportunity

based on his education

MOTIVATIONS

• To be a responsible son

• To grow above his current status

quo

Financial awareness

Digital comfort

Life stage

“On my way to be a rockstar!”

Hard working HustlerAspirational Helper Experimental Street smart

Quick learner Literate

27. Learning through Experience

Idea University

Customer Personalized Recommendations

Personalized Counselling

Incentive fed savings

Micro Loans as Learning Samples

Assisted Mobile Banking Agent

Entertainment Channels with embedded Education

Literate

Helper

Street smart

Quick learner