Download to read offline

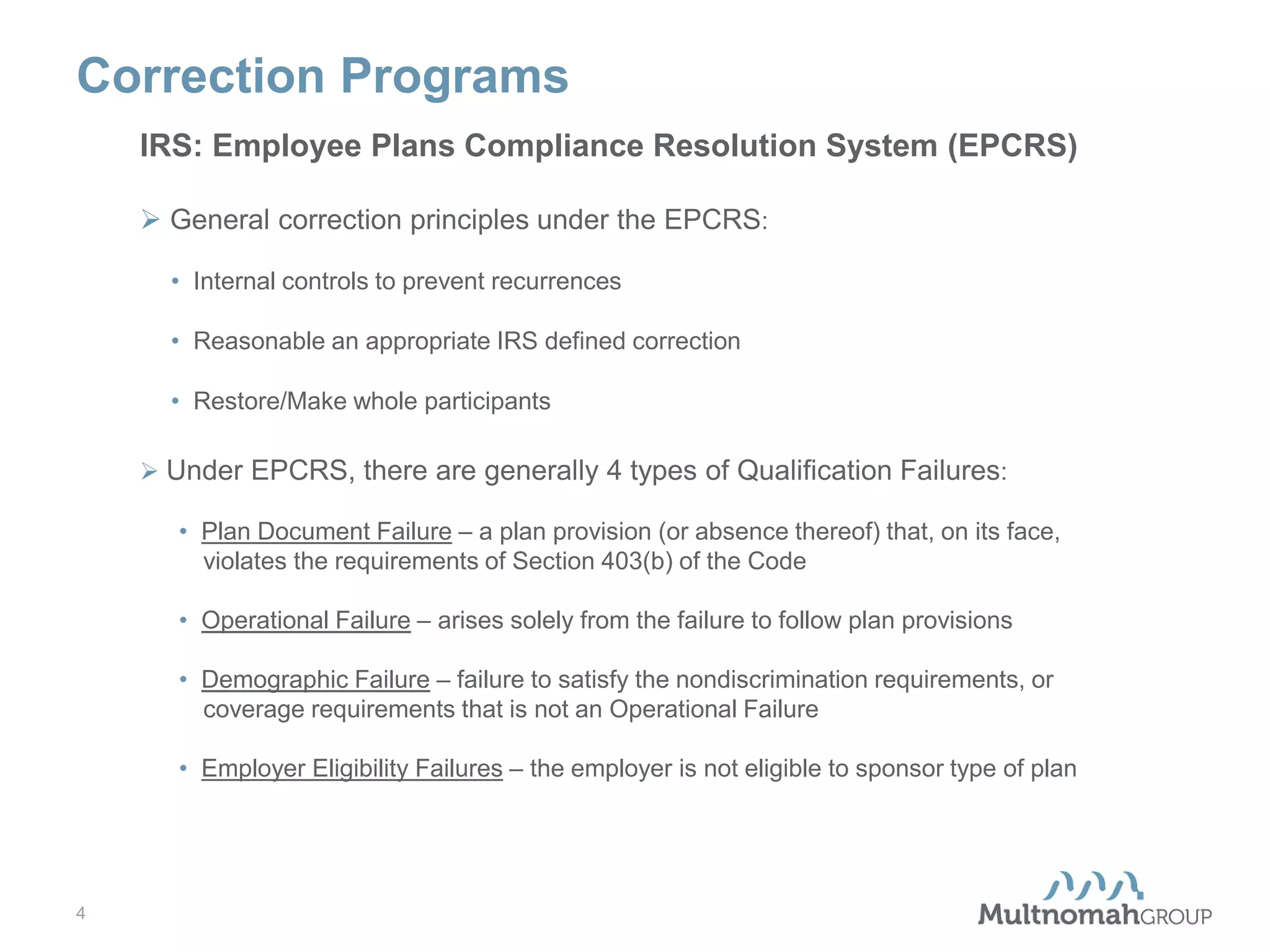

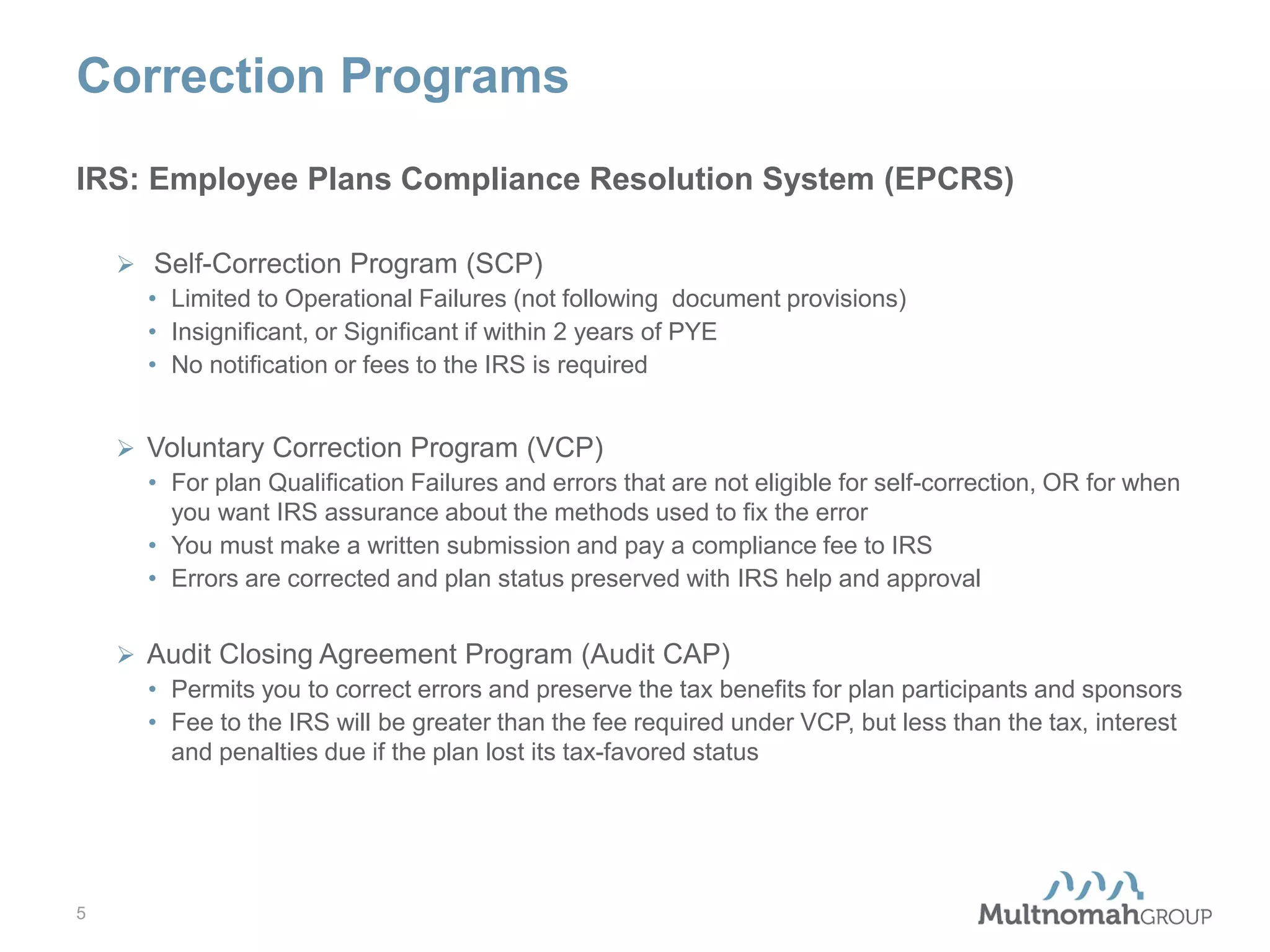

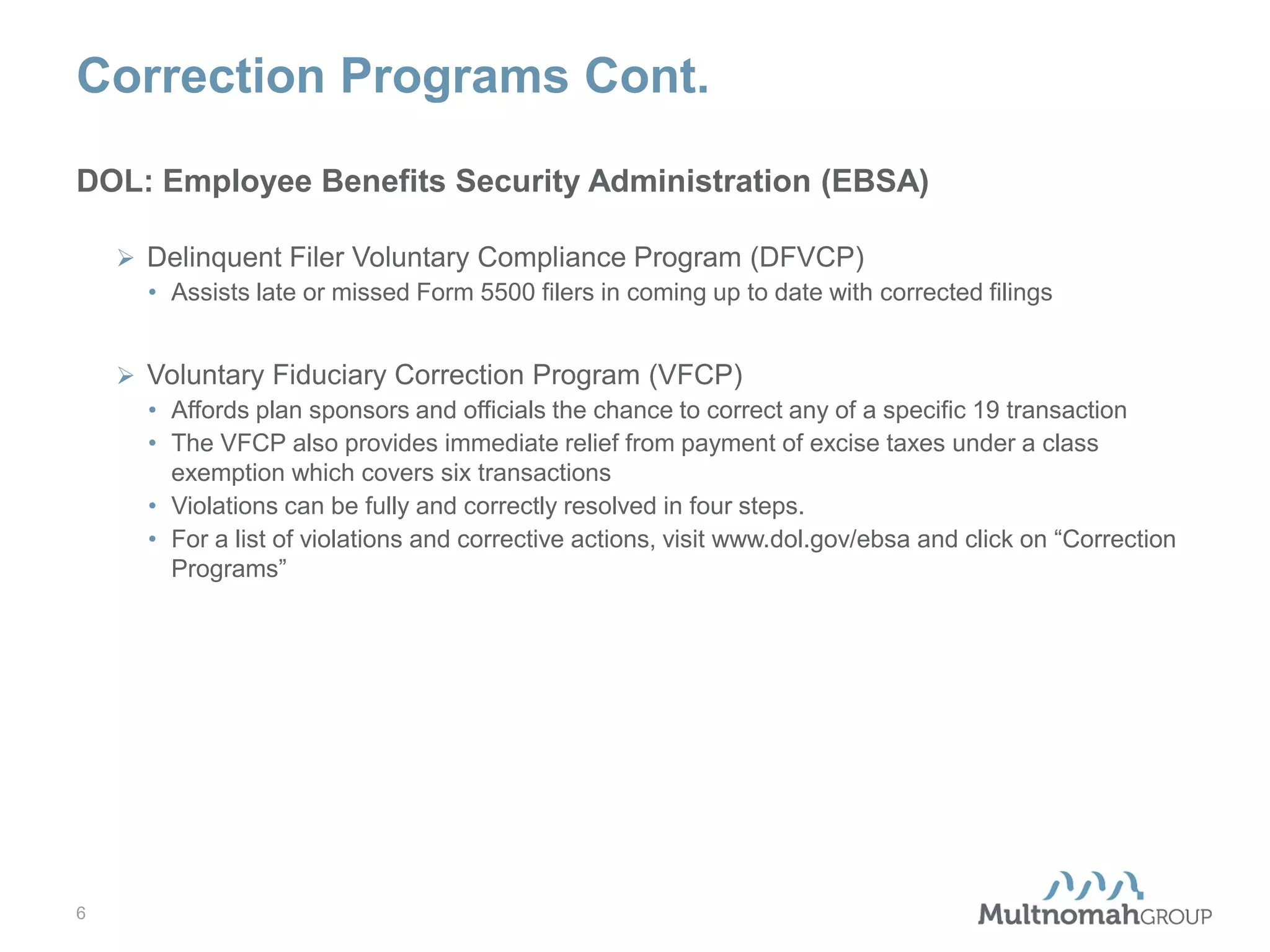

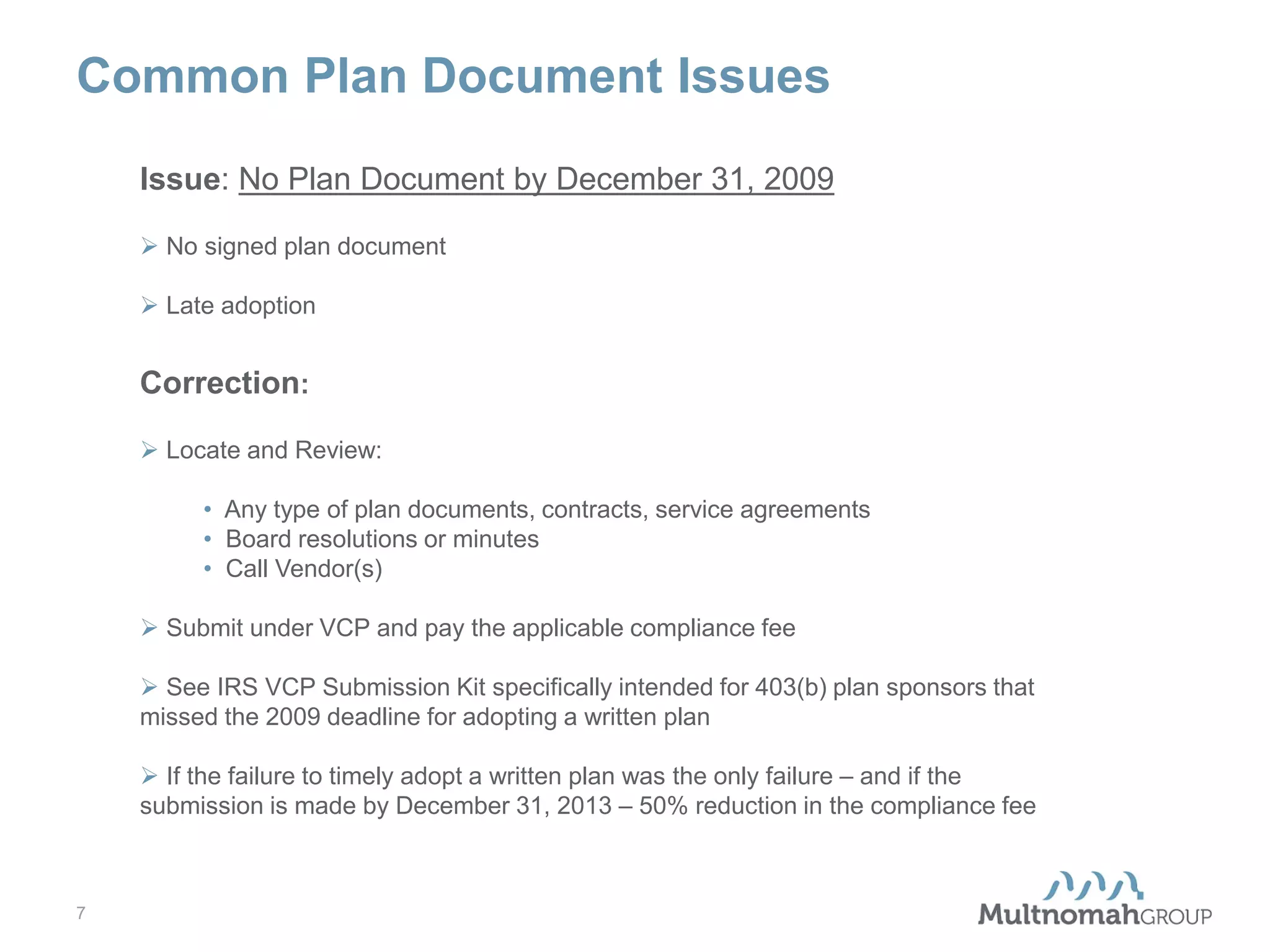

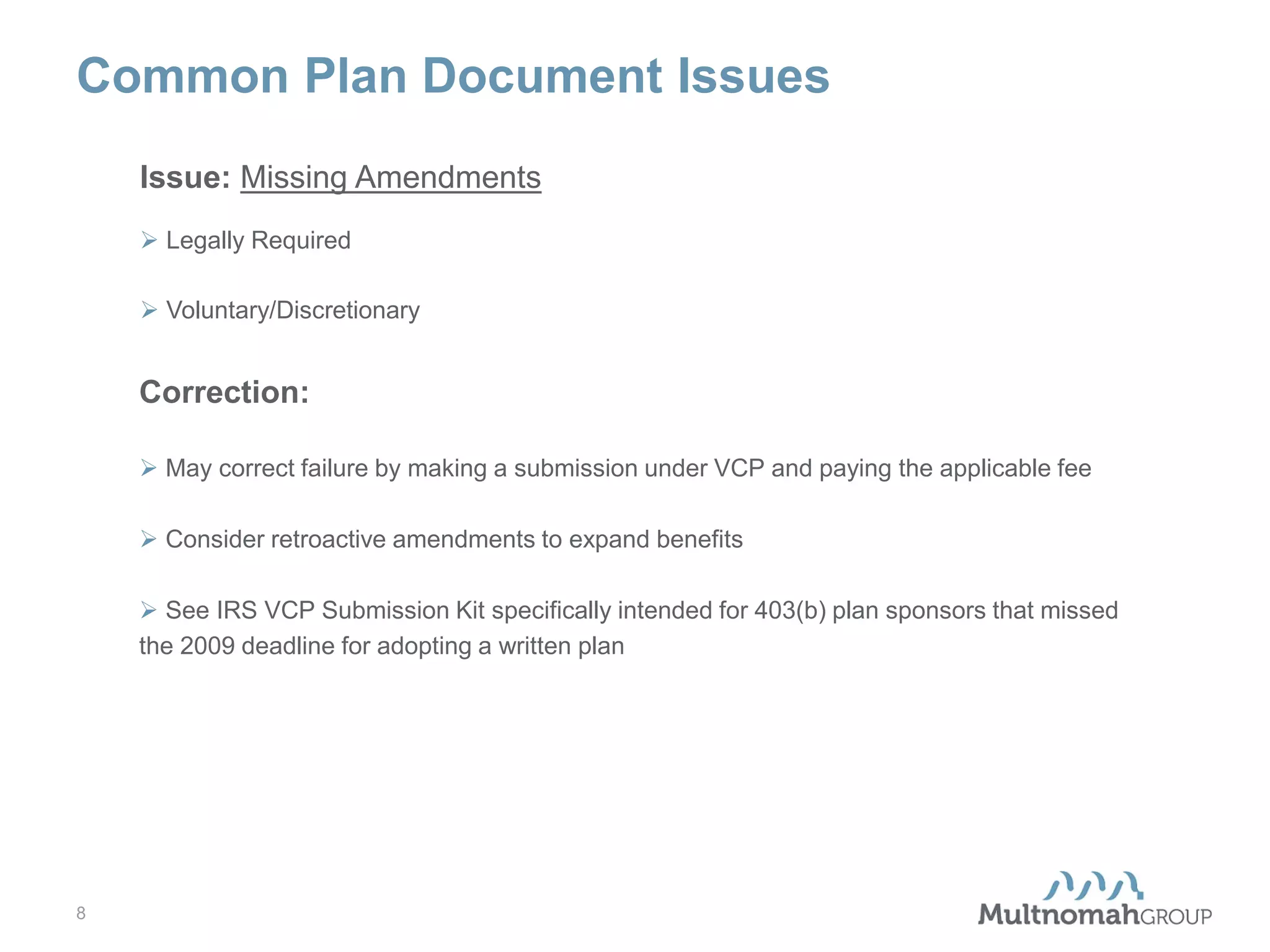

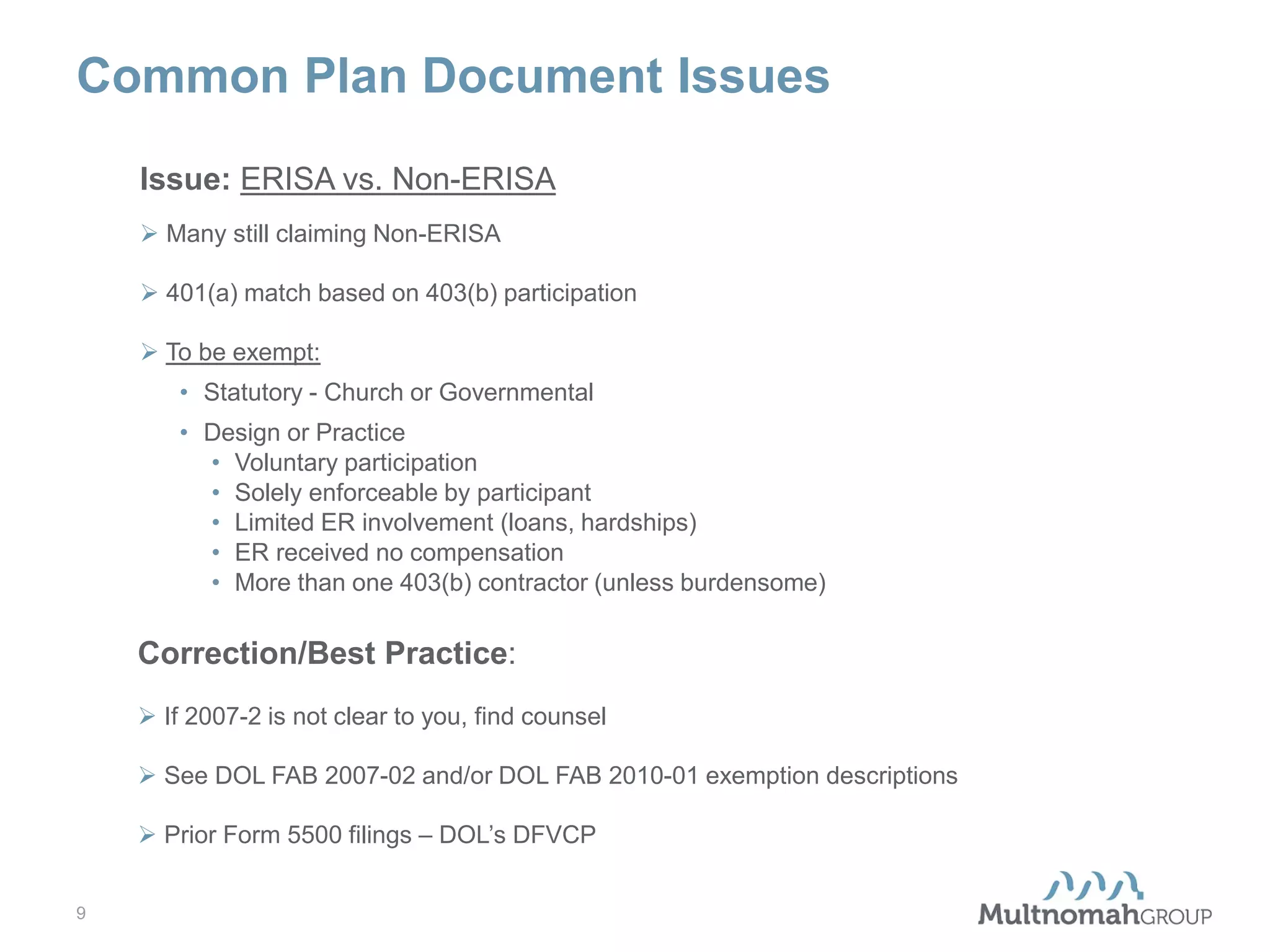

This document provides an overview and agenda for a presentation on common 403(b) plan compliance issues and solutions. It begins with introductions of the presenter and his background and experience. It then outlines the IRS and DOL voluntary correction programs that can be used to resolve plan failures. The majority of the document details frequent plan document issues, operational errors, and governance problems that 403(b) plans encounter. It provides examples and recommends best practices for correction.