1) The IMF faces many challenges as global economic and political power shifts, including rising populism, protectionism, and great power rivalry. It must adapt to remain relevant.

2) Key changes needed are rebalancing voting shares to reflect economic weights, increasing financial resources, and making the top leadership truly global and merit-based.

3) Ultimately, the IMF relies on countries cooperating in a rules-based global system. If that cooperation breaks down, the IMF's role will be difficult to maintain.

arifanee.com is world's leading website on the hottest financial news, perspectives and behind the scenes stories. arifanees.com brings you insight and information to inspire and transform your paradigm by enriching your with the best of facts and the vision.

arifanees.com

Information-Inspiration-Transformation

arifanee.com is world's leading website on the hottest financial news, perspectives and behind the scenes stories. arifanees.com brings you insight and information to inspire and transform your paradigm by enriching your with the best of facts and the vision.

arifanees.com

Information-Inspiration-Transformation

This is a presentation on Worldwide Financial Crisis made by Vinod Thomas, Director-General & Senior Vice President at the Independent Evaluation Group, World Bank. In the presentation, Mr. Thomas describes the reasons for the recent financial crisis, highlights the extent of damages, and discusses policy responses to the crisis.

Covid19 Pandemic: Looming Global Recession and Impact on BangladeshMd. Tanzirul Amin

The following article was written by me, and was published in the Economic Trends section of the Keystone Quarterly Review (Volume-30) on July 30, 2020: https://lnkd.in/g9nGxzn

The article covers the effects of the Covid-19 Pandemic in the world economics, and the resulting impacts on the Bangladeshi economy. Various other economic aspects are covered, along with the alarming signs/symptoms of another "Great Global Recession".

Present study re-evaluates the inflation-targeting monetary framework in Canada with a broader perspective by analyzing its impact on the real economy, macroeconomy, and financial economy rather than typically the performance of the inflation rate alone. It establishes that under this framework: Canada’s real economy has seen lower rates of domestic investment and GDP growth besides higher rates of unemployment; macroeconomy has experienced low inflation by virtue of cheap imports, aggregate demand sustained with the unsustainable debt levels, and the economic structure overwhelmed by the asset economy. The study concludes that the ‘so-called’ healthy system of inflation targeting is meaningless in an unhealthy economy, especially when it is among the contributing factors. This re-evaluation exercise leads to the obvious question for the Canadian policy-makers: whether macroeconomic, financial, exchange rate, employment, industrial, or social stability is less important than price stability?

An afro arab spring - socio-political trajectories in stemming the tide of th...Costy Costantinos

The financial, economic and for many, the livelihood, crisis that erupted in 2008 showed a cliffy downward freefall of economic trajectories unheard of in recent memory. The outbreak of the financial crisis provoked a broad liquidation of investments, substantial loss in wealth worldwide, a tightening of lending conditions, and a widespread increase in uncertainty. Higher borrowing costs and tighter credit conditions, coupled with the increase in uncertainty provoked a global flight to quality, caused firms to cut back on investment expenditures, and households to delay purchases of big-ticket items. Unemployment is on the rise, bringing with it a substantial deterioration in conditions for the most vulnerable. The sharp rise in commodity prices eventually resulted in The Arab Spring

Financialization, Rentier Interests, and Central Bank PolicyConor McCabe

Financialization, Rentier Interests, and Central Bank Policy

Gerald Epstein

Department of Economics and Political Economy Research Institute (PERI)

University of Massachusetts, Amherst

December, 2001; this version, June, 2002

Monetary policy is an important public policy, but it is not the only one to stabilize our economy and reduce its business cycles. The leading central bank, the Federal Reserve of the U.S., has introduced, after the 2008 global financial crisis, new instruments and unusual facilities to implement its new innovative monetary policy. The financial world and mostly the social scientists watch as the Federal Open Market Committee (FOMC) decides on a target interest rate in the federal funds market for the next period. The framework that the FOMC uses to implement monetary policy has changed over the last twelve years and continues to evolve today. Here, we try to evaluate the new instruments and their “effectiveness”. Before the 2008 financial crisis, policymakers used one set of traditional instruments (tools) to achieve the target rate. However, several policy interventions, introduced soon after the crisis, drastically altered the landscape of the federal funds market and the traditional economic theory. This new and uncertain environment, with enormous reserves and even interest on reserves, necessitated a new set of instruments by the Fed for its monetary policy implementation. Lately, after seven years of zero interest rate, the FOMC began in December 2015 to increase the target rate and then, went back again to a lower one, but many questions arise. How did they evaluate the effectiveness of these new instruments? Is the current federal funds rate the appropriate one for our economic wellbeing? How efficient was so far this ZIR monetary policy after the latest global financial crisis? Why the Fed put all these burdens of its ‘innovated” new monetary policy to the poor taxpayers (bail out) and to the risk-averse depositors (bail in)? Is it possible for the Fed’s policy to prevent the future financial crises? The federal funds rate was very low and affected negatively the financial markets (bubbles were growing), the real rates of interest (it is negative for twelve years), and the deposit rates (they are closed to zero for twelve years). The redistribution of wealth of depositors and taxpayers continues, which means the true economic welfare is falling and a new global recession was in preparation, if the current unfair easy money policy will persist, ignoring the necessity of a prevention of financial crises. Then, it came as an unexpected plague the coronavirus pandemic, following with a new but, the worse in economic history global crisis (chaos).

This article aims to demonstrate that the world is heading towards recession followed by a global economic depression, as well as presenting the solutions to deal with this gigantic problem.

Coronavirus-hit markets brace for the worst economic consequencesTatianaApostolovich

The coronavirus outbreak is leading investors to plan for situations more serious than a recession.

The S&P 500 has declined by 29.5% in two months.

The Federal Reserve's action to cut interest rates has been perceived as a "total breakdown of confidence".

PIMCO’s global economic advisor has warned a global recession is a "foregone conclusion".

DESA News is an insider's look at the United Nations in the area of economic and social development policy. The newsletter is produced by the Communications and Information Management Service of the United Nations Department of Economic and Social Affairs in collaboration with DESA Divisions. DESA News is issued every month.

For more information: http://www.un.org/en/development/desa/newsletter/desanews/index.html

This paper takes a systematic look at the economic impact of the crisis that started in earnest in the fall of 2008 across countries and regions. Despite warnings of growing domestic and external imbalances in many countries years ahead of the crisis, the massive impact of the crisis came as a surprise to most. By correlating economic performance in the crisis with an extensive set of early warning, country insurance, and policy indicators, this paper provides some lessons on crisis prevention and management for the future. Although significant efforts have been made to develop robust early warnings systems, the paper shows the mixed success of some commonly analyzed indicators in predicting economic outcomes in this crisis. The only robust early warning indicator was increases in real estate prices while international reserves seem to have insured against the worst crisis outcomes on average. However, much work on building a robust early warning system remains and the analytical and empirical challenges in this area are substantial. The issues confronting early warning systems are also relevant to the more recent field of macro prudential supervision and regulation. Nevertheless, the cost of crises is massive and preventing future ones with better regulation, policies and supervision based on solid research must be a top priority among policy makers and academics alike.

This is a presentation on Worldwide Financial Crisis made by Vinod Thomas, Director-General & Senior Vice President at the Independent Evaluation Group, World Bank. In the presentation, Mr. Thomas describes the reasons for the recent financial crisis, highlights the extent of damages, and discusses policy responses to the crisis.

Covid19 Pandemic: Looming Global Recession and Impact on BangladeshMd. Tanzirul Amin

The following article was written by me, and was published in the Economic Trends section of the Keystone Quarterly Review (Volume-30) on July 30, 2020: https://lnkd.in/g9nGxzn

The article covers the effects of the Covid-19 Pandemic in the world economics, and the resulting impacts on the Bangladeshi economy. Various other economic aspects are covered, along with the alarming signs/symptoms of another "Great Global Recession".

Present study re-evaluates the inflation-targeting monetary framework in Canada with a broader perspective by analyzing its impact on the real economy, macroeconomy, and financial economy rather than typically the performance of the inflation rate alone. It establishes that under this framework: Canada’s real economy has seen lower rates of domestic investment and GDP growth besides higher rates of unemployment; macroeconomy has experienced low inflation by virtue of cheap imports, aggregate demand sustained with the unsustainable debt levels, and the economic structure overwhelmed by the asset economy. The study concludes that the ‘so-called’ healthy system of inflation targeting is meaningless in an unhealthy economy, especially when it is among the contributing factors. This re-evaluation exercise leads to the obvious question for the Canadian policy-makers: whether macroeconomic, financial, exchange rate, employment, industrial, or social stability is less important than price stability?

An afro arab spring - socio-political trajectories in stemming the tide of th...Costy Costantinos

The financial, economic and for many, the livelihood, crisis that erupted in 2008 showed a cliffy downward freefall of economic trajectories unheard of in recent memory. The outbreak of the financial crisis provoked a broad liquidation of investments, substantial loss in wealth worldwide, a tightening of lending conditions, and a widespread increase in uncertainty. Higher borrowing costs and tighter credit conditions, coupled with the increase in uncertainty provoked a global flight to quality, caused firms to cut back on investment expenditures, and households to delay purchases of big-ticket items. Unemployment is on the rise, bringing with it a substantial deterioration in conditions for the most vulnerable. The sharp rise in commodity prices eventually resulted in The Arab Spring

Financialization, Rentier Interests, and Central Bank PolicyConor McCabe

Financialization, Rentier Interests, and Central Bank Policy

Gerald Epstein

Department of Economics and Political Economy Research Institute (PERI)

University of Massachusetts, Amherst

December, 2001; this version, June, 2002

Monetary policy is an important public policy, but it is not the only one to stabilize our economy and reduce its business cycles. The leading central bank, the Federal Reserve of the U.S., has introduced, after the 2008 global financial crisis, new instruments and unusual facilities to implement its new innovative monetary policy. The financial world and mostly the social scientists watch as the Federal Open Market Committee (FOMC) decides on a target interest rate in the federal funds market for the next period. The framework that the FOMC uses to implement monetary policy has changed over the last twelve years and continues to evolve today. Here, we try to evaluate the new instruments and their “effectiveness”. Before the 2008 financial crisis, policymakers used one set of traditional instruments (tools) to achieve the target rate. However, several policy interventions, introduced soon after the crisis, drastically altered the landscape of the federal funds market and the traditional economic theory. This new and uncertain environment, with enormous reserves and even interest on reserves, necessitated a new set of instruments by the Fed for its monetary policy implementation. Lately, after seven years of zero interest rate, the FOMC began in December 2015 to increase the target rate and then, went back again to a lower one, but many questions arise. How did they evaluate the effectiveness of these new instruments? Is the current federal funds rate the appropriate one for our economic wellbeing? How efficient was so far this ZIR monetary policy after the latest global financial crisis? Why the Fed put all these burdens of its ‘innovated” new monetary policy to the poor taxpayers (bail out) and to the risk-averse depositors (bail in)? Is it possible for the Fed’s policy to prevent the future financial crises? The federal funds rate was very low and affected negatively the financial markets (bubbles were growing), the real rates of interest (it is negative for twelve years), and the deposit rates (they are closed to zero for twelve years). The redistribution of wealth of depositors and taxpayers continues, which means the true economic welfare is falling and a new global recession was in preparation, if the current unfair easy money policy will persist, ignoring the necessity of a prevention of financial crises. Then, it came as an unexpected plague the coronavirus pandemic, following with a new but, the worse in economic history global crisis (chaos).

This article aims to demonstrate that the world is heading towards recession followed by a global economic depression, as well as presenting the solutions to deal with this gigantic problem.

Coronavirus-hit markets brace for the worst economic consequencesTatianaApostolovich

The coronavirus outbreak is leading investors to plan for situations more serious than a recession.

The S&P 500 has declined by 29.5% in two months.

The Federal Reserve's action to cut interest rates has been perceived as a "total breakdown of confidence".

PIMCO’s global economic advisor has warned a global recession is a "foregone conclusion".

DESA News is an insider's look at the United Nations in the area of economic and social development policy. The newsletter is produced by the Communications and Information Management Service of the United Nations Department of Economic and Social Affairs in collaboration with DESA Divisions. DESA News is issued every month.

For more information: http://www.un.org/en/development/desa/newsletter/desanews/index.html

This paper takes a systematic look at the economic impact of the crisis that started in earnest in the fall of 2008 across countries and regions. Despite warnings of growing domestic and external imbalances in many countries years ahead of the crisis, the massive impact of the crisis came as a surprise to most. By correlating economic performance in the crisis with an extensive set of early warning, country insurance, and policy indicators, this paper provides some lessons on crisis prevention and management for the future. Although significant efforts have been made to develop robust early warnings systems, the paper shows the mixed success of some commonly analyzed indicators in predicting economic outcomes in this crisis. The only robust early warning indicator was increases in real estate prices while international reserves seem to have insured against the worst crisis outcomes on average. However, much work on building a robust early warning system remains and the analytical and empirical challenges in this area are substantial. The issues confronting early warning systems are also relevant to the more recent field of macro prudential supervision and regulation. Nevertheless, the cost of crises is massive and preventing future ones with better regulation, policies and supervision based on solid research must be a top priority among policy makers and academics alike.

Publication: RITES Journal July 2014

Organization: Rail India Technical and Economic Service (RITES)

Source: www.rites.com

Date: July 2014

Summary: RITES Ltd., Government of India Enterprise was established in 1974, under the aegis of Indian Railways. It publishes an annual journal and discusses topics of contemporary significance.

Note: Please visit www.compad.in for more information

IMF: Analysis of Policy Recommendations after the Global Financial CrisisUNDP Policy Centre

IMF policy recommendations are often criticised for being orthodox, restrictive and prociclycal in their policy recommendations for developing countries. The global financial and economic crisis has led the Fund to publish papers and organize conferences that show some rethinking on these positions. But, to which extent IMF recent willingness to rethinking has led to actual changes in its policy advice to the developing countries?

This new paper by the Brasilia-based International Policy Centre for Inclusive Growth (IPC-IG) analyses recent recommendations given by the IMF to 26 developing countries to assess whether this ‘change’ discourse has been translated into action in the field. Our analysis looked at the recommendations around exchange rate, inflation, fiscal consolidation, employment and social protection policies. It also covers the theoretical debate behind the policies recommended: the underlying arguments, the criticisms received and the IMF’s position.

AnsA) When financial markets stood on the verge of collapse in th.pdfsutharbharat59

Ans:

A) When financial markets stood on the verge of collapse in the summer of 2008, two of the

worlds most important central banks, the US Federal Reserve and the Bank of England, began

considering unorthodox policy measures. They turned to Quantitative Easing, or QE: injecting

money into the economy by purchasing assets from the private sector, in the hope of boosting

spending and staving off the threat of deflation. These were desperate measures for desperate

times.

With signs of a fragile economic recovery gathering enough momentum to reassure

policymakers in the US, the policy was expected to be wound down. But in a move that caught

commentators off guard, the Fed instead committed to continue with its existing level of asset

purchases. For the foreseeable future, at least, QE is here to stay. What began as a short-term

crisis measure has now become a key component of Anglo-American growth strategies. Its

important, then, to take stock of QE and the central role it has played within the Anglo-American

response to the financial crisis.

The way the Fed led the policy response to the financial crisis is important in two ways. First, it

reflects the extent to which the Anglo-American economies have become financialised: credit-

debt relations are pervasive throughout all facets of contemporary economic activity and there

has been a deepening, extension and deregulation of financial markets commensurate with this

development. In that context, with the increased competitiveness, scale and global integration of

financial markets intensifying the risk of financial instability, the crisis management capacities of

central banks have become increasingly important.

Second, central bank leadership of the policy response also reflects a key feature of neoliberal

political economy in practice. Despite all the rhetoric of free markets, competition and

deregulation that has been the mainstay of neoliberalism, there is a central contradiction at its

heart: neoliberalism has been extremely reliant upon the active interventions of central banks

within supposedly free markets.

The crisis has been warehoused on the expanding balance sheets of central banks, demonstrating

just how much scope for policy manoeuvre there is when governing elites want it. Government

debt and private assets, including toxic mortgage-backed securities, have been indefinitely

transferred onto central bank accounts. This strategy highlights the role of arbitrary accounting

processes, shaped by state institutions, at the heart of supposedly free market economies.

Given this room for manoeuvre, there is no doubt that a much more expansionary fiscal policy

and a progressive taxation system could have been implemented in response to the crisis, but that

response is foreclosed by the ideological confines of the prevailing neoliberal orthodoxy. Instead,

we have monetary expansion and fiscal austerity.

Incubated within the crisis conditions of the 1970s, the neoliberal revolution in the West.

MTBiz is for you if you are looking for contemporary information on business, economy and especially on banking industry of Bangladesh. You would also find periodical information on Global Economy and Commodity Markets.

Swedbank was founded in 1820, as Sweden’s first savings bank was established. Today, our heritage is visible in that we truly are a bank for each and every one and in that we still strive to contribute to a sustainable development of society and our environment. We are strongly committed to society as a whole and keen to help bring about a sustainable form of societal development. Our Swedish operations hold an ISO 14001 environmental certification, and environmental work is an integral part of our business activities.

As the global financial crisis entered its most dramatic phase, in the second half of 2008, the International Monetary Fund (IMF), many governments and several distinguished scholars advocated expansionary fiscal olicy as the second most effective tool (after monetary stimulus) to fight deep recession and deflation. Now, more than a year later, the previous excitement surrounding the supposed power of fiscal stimulus largely disappeared and instead has been replaced by ising concerns over the sustainability of public finances in many countries. Unfortunately, the previous enthusiasts of the active counter‐cyclical fiscal policy have not always realized the causality between the two.

Authored by: Marek Dąbrowski

Published in 2009

The world economy has twice before enjoyed a super-cycle. It may now be

experiencing its third super-cycle.

To put it in context, it is defined here as, “A period of historically high global growth,

lasting a generation or more, driven by increasing trade, high rates of investment,

urbanisation and technological innovation, characterised by the emergence of large,

new economies, first seen in high catch-up growth rates across the emerging world.”

The first super-cycle took place during the second half of the 19th century, from 1870

until 1913, the eve of the First World War. At that time, the world economy witnessed

a significant step-up in its rate of growth, rising 2.7% on average per annum in

volume, or real, terms. That was a full 1% higher than the average growth rate seen

during the previous half-century. America was the big gainer, moving from the fourthlargest

to the largest economy. The second super-cycle was after the Second World

War until the early 1970s. World growth averaged a huge 5% per annum, again in

real or inflation-adjusted terms. Japan and the Asian tigers saw the biggest gains

over this time. Japan, for instance, moved from 3% to 10% of the world economy.

The Economic and Social Council will hold its Special high-level meeting with the World Bank, International Monetary Fund, the World Trade Organization and the United Nations Conference on Trade and Development on 14 and 15 April at the United Nations Headquarters, New York. The overall theme of the meeting will be “Coherence, coordination and cooperation in the context of financing for sustainable development and the post-2015 development agenda”.

For more information:

http://www.un.org/esa/ffd/ecosoc/springmeetings/2014/index.htm

The European Unemployment Puzzle: implications from population agingGRAPE

We study the link between the evolving age structure of the working population and unemployment. We build a large new Keynesian OLG model with a realistic age structure, labor market frictions, sticky prices, and aggregate shocks. Once calibrated to the European economy, we quantify the extent to which demographic changes over the last three decades have contributed to the decline of the unemployment rate. Our findings yield important implications for the future evolution of unemployment given the anticipated further aging of the working population in Europe. We also quantify the implications for optimal monetary policy: lowering inflation volatility becomes less costly in terms of GDP and unemployment volatility, which hints that optimal monetary policy may be more hawkish in an aging society. Finally, our results also propose a partial reversal of the European-US unemployment puzzle due to the fact that the share of young workers is expected to remain robust in the US.

Empowering the Unbanked: The Vital Role of NBFCs in Promoting Financial Inclu...Vighnesh Shashtri

In India, financial inclusion remains a critical challenge, with a significant portion of the population still unbanked. Non-Banking Financial Companies (NBFCs) have emerged as key players in bridging this gap by providing financial services to those often overlooked by traditional banking institutions. This article delves into how NBFCs are fostering financial inclusion and empowering the unbanked.

how to sell pi coins effectively (from 50 - 100k pi)DOT TECH

Anywhere in the world, including Africa, America, and Europe, you can sell Pi Network Coins online and receive cash through online payment options.

Pi has not yet been launched on any exchange because we are currently using the confined Mainnet. The planned launch date for Pi is June 28, 2026.

Reselling to investors who want to hold until the mainnet launch in 2026 is currently the sole way to sell.

Consequently, right now. All you need to do is select the right pi network provider.

Who is a pi merchant?

An individual who buys coins from miners on the pi network and resells them to investors hoping to hang onto them until the mainnet is launched is known as a pi merchant.

debuts.

I'll provide you the Telegram username

@Pi_vendor_247

Turin Startup Ecosystem 2024 - Ricerca sulle Startup e il Sistema dell'Innov...Quotidiano Piemontese

Turin Startup Ecosystem 2024

Una ricerca de il Club degli Investitori, in collaborazione con ToTeM Torino Tech Map e con il supporto della ESCP Business School e di Growth Capital

Falcon stands out as a top-tier P2P Invoice Discounting platform in India, bridging esteemed blue-chip companies and eager investors. Our goal is to transform the investment landscape in India by establishing a comprehensive destination for borrowers and investors with diverse profiles and needs, all while minimizing risk. What sets Falcon apart is the elimination of intermediaries such as commercial banks and depository institutions, allowing investors to enjoy higher yields.

The secret way to sell pi coins effortlessly.DOT TECH

Well as we all know pi isn't launched yet. But you can still sell your pi coins effortlessly because some whales in China are interested in holding massive pi coins. And they are willing to pay good money for it. If you are interested in selling I will leave a contact for you. Just telegram this number below. I sold about 3000 pi coins to him and he paid me immediately.

Telegram: @Pi_vendor_247

Even tho Pi network is not listed on any exchange yet.

Buying/Selling or investing in pi network coins is highly possible through the help of vendors. You can buy from vendors[ buy directly from the pi network miners and resell it]. I will leave the telegram contact of my personal vendor.

@Pi_vendor_247

Currently pi network is not tradable on binance or any other exchange because we are still in the enclosed mainnet.

Right now the only way to sell pi coins is by trading with a verified merchant.

What is a pi merchant?

A pi merchant is someone verified by pi network team and allowed to barter pi coins for goods and services.

Since pi network is not doing any pre-sale The only way exchanges like binance/huobi or crypto whales can get pi is by buying from miners. And a merchant stands in between the exchanges and the miners.

I will leave the telegram contact of my personal pi merchant. I and my friends has traded more than 6000pi coins successfully

Tele-gram

@Pi_vendor_247

Falcon stands out as a top-tier P2P Invoice Discounting platform in India, bridging esteemed blue-chip companies and eager investors. Our goal is to transform the investment landscape in India by establishing a comprehensive destination for borrowers and investors with diverse profiles and needs, all while minimizing risk. What sets Falcon apart is the elimination of intermediaries such as commercial banks and depository institutions, allowing investors to enjoy higher yields.

how can I sell my pi coins for cash in a pi APPDOT TECH

You can't sell your pi coins in the pi network app. because it is not listed yet on any exchange.

The only way you can sell is by trading your pi coins with an investor (a person looking forward to hold massive amounts of pi coins before mainnet launch) .

You don't need to meet the investor directly all the trades are done with a pi vendor/merchant (a person that buys the pi coins from miners and resell it to investors)

I Will leave The telegram contact of my personal pi vendor, if you are finding a legitimate one.

@Pi_vendor_247

#pi network

#pi coins

#money

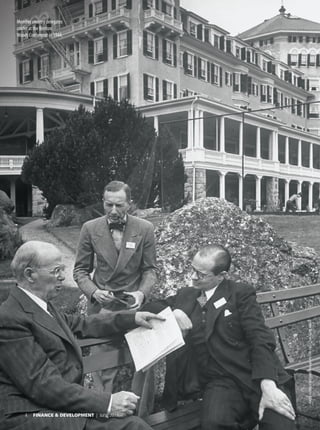

1. 4 FINANCE & DEVELOPMENT | June 2019

PHOTO:ALFREDEISENSTAEDT/THELIFEPICTURECOLLECTION/GETTYIMAGES

Member country delegates

confer at the Bretton

Woods Conference in 1944.

2. June 2019 | FINANCE & DEVELOPMENT 5

To meet future challenges, the IMF must have strong backing from its members

MartinWolf

THE IMF

T

he world is changing. The IMF is changing

with it. The question, however, is not only

how it needs to change if it is to remain rele-

vant. It is also whether the political environment will

allowittoremainrelevant.TheIMFisbuiltonacom-

mitment to cooperation among member countries.

That commitment is on the wane. But the countries

of the world might rediscover its importance. If so,

they will find the Fund an invaluable instrument.

The IMF cannot ensure that outcome. But it can,

and must, prepare for it. To its credit, it is doing so.

The world that surrounds the Fund has changed,

or is changing, in several crucial respects.

The first and most important change is a shift in

global economic, and therefore political, power. In

2000, advanced economies generated 57 percent

of global output, measured by purchasing power

parity. By 2024, according to IMF forecasts, that

share will fall to 37 percent. Meanwhile, China’s

share will jump to 21 percent from 7 percent, and

the rest of emerging Asia will account for 39 percent

of global output, compared with 14 percent for

the United States and 15 percent for the European

Union (see Chart 1).

The second transformation is an increase in great-

powerrivalryasrelationsdeterioratebetweenWestern

Today and Tomorrow

“Wehavecometorecognizethat

thewisestandmosteffectiveway

toprotectournationalinterestsis

throughinternationalcooperation—

thatistosay,throughunitedeffortfor

theattainmentofcommongoals.”

—USTreasury Secretary Henry Morgenthau, Jr.,

closing address at BrettonWoods Conference,

July 22, 1944

“Protectionwillleadtogreat

prosperityandstrength.”

—US President DonaldTrump,

inaugural address, January 20, 2017

“Foreverythingtostay

thesame,everything

mustchange.”

—GiuseppeTomasi di Lampedusa,

TheLeopard

3. 6 FINANCE & DEVELOPMENT | June 2019

powers and a rising China. The United States has

labeled China a “strategic competitor.” The European

Union, more narrowly, has called it an “economic

competitorinthepursuitoftechnologicalleadership.”

Either way, cooperation seems certain to become

more difficult.

The third change is a turn toward populist politics,

not least within advanced economies. One feature

of this populism is suspicion toward technocratic

expertise.Thisaffectsnotjustthecredibilityofdomes-

tic technocratic institutions, including independent

central banks and finance ministries, but also of inter-

national technocratic institutions, among which the

IMF is arguably the most significant.

The fourth change consists of the slowdown, or

even reversal, of globalization. This is markedly

true in some areas of finance, such as a dramatic

decline in the foreign claims of euro area banks

(Lund and others 2017). But it is also true in trade:

prior to the transatlantic financial crisis, the volume

of world trade grew almost twice as fast as world

output. Now trade and output are growing at about

the same rate. Recently we have even seen the

emergence of outright protectionism in the United

States (see Chart 2).

The fifth change involves technology.

Technological progress has been the driving force

of economic growth. But the role of the internet

and recent advances in artificial intelligence have

brought new vulnerabilities and upheavals, includ-

ing cyberattacks and massive shifts in labor markets.

The sixth change is an increase in financial fragility.

This has been gathering over decades. Substantial

efforts have been made to reduce this fragility, not

least by the IMF. But the ratio of debt to gross output

has increased, and debt has shifted from the private to

the public sector and to some degree from advanced

to emerging market economies. Further financial

disruptions are quite possible (see Chart 3).

The seventh change is the phenomenon dubbed

“secularstagnation”byHarvardUniversity’sLawrence

Summers at an IMF conference in 2013. Weak

demand, indicated by a combination of low inflation

and ultralow real and nominal interest rates, appears

to be structural and so is likely to persist. Room for

an effective conventional—or even conventionally

unconventional—policy response to a downturn

might be very limited.

The final change is the rising salience of climate

changeasapolicyissue.Thisislikelytohaveimportant

effectsondevelopmentstrategiesandmacroeconomic

policies in all countries, particularly in poorer and

more vulnerable ones.

All this creates a highly challenging environment

for the IMF, which has also been changing. Indeed,

its most durable characteristic has been its ability to

adapt to successive changes in the world. This partly

reflects the high quality of its staff and its usually

competent management.

Chart 1

Asia rising

Emerging Asia and China account for a growing share of global GDP, while the share

produced by advanced economies is dwindling.

Source: IMF, World Economic Outlook.

Note: Shares are calculated based on purchasing power parity.

0 20 40 60 80 100

Percent

European Union

United States

Other advanced

economies

China

India

Other emerging

Asia

Latin America and the Caribbean

Middle East, North Africa, Afghanistan,

and Pakistan

Other emerging economies

2024

2018

2009

2000

Wolf, 4/30/2019

Chart 2

Convergence

Before the global financial crisis, global trade was expanding at almost twice the pace

of GDP.Today, the growth rates are about the same.

(percent)

Source: IMF, World Economic Outlook.

Note: Figures are based on moving averages at the end of each period.

1994 97 2000 03 06 09 12 15 18 21

Five-year moving average growth of GDP

Five-year moving average growth of trade volume

Wolf, 4/30/2019

0

1

2

3

4

5

6

7

8

9

4. June 2019 | FINANCE & DEVELOPMENT 7

The IMF’s financial firepower must be

increased substantially, particularly in a

world of relatively free capital flows.

Yet the IMF is also handicapped by a limited capac-

ity to influence the actions either of countries with

robust balance of payments positions or of the United

States, the issuer of the world’s reserve currency, the

dollar. This is not a new issue: it was recognized—and

remained unresolved—at the Bretton Woods con-

ference in 1944 (Steil 2013). The Fund also makes

mistakes, not least because it is heavily influenced by

the conventional wisdom of professional economists

and powerful countries. It seriously underestimated

theperilsoffinancialliberalization,bothdomesticand

external. This was true despite the prescient warnings

of Raghuram Rajan, the IMF’s economic counsellor

from 2003 to 2006.

Learning from mistakes

It is, however, reasonable to expect the Fund to learn

from mistakes. It has done so. After the transatlantic

crisis, it reevaluated the impact of government spend-

ing cuts and tax increases on growth. The quality of its

surveillance of financial risks has also vastly improved

in its flagship Global Financial Stability Report and

World Economic Outlook and in work on member

countries. An important step has been its recognition

that liberalizing flows of capital across borders carries

risks as well as benefits.

No crisis has been more troublesome than the

one in the euro area. It put the IMF in the difficult

position of dealing with a central bank and countries

it could not control. The Fund worked with euro

area institutions on country programs that had some

successes but also significant shortcomings, notably

in the case of Greece. One result was to reform the

IMF’s lending framework for countries with high

sovereign debt and, above all, to end exemptions—in

the case of systemic crises—from mandatory debt

sustainability as a condition for Fund support.

The IMF’s stepped-up engagement with fragile

states is significant as well. It requires new and imag-

inative approaches to securing necessary political and

institutional transformation.

With these steps, the Fund has updated its old

agenda of maintaining macroeconomic stability.

But it has also taken up several new challenges,

including income and wealth inequality, gender

inequality, corruption, and climate change. These

challenges are outside the Fund’s historical areas of

competence. But they are vital in themselves and to

important constituencies in member countries, and

they have important macroeconomic implications.

Softening the IMF’s image can be helpful, especially

in a political environment that has become difficult

for international financial institutions. And, in some

respects, the Fund’s work has been vital, especially

on fossil fuel subsidies and the cost of corruption.

Challenges to come

If the world of cooperative globalization is to survive

and the IMF is to maintain its role within it, a great

dealmustchange.Someofthesechangesarewithinthe

Fund’scontrol.Otherscallforanewglobalconsensus.

A big internal task is to take on the intellectual

challengesofourunstableworldeconomy.Particularly

significant is the need to reconsider monetary, fiscal,

and structural policies, globally and within influential

countries, in the context of ultralow interest rates, low

inflation,largedebtoverhangs,andsecularstagnation.

Whatarepolicymakerstodowhenthenextdownturn

comes? How—if at all—might mass restructuring of

private or sovereign debt be managed? Is there any

validity in unorthodox perspectives such as “modern

IMF AT 75

Chart 3

Deeper in debt

Gross debt as a percentage of global GDP has increased, as has the share of public

debt.

(percent)

Source: Institute for International Finance.

1999 2002 05 08 11 14 17

350

300

250

200

150

100

50

0

Households Nonfinancial firms Financial firms Government

Wolf, 4/30/2019

5. 8 FINANCE & DEVELOPMENT | June 2019

monetary theory”? The Fund needs to become even

more deeply engaged in these topics if it is to prepare

for what lies ahead. But it must also get more closely

engaged in other difficult areas. The political econ-

omy of protectionism is one example. The impact of

artificial intelligence is another.

Above all, the IMF must remain relevant to all

its members. The only plausible way to do that is to

produce work of the highest intellectual quality and

integrity, especially in surveillance. This may irritate

the subjects of the Fund’s judgments from time to

time. But it will sustain the reputation and influence

of the IMF among its members. A question in this

context is whether it needs more staff expertise in

the politics of change: it is all very well to preach the

ending of subsidies, but how is that to be accepted?

Another question is whether more staff should reside

permanently in member countries. A detailed review

of the IMF’s way of working would make good sense.

The most important challenges for the IMF of

tomorroware,however,thosecreatedbyourchanging

world. Three stand out.

First, voting shares should be aligned with each

member’s economic importance. EU members

(including the United Kingdom) currently have 29.6

percent of votes; the United States, 16.5 percent;

Japan, 6.2 percent; and Canada, 2.2 percent. By

contrast, China has a mere 6.1 percent and India 2.6

percent. These figures are wildly out of keeping with

therelativeweightoftheseeconomies.True,advanced

economies still dominate global finance and issue all

thesignificantreservecurrencies.Butthiswillprobably

not last. If institutions such as the IMF are to remain

globally relevant, voting shares must be reweighted,

especially toward Asia, as Edwin Truman (2018) of

the Peterson Institute for International Economics

has persuasively argued. Otherwise, China will surely

establish its own version of the IMF, just as it has

already launched the Asian Infrastructure Investment

Bank and the New Development Bank.

Second, the IMF’s financial firepower must be

increased substantially, particularly in a world of rela-

tivelyfreecapitalflows.Itslendingcapacityiscurrently

just $1 trillion. Compare that with global foreign

exchange reserves of $11.4 trillion. The disparity

demonstrates the inadequacy of IMF resources and

the perceived costliness of gaining access to them. Of

course,thereismoralhazardassociatedwithexpanding

the safety net. But moral hazard does not eliminate

the case for insurance, fire brigades, or central banks.

The same applies to the Fund.

Finally, if the institution is to be credibly global,

its top job cannot be permanently left in the hands

of a European, however admirable some of those

Europeans have been. Global institutions need the

best global leaders. Those leaders should be chosen

not by a process of lowest-common-denominator

horse trading, but openly and transparently, with

candidates required to submit their platforms for the

future development of the institution.

Will to cooperate

As IMF Managing Director Christine Lagarde has

said,“The44nationsgatheringatBrettonWoodswere

determined to set a new course—based on mutual

trust and cooperation, on the principle that peace and

prosperity flow from the font of cooperation, on the

belief that the broad global interest trumps narrow

self-interest.” It is the marriage of professionalism

with this will to cooperate that has made the IMF a

cornerstone institution.

PerhapstheFund’smoststrikingqualityisitsadapt-

ability. It will surely need that adaptability in the

years to come. But even more, it will need a world

where the dominant powers believe in what the IMF

embodies:professionalism,multilateralism,andabove

all, cooperation. If this is not the world in which it

operates, it will struggle. In the end, the Fund is the

world’s servant. It can guide, but it cannot shape the

world. As the world goes, so will the IMF.

MARTINWOLFisassociateeditorandchiefeconomicscommen-

tatorattheFinancialTimes.

References:

Lund,Susan,EckartWindhagen,JamesManyika,PhilippHärle,JonathanWoetzel,andDiana

Goldshtein.2017.“TheNewDynamicsofFinancialGlobalization.”McKinseyGlobalInstitute,

NewYork.

Steil,Benn.2013.TheBattleofBrettonWoods:JohnMaynardKeynes,HarryDexterWhite,and

theMakingofaNewWorldOrder.Princeton,NJ:PrincetonUniversityPress.

Truman,EdwinM.2018.“IMFQuotaandGovernanceReformOnceAgain.”PIIEPolicyBrief,

PetersonInstituteforInternationalEconomics,Washington,DC.

IMF AT 75

It is the marriage of professionalism with this will to

cooperate that has made the IMF a cornerstone institution.