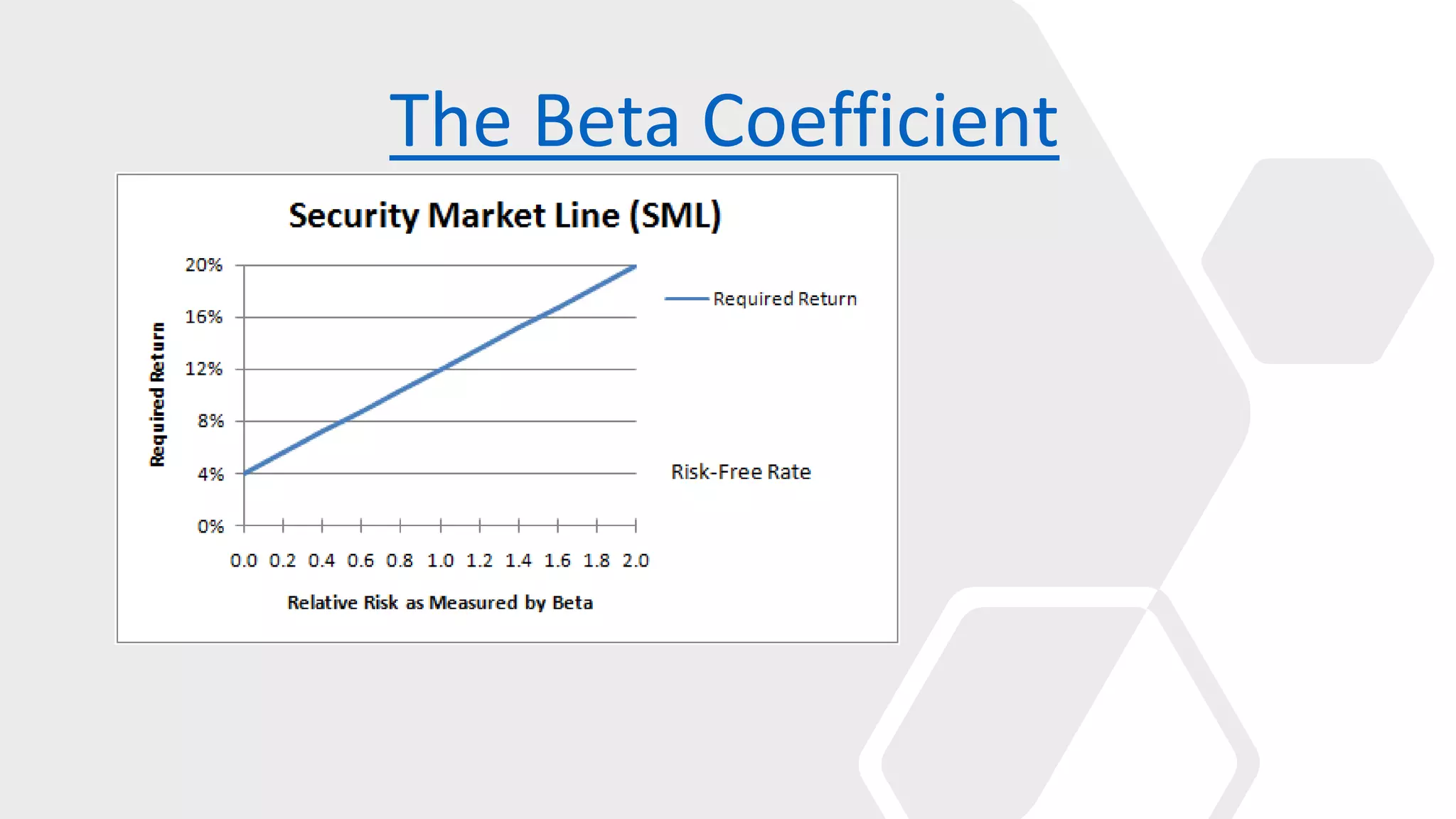

The beta coefficient measures the volatility and systematic risk of an individual stock relative to comparable stocks and the broader market, calculated through regression analysis. The beta formula involves covariance of the stock's returns with market returns divided by market variance, helping investors assess stock risk and its potential impact on their portfolio. A high beta indicates greater risk and potentially higher returns, while a low beta suggests less volatility.

What is Beta?

Thebeta coefficient is a form of measurement for volatile movement in an

individual stock, as well as systematic risk in comparison to comparable stocks or

the wider market.

Beta is a representation of the trajectory output of the slop calculated through

regression analysis of a particular stock vs sector vs wider market.

3.

Beta Formula (Howto calculate Beta)

Re = Return on individual stock

Rm = Return on the Market.

Covariance = how changes in a stock’s returns are related to changes in the

market’s returns.

Variance = how far the market’s data points spread out from their average

value.

𝐵𝑒𝑡𝑎 B = Coveriance Re, RM /Variance Rm

4.

Applying (B) Beta

Whena security experiences price movement ‘rubber banding’ or ‘swings’, beta

justifies this activity. You can measure Beta in three steps:

• Identify the target of the covariance;

• Divide the covariance against the variance of the market;

• Over defined period;

This calculation is used to measure if there was any movement of the stock against the

wider market, including the volatility-risk in comparison to its sector or wider market.

The target return used in the beta calculation must be related to the particular stock,

as an investor you would be trying to ascertain the risk of that particular stock and the

effect of that risk to your wider portfolio. If the stock has a strong deviation from the

market, then it would add a lot of risk to your portfolio but could also provide greater

return potential in comparison to lesser risk investments.

5.

Blue Gum GoogleDrive Blue Gum Website Blue Gum Google Site Blue Gum SlideShare