Implications of Tax Cuts on Commercial Real Estate

Avoid the Fiscal Cliff with Tax Planning Strategies

1. Destination: Plan

A Real Cliffhanger: Tax Planning

Strategies for 2013

DON’T TAKE THE FALL IF FEDERAL BUDGET GOES OVER THE FISCAL CLIFF

As 2012 comes to a close, Americans are dealing As a taxpayer and investor, how will this impending crisis

affect your investment goals? Importantly, what can you

with more uncertainty in their tax situation than

do to help:

in any time in recent history. Unless Congress l Minimize your tax obligations

can reach a compromise prior to year-end, the

l Maximize your after-tax return

U.S. economy will tumble over a “fiscal cliff,”

l And increase the likelihood of you reaching your

a term for the simultaneous increase in tax financial destination

rates and drastic cuts in federal spending. Unless Congress acts soon, nearly nine out of every 10

households will be paying higher taxes. Every income

group would see their taxes rise by at least 3.5%, with

high-income households taking an even bigger hit.*

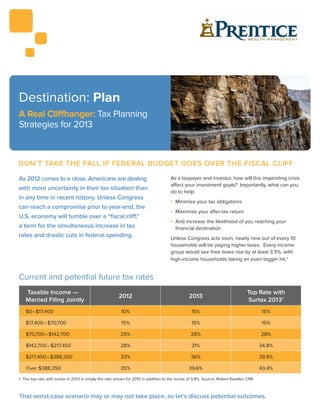

Current and potential future tax rates

Taxable Income — Top Rate with

2012 2013

Married Filing Jointly Surtax 2013 1

$0–$17,400 10% 15% 15%

$17,400–$70,700 15% 15% 15%

$70,700–$142,700 25% 28% 28%

$142,700–$217,450 28% 31% 34.8%

$217,450–$388,350 33% 36% 39.8%

Over $388,350 35% 39.6% 43.4%

1 The top rate with surtax in 2013 is simply the rate shown for 2013 in addition to the surtax of 3.8%. Source: Robert Keebler, CPA

That worst-case scenario may or may not take place, so let’s discuss potential outcomes.

2. Exploring likely outcomes you can do to mitigate its impact. First, for interest

If Bush-era income-tax cuts expire for tens of millions of income, you can convert taxable interest to municipal

Americans, billions of dollars of spending cuts will likely interest, which is tax exempt. That’s also the case with

take effect. It could go many ways, but the first possible dividend income, where we can reposition your holdings

outcome is the “over the cliff scenario,” where Congress to a tax-deferred or tax-free account.

takes no action and let’s current law stand. There are also options for investors planning to pass

Another option is Congress postponing action for six wealth to their heirs or their favorite charity. You may

months or more in what the Wall Street Journal called want to consider a Grantor Retained Annuity Trust,

the “kick the can down the road” scenario. A third – but which may be ideal for gifting wealth to your heirs,

welcome – scenario involves the President and Congress or a Charitable Remainder Trust, which is advantageous

coming up with both a long-term and short-term plan, for giving to charities. Both vehicles may offer significant

leaving many tax cuts in place and giving Congress time tax advantages.

to build bipartisan support for a permanent solution.

Unfortunately, we can’t predict what is going to happen,

Act now to manage against

so we’re advising clients to plan for the worst, which would uncertainty

mean one of the largest tax increases in US history.1 In summary, we don’t know what’s going to happen in

Washington over the next few months, so that’s why we

l Reinstatement of 36% and 39.6% tax brackets need to start now to make smart tax decisions. Don’t

l Long-term capital gain rate increased to 20% postpone tax planning until next April, when you’re up

l Itemized deduction limits re-instated against a deadline, or even year-end. There’s a lot of

uncertainty out there and it’s best if we try to get on top

l Reinstatement of $1 million exemption for estate tax

of it now.

(previously $5 million)

l Medicare tax rate increased for many households2 Finally, we’d like to offer our assistance. Our firm is

very familiar with the impact taxes can have on your

investments and can help you to achieve that goal of

It’s all about “asset location” maximizing your real return. We can sit down with you,

The important question is, what can we do about it? How

and/or your tax advisor and come up with a solid tax plan

can we minimize the damages taxes will have on our

– regardless of what Congress decides to do. Let’s start

investment portfolio? Remember, when investing, it’s not

working together now.

what you earn, but what you keep. Let’s take the steps

now to ensure you keep as much as possible. William J. Prentice II, AWMA, CFP®

President

First, investors should consider “asset location.” More

Prentice Wealth Managment, LLC

often than not, advisors are talking to clients about asset

110 Linden Oaks Drive Ste. F

allocation, or the mix of stocks and bonds in their

portfolios. Asset location refers to whether your assets

Rochester, NY 14625

are in a taxable, tax exempt or tax deferred investment wprentice@prenticewealth.com

vehicle. Investors should: www.prenticewealth.com

Office (585) 218-0001

l Consider maximizing contributions to retirement

Fax (585) 218-0097

plans & IRAs

l Consider investing in tax-exempt municipal bonds

l Consider whether Roth IRA is appropriate for you

Note from the chart on the front, there may be a new top Securities offered through Cadaret, Grant & Co. Inc. Member FINRA/SIPC.

Prentice Wealth Management, LLC and Cadaret, Grant & Co. Inc. are

rate for Medicare tax in 2013. However, there are things separate entities.

* Forbes.com, October 1, 2012

1

CBSNews.com, Unresolved fiscal cliff could raise taxes for 90 percent of U.S. families, Oct. 1, 2012

2

A

ll tax rate data from: AICPA, American Institute of Certified Public Accountants

This firm Prentice Wealth Managment, LLC does not provide tax advice. This content does not constitute tax,

legal or investing advice. Please note that (i) any discussion of U.S. tax matters contained in this

communication cannot be used by you for the purpose of avoiding tax penalties; (ii) this communication was

written to support the promotion or marketing of the matters addressed herein: and (iii) you should seek

advice based on your particular circumstances from an independent tax advisor.

121601