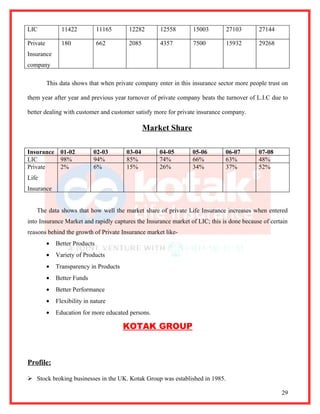

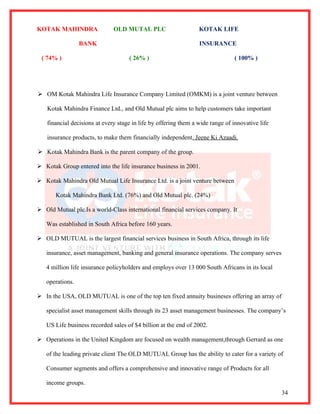

This document is a summer training project report submitted by Swati Gupta for partial fulfillment of an MBA degree. The report provides an acknowledgment, declaration, preface and table of contents. It then discusses India's financial markets and provides background on the insurance sector in India, including its history and regulations. The report also includes a company profile section on Kotak Mahindra Old Mutual Life Insurance Ltd where the training took place. It discusses various financial products like life insurance, mutual funds and equity markets. The report aims to do a comparative study of customer behavior toward these different options.