Downloaded 432 times

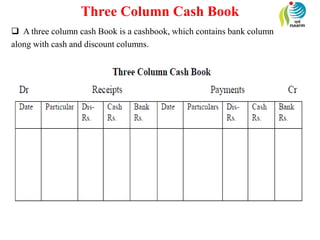

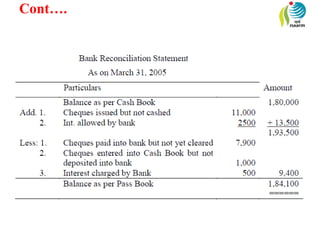

This document provides an overview of cash books, pass books, and bank reconciliation statements. It defines key terms like cash book, petty cash book, pass book, and bank reconciliation statement. It explains the different types of cash books (simple, two-column, three-column), and how to record transactions in each. It also outlines the process for preparing a bank reconciliation statement by identifying reconciling items that cause a difference between the cash book and pass book balances.