1. CREDIT

BEGINNERS

FOR

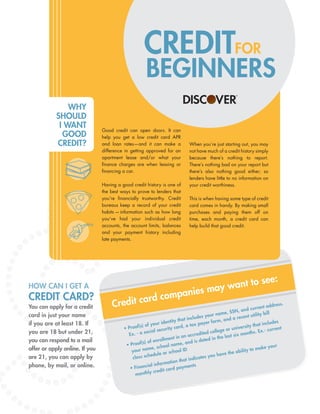

Good credit can open doors. It can

help you get a low credit card APR

and loan rates—and it can make a

difference in getting approved for an

apartment lease and/or what your

finance charges are when leasing or

financing a car.

Having a good credit history is one of

the best ways to prove to lenders that

you’re financially trustworthy. Credit

bureaus keep a record of your credit

habits —information such as how long

you’ve had your individual credit

accounts, the account limits, balances

and your payment history including

late payments.

When you’re just starting out, you may

not have much of a credit history simply

because there’s nothing to report.

There’s nothing bad on your report but

there’s also nothing good either; so

lenders have little to no information on

your credit worthiness.

This is when having some type of credit

card comes in handy. By making small

purchases and paying them off on

time, each month, a credit card can

help build that good credit.

CREDIT CARD?

HOW CAN I GET A

You can apply for a credit

card in just your name

if you are at least 18. If

you are 18 but under 21,

you can respond to a mail

offer or apply online. If you

are 21, you can apply by

phone, by mail, or online.

WHY

SHOULD

I WANT

GOOD

CREDIT?

• Proof(s) of your identity that includes your name, SSN, and current address.

Ex. - a social security card, a tax payer form, and a recent utility bill

• Proof(s) of enrollment in an accredited college or university that includes

your name, school name, and is dated in the last six months. Ex.- current

class schedule or school ID

• Financial information that indicates you have the ability to make your

monthly credit card payments

Credit card companies may want to see:

2. WHAT’S

AN APR?

APR stands for Annual Percentage

Rate. It’s an interest rate used to

calculate interest charges on

your balance. The APR may

vary depending on the type

of transaction.

If you pay your

monthly statement

balance in full every

billing period by the

due date, then you

may not have to pay

any interest charges

for purchases.

You typically cannot

avoid paying interest on

Balance Transfers and Cash

Advances. If you don’t pay

your balance in full every

month, you will pay an

interest charge based on

your APR.

Some credit cards offer a

promotional or introductory

APR—for instance, a

low or 0% APR for six

or nine months. After the

introductory time period is

up, you then pay a higher

APR which is typically

a variable purchase APR.

Before applying for a credit card,

here are a few things you need to know.

?WHAT SHOULD I

KNOW BEFORE

APPLYING FOR A

CREDIT CARD?

Most credit card companies use a calculation

method called the daily balance. Everyday

the company will start by figuring the Daily

Balance for each Transaction Category* and

multiply it by the Daily Interest Rate to get the

Daily Interest Charge.

The Daily Interest Charges then get added

up together to get the Total Interest Charges

for a billing period. See your cardmember

agreement for details on your card.

How are my

calculated?

INTEREST

CHARGES

Transaction

category*

APR

DAILY INTEREST RATE

DAILY INTEREST CHARGE

365

Days

Daily

Interest

Rate

÷ =

Daily

Balance

Daily

Interest

Rate

x

+

+

+

=

beginning

balance

new

transactions

Daily Interest

Charges

+new fees

other credits

adjustments

new

payments

*Transaction categories typically include standard Purchases, standard Cash Advances and different promotional balances, such

as Balance Transfers.

Daily

Interest

Charges

on previous

Daily Balances

3. ??????????????????????????????

??????????????????????????????

??????????????????????????????

??????????????????????????????

What’s

a credit

limit?

A credit limit is the maximum amount that you can

charge on your credit card. It’s typically based on your

creditworthiness. Your credit limit may increase as you

build a good record of paying your credit card bill on time.

Please review your credit card agreement for how your credit card works. Terms and conditions

may vary across companies and product types.

DiscoverStudentCenter.com

FIND OUT MORE

ABOUT CREDIT

for using a credit card?

Some credit cards have annual fees, some

don’t. However, you may get a late fee if

you miss a payment. Other fees may include

balance transfer fees, cash advance fees,

returned payment fees, returned check fees and

minimum interest charges. See your cardmember

agreement for details on your card.

ARE THERE

FEES

You may pay your entire balance shown on your credit card billing

statement at any time. Each billing period you must pay at least the

minimum payment due by the payment due date shown on your billing

statement to keep your account in good standing. To cut your interest

charges you can make more than the minimum payment.

With some companies, you can choose a due date that is more

convenient for you. This will be the same day every month.

WHEN DO I HAVE

TO MAKE A CREDIT

CARD PAYMENT?JANUARY

$