Download to read offline

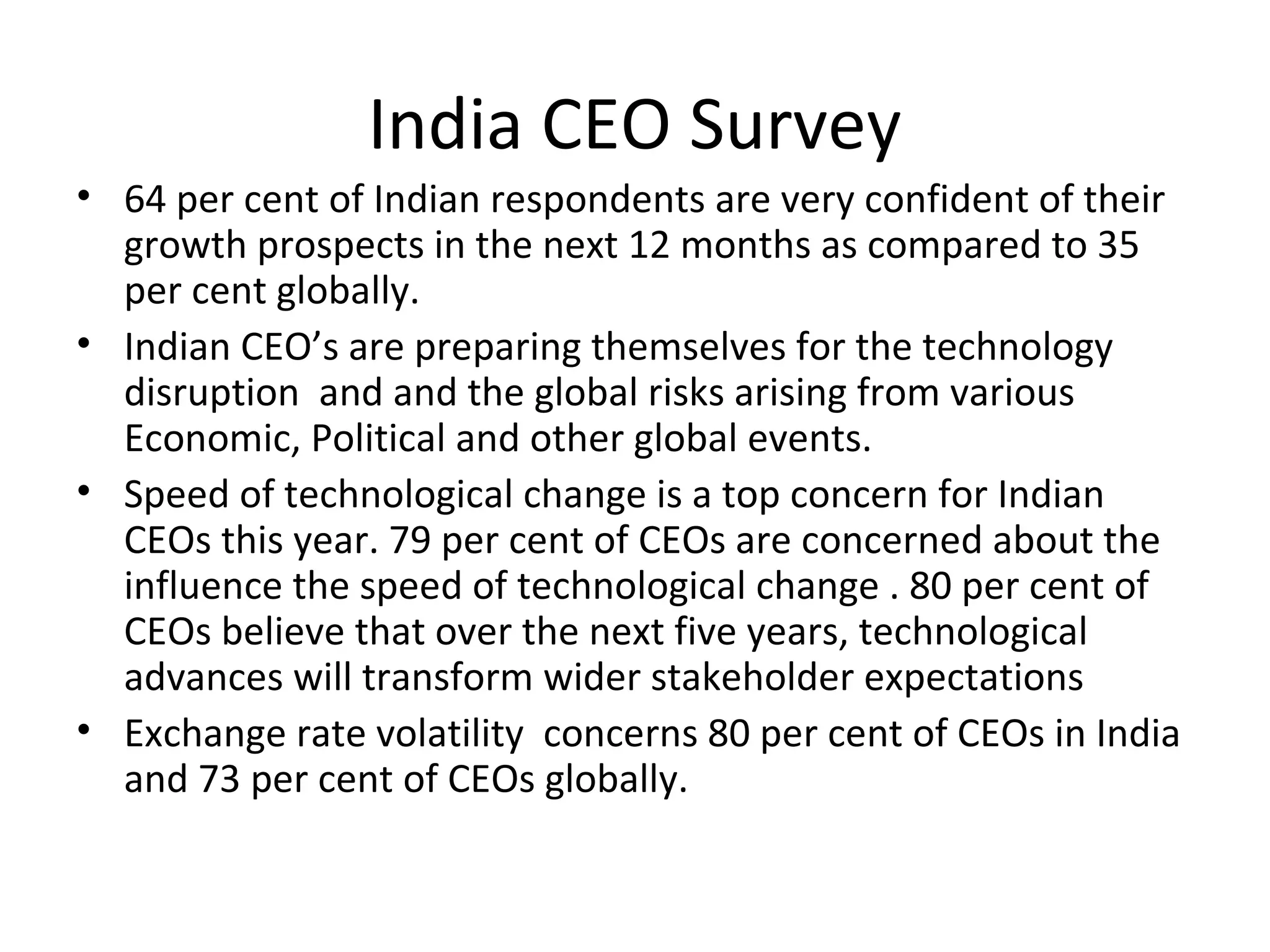

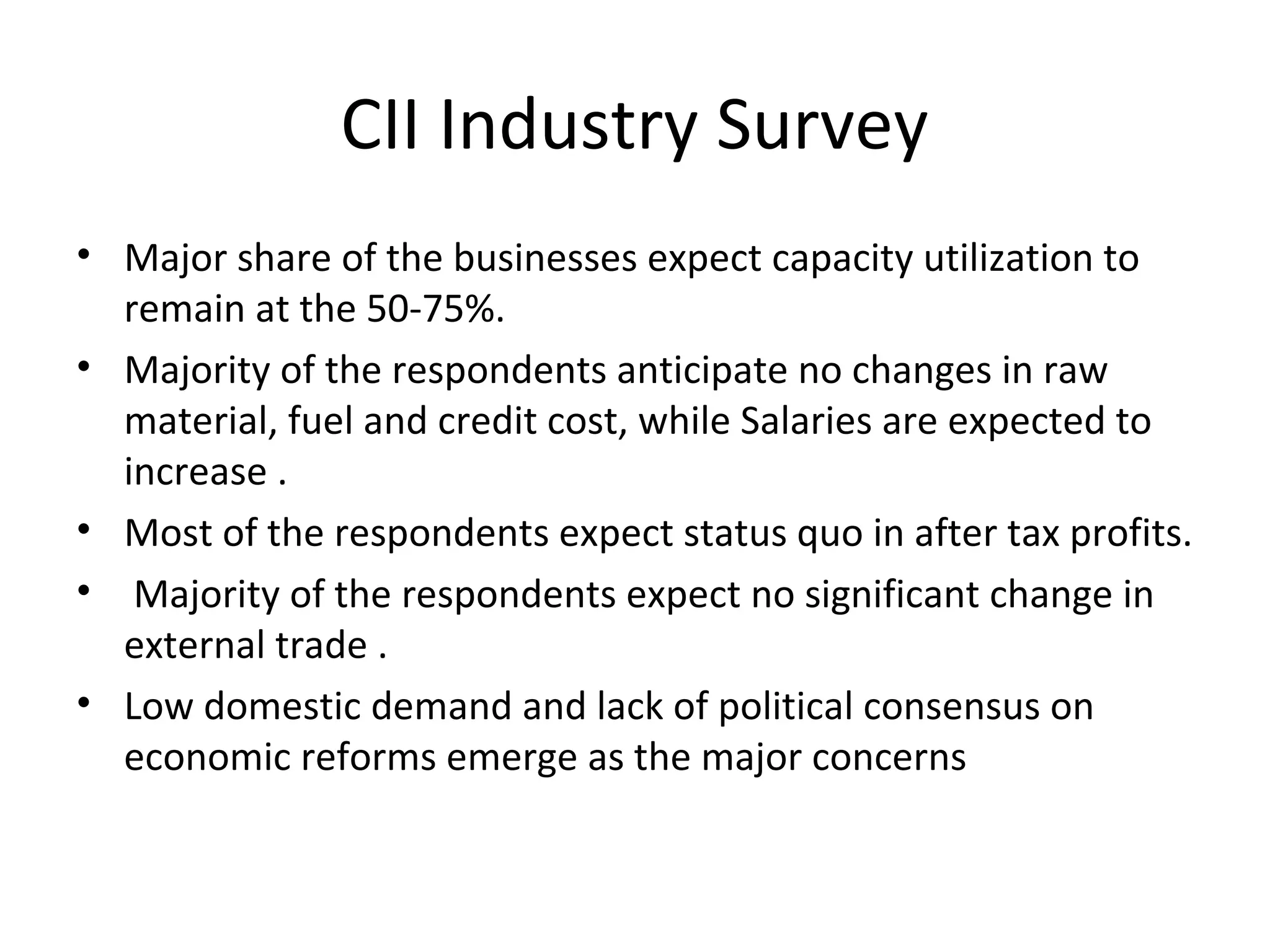

The document discusses strategies for companies in turbulent times based on various surveys. It notes that the global economic crisis of 2008 continues to have spill over effects. The world has become more volatile, uncertain, complex and ambiguous (VUCA). Risks have increased from multiple directions. Surveys find that customers and technology are top priorities for companies. Companies are focusing on their core competencies, reducing debt, converting costs to variable models, and exploring growth opportunities in emerging markets.