CERTIFICATE: MUNICIPAL FINANCIALMANAGEMENT

ID 48965 LEVEL 6 – 166 CREDITS

SKILLS PROGRAM 3:

LEARNER GUIDE

SAQA : 116342;116358

MUNICIPAL STRATEGIC PLANNING AND

IMPLEMENTATION

2 | P a g e

2.

3 | Pa g e

Learner Information:

Details Please Complete this Section

Name & Surname:

Organization:

Unit/Dept:

Facilitator Name:

Date Started:

Date of Completion:

Copyright

All rights reserved. The copyright of this document, its previous editions and any annexure

thereto, is protected and expressly reserved. No part of this document may be reproduced,

stored in a retrievable system, or transmitted, in any form or by any means, electronic,

mechanical, photocopying, recording or otherwise without the prior permission.

3.

4 | Pa g e

Key to Icons

The following icons may be used in this Learner Guide to indicate specific functions:

Books

This icon means that other books are available for further information on

a particular topic/subject.

References

This icon refers to any examples, handouts, checklists, etc…

Important

This icon represents important information related to a specific topic or

section of the guide.

Activities

This icon helps you to be prepared for the learning to follow or assist you

to demonstrate understanding of module content. Shows transference of

knowledge and skill.

Exercises

This icon represents any exercise to be completed on a specific topic at

home by you or in a group.

Tasks/Projects

An important aspect of the assessment process is proof of competence.

This can be achieved by observation or a portfolio of evidence should

be submitted in this regard.

4.

Workplace Activities

An importantaspect of learning is through workplace experience.

Activities with this icon can only be completed once a learner is in the

workplace

Tips

This icon indicates practical tips you can adopt in the future.

Notes

This icon represents important notes you must remember as part of the

learning process.

5 | P a g e

5.

Learner Guide Introduction

Aboutthe Learner

Guide…

This Learner Guide provides a comprehensive overview of the

MUNICIPAL STRATEGIC PLANNING AND IMPLEMENTATION, and forms part

of a series of Learner Guides that have been developed for

CERTIFICATE: MUNICIPAL FINANCIAL MANAGEMENT AT NQF LEVEL 6,

WORTH 166 CREDITS.

The series of Learner Guides are conceptualized in modular’s format

and developed for CERTIFICATE: MUNICIPAL FINANCIAL MANAGEMENT.

They are designed to improve the skills and knowledge of learners, and

thus enabling them to effectively and efficiently complete specific

tasks.

Learners are required to attend training workshops as a group or as

specified by their organization. These workshops are presented in

modules, and conducted by a qualified facilitator.

Purpose The purpose of this Learner Guide is to provide learners with the

necessary knowledge related to CERTIFICATE: MUNICIPAL FINANCIAL

MANAGEMENT.

Assessment Criteria The only way to establish whether a learner is competent and has

accomplished the specific outcomes is through an assessment process.

Assessment involves collecting and interpreting evidence about the

learner’s ability to perform a task.

This guide may include assessments in the form of activities,

assignments, tasks or projects, as well as workplace practical tasks.

Learners are required to perform tasks on the job to collect enough and

appropriate evidence for their portfolio of evidence, proof signed by

their supervisor that the tasks were performed successfully.

To qualify To qualify and receive credits towards the learning program, a

registered assessor will conduct an evaluation and assessment of the

learner’s portfolio of evidence and competency

Range of Learning This describes the situation and circumstance in which competence

must be demonstrated and the parameters in which learners operate

6 | P a g e

6.

Responsibility The responsibilityof learning rest with the learner, so:

Be proactive and ask questions,

Seek assistance and help from your facilitators, if required.

7 | P a g e

7.

88 | Pa g e

1

Contribute to the strategic planning

process in a South African municipality

Learning Unit

UNIT STANDARD NUMBER : 116358

LEVEL ON THE NQF : 6

CREDITS : 15

FIELD : Business, Commerce and Management Studies

SUB FIELD : Public Administration

PURPOSE:

This Unit Standard deals with the strategic planning process, which is specific for

municipal government, but includes competencies applicable to a range of

organisations, including private sector organisations.

Qualifying learners are able to:

Participate effectively in the strategic planning process within their municipality,

irrespective of their position in the organisation structure.

Impact on social and economic development through assisting municipal

organisations in planning better, which should lead to improved service

delivery.

LEARNING ASSUMED TO BE IN PLACE:

It is assumed that the Learners are competent in:

• Communication at Level 4.

• Mathematical Literacy at Level 4.

• Economics at Level 4.

8.

99 | Pa g e

SESSION 1:

Formulate vision and mission statements in a south African

municipality as required by the local government legislative

framework.

Learning Outcomes

The various role-players for consultation typically required in the formulation of

municipal 'vision' and 'mission' statements are identified for consultation.

A process is designed for formulating 'vision' and 'mission' statements including all

role-players and in accordance with relevant legislation.

Different municipal mission statements are evaluated in the context of the actual

service delivery programmes and evolving macro environment.

Programmes are formulated to carry out service delivery activities required to

support an already formulated mission statement.

1.1. Strategic planning

Strategic planning is a systematic process for identifying and implementing programs

that capitalize on the municipality’s strengths and weaknesses, while recognizing there

are external threats and opportunities that have an impact upon the municipality.

Quite simply, it provides the means for a municipality to chart a future it desires rather

than reacting to events as they unfold. It provides the opportunity for the municipality to

develop a vision of the desired future of the municipality with the participation from all

stakeholders. The process also includes steps to ensure the strategic plan remains

current, and responds and adapts to a changing environment.

There are seven basic steps in preparing a strategic plan, which are as follows:

1. Getting Organized

Striking a Strategic Planning Team

Setting Organizational Framework

Identifying Municipality’s Mandates

9.

1010 | Pa g

e

2. Clarifying Values and Mission

Stakeholder Analysis

10.

1111 | Pa g

e

Municipality’s Values

Municipality’s Mission Statement

3. Assessing the Situation

Situation Assessment

SWOT Analysis (strengths, weaknesses, opportunities and threats)

Identifying Strategic Issues

4. Strategic Plan

Formulate Strategies

Integrating Strategies to Strategic Plan

Municipality’s Vision Statement

Evaluation Process

Prepare Document.

5. Adopting the Strategic Plan

6. Implementation

Formulate Implementation Process

7. Strategic Issue Management

Reassess Strategies and Strategic Planning Process

There are five main benefits of conducting a strategic plan:

It promotes strategic thought and action.

It focuses attention to critical issues.

It enhances a municipality’s organizational responsiveness and performance.

Policy makers and decision makers are better able to fulfill their roles and

the team work of municipal staff is strengthened.

A strategic plan provides the ground work for a municipal business plan.

The Strategic Plan can take twelve to twenty working days spread over a six to twelve

month period, depending on the breadth and complexity of issues to be addressed. For

any municipality, this is a manageable and rewarding endeavor, as a review of many

successful municipalities will indicate; a strategic plan is the cornerstone to their success.

11.

1212 | Pa g

e

1.2. Articulating Mission and Vision

12.

1313 | Pa g

e

A mission statement is like an introductory paragraph: it lets the reader know where the

writer is going, and it also shows that the writer knows where he or she is going. Likewise,

a mission statement must communicate the essence of an organisation to the reader.

An organisation's ability to articulate its mission indicates its focus and purposefulness. A

mission statement typically describes an organisation in terms of it’s:

Purpose - why the organisation exists, and what it seeks to accomplish.

Business – the main method of activity through which the organisation tries to fulfill its

purpose.

Values – the principles and believes that guide an organisations members.

Whereas the mission statement summaries the what, how, and why of an organisations

work, a vision statement presents an image of what success will look like. For example,

the mission statement of the Support Centres of America is as follows:

The mission of the Support Centres of America is to increase the effectiveness of the non-

profit sector by providing management consulting, training and research. Their guiding

principles are: promote client independence, expand cultural proficiency, collaborate

with others, ensure our own competence, and act as one organisation

With mission and vision statements in hand, an organisation has taken an important step

towards creating a shared, coherent idea of what it is strategically planning for.

1.2. Who should be involved in the Strategic Planning Process?

The key decision makers in a municipality cannot prepare a strategic plan in a vacuum.

Rather the major stakeholders must be included in the discussions. This would include

customers (interested members of the public and interest groups), councillors and the

mayor or warden, municipal managers, employees and unions.

This overall balanced approach to forming a Strategic Planning Team is critical for its

success, and each municipality will have to strike the right balance to ensure all major

parties are involved. This provides for a collaborative and interactive process at all levels.

Consider the following

Leadership doesn’t stop at the top. Leadership at the top levels is important, but

leadership by employees in solving problems is equally important to contributing

to a successful organization.

13.

1414 | Pa g

e

Listen to your customers and stakeholders. What is really important to them? It

may not always be the same as what the managers and elected officials may

think.

Listen to your employees and unions. The employees have the historical

knowledge and experience at the day to day operations level. This information

and expertise can be very influential to obtaining achievable results from a

strategic plan.

With respect to unions, their mandate is to protect and forward the interests of their

membership. If union membership is significant in the municipality, their involvement may

be critical to the final success, as it ensures the employee’s interests are represented as

well as a “buy in” on the process and final results. This principle is especially critical in

achieving culture change within an organization.

The rationale for including a broad-based committee is two fold:

Those who are consulted about the plan will take a greater interest and may

adopt all or part of it as their own.

The plan will reflect a broader spectrum of viewpoints and a wider range of

resources if more people have an opportunity to contribute.

Integrated development planning

Integrated development planning is an approach to planning that is aimed at involving

the municipality and the community in finding the best solutions towards sustainable

development.

An Integrated Development Plan (IDP) is a super plan for an area that gives an overall

framework for development. It aims to co-ordinate the work of local and other spheres

of government in a coherent plan to improve the quality of life for all the people living in

an area. It takes into account the existing conditions and problems and resources

available for development.

Through Integrated Development Planning, which necessitates the involvement of all

relevant stakeholders, a municipality?

Identifies its key development priorities

Formulates a clear vision, mission and values

Formulates appropriate strategies

14.

1515 | Pa g

e

Develops the appropriate organisational structure and systems to realise the vision

and mission

Aligns resources with developmental priorities

A process for formulating vision and mission statements

Obviously, a municipality cannot include all of the interested parties or stakeholders. The

Strategic Planning Team must be a manageable group and as the number of

participants increases the process is likely to become more unwieldy. Similarly, the

greater the diversity among the participants the more time-consuming it will be to reach

a consensus. Therefore, tradeoffs will have to be made during the selection process to

encourage key participants to join the Strategic Planning Team, based on time and

budgetary constraints of the process. It has been suggested if the numbers are to be

limited at the outset, consider which individuals might be in a position to veto or block

the implementation of the strategy (high-ranking officials and policy makers). These are

the people to include at the outset in the Strategic Planning Team. Generally speaking,

the Strategic Planning Team should not be more than 15 members. The Strategic

Planning Team should also be large enough to operate at two-thirds in full attendance.

The appropriate roles for this committee will include the following:

Develop or approve a list of key issues to be addressed in the planning process.

Review the draft reports.

Assist in the identification and allocation of resources, both for the planning effort

itself and for the implementation of results.

Deciding initial issues such as the area to be addressed and major areas of

concern.

Divide up implementation responsibilities among participating organizations.

Develop or endorse broad goals and at some later point broad strategies.

15.

CITY/ MUNICIPAL MUNICIPALMISSION STATEMENTS

1 Buffalo City Metropolitan

Municipality

Vision

“A responsive, people-centred and developmental City”

Mission

Promote a culture of good governance;

Provide effective and efficient municipal services;

Invest in the development and retention of human capital

to service the City and its community;

Promote social and equitable economic development;

Ensure municipal sustainability and financial viability;

Create a safe and healthy environment; and

Place Batho Pele principles at the centre of service

delivery

2 Cacadu District

Municipality

Vision

A transformed and integrated Cacadu District Municipality

contributing to a sustainable quality of life in our urban and rural

communities.

Mission

To provide equitable, affordable services and sustainable socio-

economic development to improve the quality of life in our

communities, through community participation, capacity-

building and efficient and effective management of resources

3 Amathole District

Municipality

14 | P a g e

16.

1515 | Pa g

e

SESSION 2:

Conduct a stakeholder analysis and develop a framework

for a community participation process.

Learning Outcomes

Various stakeholders are identified that should be consulted in a municipal strategic

planning process.

Current practices with respect to stakeholder analysis and participation are applied

in a municipality's strategic planning process.

Principles are identified from legislation pertaining to community participation as

part of integrated development planning.

2.1. Municipal Stakeholders

The purpose of the IDP process is to determine the needs and priorities of a municipality’s

stakeholders and community which should be addressed towards improving the quality

of life in respect of those concerned. Community and stakeholder participation in

determining those needs is therefore at the heart of the IDP process. The Constitution

and the Systems Act clearly stipulate that a municipality must mobilise the involvement

and commitment of its stakeholders by establishing an effective participatory process.

The municipality should especially ensure participation by previously disadvantaged

groups.

Stakeholder groups that are not organised, i.e. Non-Governmental Organisations

(NGO’s), play a critical role to voice the interests of those groups. Thus it is the nature of

the IDP process to allow all stakeholders who reside or conduct business within a

municipal area to contribute to the preparation and implementation of the IDP.

Stakeholders, or “interested parties,” can be grouped into the following categories:

international/donors, national political (legislators, governors), public (ministry of health

[MOH], social security agency, ministry of finance), labor (unions, medical associations),

commercial/private for-profit, nonprofit (nongovernmental organizations [NGOs],

foundations), civil society, and users/consumers.

17.

1616 | Pa g

e

What Are the Steps in Stakeholder Analysis?

There are eight major steps in the process:

1. Planning the process

2. Selecting and defining a policy

3. Identifying key stakeholders

4. Adapting the tools

5. Collecting and recording the information

6. Filling in the stakeholder table

7. Analyzing the stakeholder table

8. Using the

information.

What Can Be Achieved with Stakeholder Analysis?

Stakeholder analysis yields useful and accurate information about those persons and

organizations that have an interest in health reform. This information can be used to

provide input for other analyses; to develop action plans to increase support for a reform

policy; and to guide a participatory, consensus-building process.

To increase support or build consensus for reform, policymakers and managers must take

additional steps following the stakeholder analysis. In the next phases of the policy

process—constituency-building, resource mobilization, and implementation—

policymakers and managers should use the information generated by the stakeholder

analysis to develop and implement strategic communication, advocacy, and

negotiation plans.

Why is Strategic Planning Important

Municipalities that implement a strategic plan can be more effective and efficient at

utilizing their scare resources to meet the present and future needs of their communities.

Strategic planning helps municipal councils to define a clear purpose; set defined and

realistic goals; provide guidance to administration on day-to-day activities; and be

proactive rather than reactive.

The Seven Steps

Strategic planning can be done in many different ways. In this resource, a seven-step

process is presented.

18.

1717 | Pa g

e

1. Making the Commitment to Plan

It is important that everyone on council, and senior administration members, are on the

same page about the planning process and equally committed to working through it.

Set out a timeline, and make sure you’ve set aside enough resources to make it all

happen. Your municipality should consider whether or not you need to get an outside

facilitator to help you through the planning process. This is highly recommended;

especially the first time you develop a strategic plan.

2. Agreeing on the Municipality’s Responsibilities

In this step, your municipality identifies the things that you are required to do as well as

the things that you do by choice.

3. Developing Mission and Vision Statements

A mission statement describes the what, how and why of the organization’s work;

or who the municipality is, what it wants to do, for whom, where and when.

A vision statement expresses where you want your municipality to be over the

long-term.

Both of these statements are useful to the planning process, however it is often

during arguments over wording of these statements that planning processes

break down. Make sure that you don’t let disagreement derail the planning

process. You can always come back to this step at a later time.

The objective of the step is to describe the work you do and what you want your

municipality to look like at a defined period in the future.

4. SWOT Analysis

SWOT stands for Strengths, Weaknesses, Opportunities, and Threats. SWOT is a

simple tool for completing the essential environmental scan, which provides your

municipality with the information you need to have in order to be able to begin

making decisions.

Strengths and Weaknesses are internally focused lenses. The idea is to examine

your municipality and honestly assess yourself.

19.

1818 | Pa g

e

Opportunities and Threats are externally focused lenses. In this case, your

municipality must consider all of the external factors that impact your

municipality.

A completed SWOT analysis paints a good picture of the environment in which

your municipality must operate.

5. Prioritizing the Issues

Once you know the environment you’re operating in, and you know where you

want to go (Vision/Mission), then you need to begin to identify what you are

going to do to get there. One way to do this is through open brainstorming,

where everyone gets to contribute their ideas.

Eventually, you will need to look at all of your ideas and start to prioritize them.

Make sure to consider which ideas will have the greatest impact, for the minimum

amount of effort, in helping your municipality achieve its goals.

6. Creating an “Action Plan”

Once you have prioritized your ideas/strategies, you need to develop specific

action plans to show how you will implement them. While your vision statement

might look ten years down the road, your action plan should be focused on a

timeline more like three years.

For each idea/strategy, identify what will be done to work towards it, by when, by

whom, and using what resources. Be as specific as you can, and make sure that

everyone knows how their work is contributing towards progress.

7. Monitoring and Evaluating the Plan

Reviewing the plan, and evaluating your progress, is a critically important step if

your municipality’s strategic planning efforts are to be useful. Evaluations are

most effective when everyone has some degree of accountability.

Regular reports to council (at least quarterly) are one way to keep everyone

focused. It is also important for the council to feel free to make changes to the

strategic plan if unforeseen circumstances arise. This can’t happen without an

ongoing process of monitoring and evaluating the plan.

20.

1919 | Pa g

e

SESSION 3:

Identify key performance areas applicable to institutional

strategies as required by the local government legislative

framework.

Learning Outcomes

Key performance areas are identified as required by legislation in the context of a

municipality.

Key performance areas are aligned with vision and mission statements.

Key performance areas are evaluated in terms of institutional arrangements.

3.1. Performance management

Performance management is a new requirement for local government in South Africa.

Moreover it is a specialised field with concepts usually interpreted and applied

differently. This learning unit, therefore, seeks to assist councilors, managers, officials and

local government stakeholders in developing and implementing a performance

management system in terms of the requirements of the legislation. The learning unit also

strives to establish common language and thereby ensure some level of consistency and

uniformity in the application of concepts.

The learning unit is not meant to prescribe what municipalities must do, but only to

provide guidelines. It is also not meant to go into detail about the integrated

development planning processes and employee performance management, but only

to draw the necessary linkages to the overall organisational performance management.

3.2 Policy Background

3.2.1 The Batho Pele White Paper

The Batho Pele White Paper notes that the development of a service-orientated culture

requires the active participation of the wider community. Municipalities need constant

feedback from service-users if they are to improve their operations. Local partners can

be mobilised to assist in building a service culture. For example, local businesses or non-

21.

2020 | Pa g

e

governmental organisations may assist with funding a help line, providing information

about specific services, identifying service gaps or conducting a customer survey.

3.2.2 The White Paper on Local Government

The White Paper on Local Government (1998) proposed the introduction of performance

management systems to local government, as a tool to ensure Developmental Local

Government. It concludes that:

"Integrated development planning, budgeting and performance management are

powerful tools which can assist municipalities to develop an integrated perspective on

development in their area. It will enable them to focus on priorities within an increasingly

complex and diverse set of demands. It will enable them to direct resource allocations

and institutional systems to a new set of development objectives."

The White Paper adds that:

"Involving communities in developing some municipal key performance indicators

increases the accountability of the municipality. Some communities may prioritise the

amount of time it takes a municipality to answer a query; others will prioritise the

cleanliness of an area or the provision of water to a certain number of households.

Whatever the priorities, by involving communities in setting key performance indicators

and reporting back to communities on performance, accountability is increased, and

public trust in the local government system enhanced".

3.3 Legislative Requirements

3.3.1 The Municipal Systems Act

Following the processes of developing a policy framework on performance

management, the Municipal Systems Act, containing the framework was passed. The

Municipal Systems Act, enacted in November 2000, requires all municipalities to:

Develop a performance management system

Set targets, monitor and review performance based on indicators linked to their

integrated development plan (IDP)

Publish an annual report on performance for the councillors, staff, the public and

other spheres of government

Incorporate and report on a set of general indicators prescribed nationally by the

minister responsible for local government

Conduct an internal audit on performance before tabling the report

22.

2121 | Pa g

e

Have their annual performance report audited by the Auditor-General

Involve the community in setting indicators and targets and reviewing municipal

performance.

3.4. Setting Key Performance Indicators (KPIs)

What are Indicators?

They are measurements that tell us whether progress is being made in achieving our

goals. They essentially describe the performance dimension that is considered key in

measuring performance. The ethos of performance management as implemented in

local governments internationally and as captured in the White Paper on Local

Government and the Municipal Systems Bill, rely centrally on the use of KPIs.

Value of Indicators

Indicators are important as they:

Provide a common framework for gathering data for measurements and

reporting

Translate complex concepts into simple operational measurable va riables

Enable the review of goals and objectives

Assist in policy review processes

Help focus the organisation on strategic areas

Help provide feedback to the organisation and staff

Types of Indicators

With all the talk of indicators in local government recently, it is possible that you have

heard many names describing different types of indicators. This section will try to explain

some of the useful types of indicators.

A. Input Indicators

These are indicators that measure economy and efficiency. That is, they measure what it

cost the municipality to purchase the essentials for producing desired outputs

(economy), and whether the organisation achieves more with less, in resource terms

(efficiency) without compromising quality. The economy indicators are usually expressed

in unit cost terms. For example, the unit cost for delivering water to a single household.

On the other hand, efficiency indicators may be the amount of time, money or number

of people it took the municipality to deliver water to a single household.

2323 | Pa g

e

These are the indicators that measure whether a set of activities or processes yields the

desired products. They are essentially effectiveness indicators. They are usually expressed

in quantitative terms (i.e. number of or % of). An example would be the number of

households connected to electricity as a result of the municipality’s electrification

programme. The output indicators relate to programme activities or processes.

C. Outcome Indicators

These are the indicators that measure the quality as well as the impact of the products in

terms of the achievement of the overall objectives. In terms of quality, they measure

whether the products meet the set standards in terms of the perceptions of the

beneficiaries of the service rendered. Examples of quality indicators include an

assessment of whether the service provided to households complies with the applicable

standards or percentage of complaints by the community. In terms of impact, they

measure the net effect of the products/services on the overall objective. An example

would be percentage reduction in the number of houses burnt due to other sources of

energy, as a result of the electrification programme. Outcome indicators relate to

programme objectives.

D. Cost, Input, Process, Output & Outcome Indicators

These sets of different indicators relate to the ingredients, products and effects of

organisational processes

Inputs are what go into a process

Costs are what the inputs cost us

Processes are the set of activities involved in producing something

Output is the product or service generated

25.

2424 | Pa g

e

Outcome is the impact or effect of the output being produced and the process

undertaken

The measurement of costs, inputs, process, outputs and outcomes are valuable in

developmental local government. Let us look at an example of addressing housing

needs:

The Housing Process can be seen as follows:

The outcome indicators here are particularly useful in telling us about the quality of

houses and the housing process and whether we are producing the right outputs in the

right location. For example:

A municipality decides that it wishes to reduce the percentage of population not living

in formal serviced structures by 5% a year. To effect this, it decides to build 3000 houses

per year. Two years later, in measuring its performance, it finds it has built 3000 houses

per year, but discovers that the percentage of population not living in formal houses has

only decreased by 1% a year.

There are many possible reasons for this, but the most significant is that either the output

or the process is inappropriate:

The number of houses planned for could be too low

The location of the houses could be highly inaccessible to work and other

resources

The community may not have been consulted on the type of houses or their

location

The houses may be too small or of poor quality

26.

2525 | Pa g

e

The houses may not be affordable

Outcome indicators allow us to check whether our development strategies and policies

are working. They help us to identify gaps and improve strategies and policies.

The Municipal Systems Act requires local government to measure its performance on

outputs and outcomes. The measurement of inputs and processes are also useful, at a

local level.

E. Composite Indicators

Outcome indicators can be developed for each local government function. Each

function can have a variety of outcomes that need to be measured. The danger of this

is that the municipality can end up with a very long list of indicators that becomes

difficult to manage and communicate. One possible response to this problem is to use

composite indicators for each sector (transport, water, sanitation, electricity, public

participation, housing, etc.) or across sectors. Composite indices combine a set of

different indicators into one index by developing a mathematical relationship between

them.

An example of a popular composite index is the Human Development Index. It measures

three basic elements of human development: life expectancy, educational attainment

(adult literacy combined with primary, secondary and tertiary enrolment) and real gross

domestic product (GDP) per capita.

Composite indices are useful in simplifying a long list of indicators and the complex

relationships between them into one index. However, they do have their disadvantages.

It is very difficult to ensure citizen and community involvement in developing,

understanding and monitoring composite indices, as they appear to be unrelated to

everyday life. Additionally, certain specific problem areas can become hidden and are

often overlooked when aggregated into a single composite index. Knowing their

usefulness and their disadvantages, it is up to your council to decide whether or not

composite indicators are appropriate. It is however advisable to start your PM system at

the very basic level, which may mean identifying a handful of priorities and setting as

few as possible indicators for those priority areas. Composite indicators can be

introduced in later years when the list of indicators gets longer and the capacity of

citizens to participate is developed.

F. Baseline Indicators

27.

2626 | Pa g

e

These are indicators that show the status quo or the current situation. They may indicate

the level of poverty, service, infrastructure and so forth. They are usually utilised in the

planning phase to indicate the challenges the organisation is faced with. They are

important, since organisations use them to assess whether programmes are indeed

changing the situation.

How to Identify Indicators

In identifying indicators, it is important that a municipality:

Looks at the priorities and objectives set in the IDPs

Clusters the development objectives into key performance areas including

service delivery, development, institutional transformation, governance and

financial issues

Looks at the activities and processes identified in the IDP to achieve the

objectives

Looks at the resources earmarked to achieve the objectives

Identifies the indicators for inputs, outputs and outcomes

Input indicators are used to measure resources, output indicators are used to measure

the activities or processes while the outcome indicators are used to measure impact.

A municipality must identify indicators for each of the areas outlined above, brainstorm

them and rigorously check whether they are:

28.

2727 | Pa g

e

The process of setting indicators may be a sensitive one. It is therefore important that the

political leadership and communities be involved centrally. There has to be a political

champion for this process. Communities can be involved through various means

including participation in structures established by Council, consultations and public

hearings.

It is however important to note that there will never be a stage where there is complete

consensus on indicators among everybody and therefore Council will have to take

decisions at some point.

It is also important to start on a small scale and use output/quantity indicators in the

beginning. However, municipalities need to avoid the temptation to set indicators for

areas that easily lend themselves s to measurements. This is important and is the reason

that government decided to develop national indicators. These indicators have to be

incorporated into the local indicators.

Another important factor in choosing an indicator is whether data is available for its

measurement in your municipal area. A municipality needs to be clear about what data

it currently collects and what data it will have the capacity to collect in the near future.

It will also be useful for your municipality to know what data is being collected by other

institutions, such as universities, technikons, schools and hospitals in your municipal area.

It is advisable to co-operate with these institutions in sharing information that is useful.

29.

2828 | Pa g

e

Statistics South Africa collects a significant amount of data, primarily through the

National Census. Other data sources include the October Household Survey and the

Development Bank of Southern Africa.

International experience has shown that "home-grown" indicators can be very useful in

ensuring public participation in the performance management process. "Home grown"

indicators are indicators suggested by citizens and communities that are directly

relevant to the development plans and challenges of the area. The inclusion of some

"home-grown" indicators will ensure greater credibility, legitimacy and participation from

citizens and communities.

30.

2929 | Pa g

e

SESSION 4:

Formulate institutional strategies

Learning Outcomes

Participatory processes are applied to inform institutional strategies.

The economic, social and environmental context of a municipality is evaluated

when weighing alternative strategies.

Institutional strategies are identified in alignment with national and provincial plans

and programmes

Programmes are developed to align service delivery activities to the institutional

strategies.

4.1. Introduction.

‘Institutional strategy’ is a pattern of organizational action that is directed toward

managing the institutional structures within which firms compete for resources, either

through the reproduction or transformation of those structures.

4.2. Institutional economics

Institutions are indiscernible joint concepts created by human beings, which are difficult

to identify and measure. Polski and Ostrom (1998, p59) stated, “Rules are the do’s and

don’ts that one learns on the ground that may not exist in any written document”. Hess

and Ostrom (2004) described institutions as the rules, norms and behaviours that two or

more people use in interacting and making decisions that produce outcomes and

consequences. North (2005) described institutions as “humanly-devised constraints or a

regulatory framework of laws, rules, regulations, norms, practices and procedures that

structure human interaction”. Gabre-Madhin (2001) noted that institutions are

governance tools that help individuals cooperate and overcome market failures. North

(1990) described institutions as arrangements between economic agents in attempt to

decrease insecurity and costs in trading and ownership. Lastly, Commons (1931) defined

an institution as a collective action in control, liberation and expansion of individual

action; collective action being more than control and liberation of an individuals’ action

while individual actions are transactions not individuals’ behaviour.

31.

3030 | Pa g

e

New Institutional Economists describe institutions as the “Rules of the Game” of a society

(Nothard et al, 2005, Kherallah and Kirsten, 2002; Langlois, 1986; North, 1990; North, 2005).

“Rules of the Game” are the strategies used or tactics of the players that have an

influence on the processes and outcomes of the game.

Institutions are the prime motivation for individuals to engage and produce economic

products efficiently. Thus, institutional designing enables players within a system to

acquire essential information, skills and tactics, which will be of great importance in

effective resource allocation thereby leading to profit maximization and efficiency within

that system (Kherallah and Kirsten 2002). In a war scenario, if an untrained army is taken

to a war/fighting zone usually that army will lose usually because of lack of confidence.

Lack of confidence in this case will be due to lack of skills and tactics to win the war. In

farming, the war is usually around market share and maximisation of profit. Therefore, a

successful farmer is that one who will after careful planning gain a larger share of the

market (profit) when compared to other farmers. North (1990) noted that not all

institutions are efficient, since they are crafted by human beings. This means that some

institutions are better (more efficient) than others as with the varying of intelligence

among different individuals. North (2005) went on to say institutions can be designed to

achieve either efficient or inefficient outcomes, thus they cannot be ignored in

economic analysis, as they play a significant role in economic performance. Therefore,

one can say institutions are created to serve the interests of those with the power to

create new rules

4.3. Institutional arrangements versus institutional environment

The study of New Institutional Economics consists of two study levels, the macro and

micro level. The macro level deals with the institutional environments, which are the

background constraints or ‘rules of the game’, that guide individuals’ behaviour and

performance of economic actors (Davis and North, 1971). The background constraints

are the result of the goals, beliefs and choices of individual actors. Williamson (1993)

describes background constraints as the set of fundamental political, social and legal

ground rules that establish the basis for production, exchange and distribution.

The micro level analysis, also known as the institutional arrangements, deals with the

institutions of governance. An institution of governance is the playing of the game within

institutional environment using markets, hybrids, firms or bureaus (Ellis, 2004). Institutional

arrangements are specific strategies or governance structures made by specific

32.

3030 | Pa g

e

individuals to administer their own relationships and assist particular exchanges.

Contracts, organizations, the business firm, public bureaucracies, other contractual

agreements, competitive coordination, interlocking and regulated monopolies are

examples of institutional arrangements that need to be central to any analysis of the

effects of trade liberalization on smallholder farmers (Klein, 1999, FAO, 2006). According

to Kherallah and Kirsten (2002), institutional arrangements refer to the modes of

managing transactions (market, hierarchical modes of contracting, hybrids, firms or

bureaus, etc) or are arrangements between economic units that govern the ways in

which its members can cooperate and / or compete.

4.4. Coordination within economic systems

Coordination efficiency within economic systems is studied under transaction costs

economics of which today’s survival, way of doing things and a large part of our

national income is devoted to transacting. It is hypothesized under Transaction Cost

Economics that institutions are transaction cost-minimizing arrangements (Ellis, 2004);

which can be observed through relationships between producers, consumers and

market chain intermediaries. Cost-minimizing arrangements make it easier, cheaper and

less risky for producers, consumers and market chain intermediaries to communicate

and to trade with one another over longer distances between different communities.

Ellis (2004) noted that mechanical systems have friction, which he equated transaction

costs as the friction within economic systems. A transaction occurs when a good or

service is transferred from one individual to another across a technologically divisible

crossing point (Kherallah and Kirsten 2002). On a smooth crossing point, transfers occur

smoothly and cost free but if the crossing point has an impediment, transaction costs

increase as the level of the impediment increases. Therefore, since transaction costs are

fixed per transaction or per transaction relationship, increasing traded volumes as

observed in commercial farming can also reduce transaction costs per unit good

transacted.

Transaction costs include search, monitoring, information, coordination, arbitration,

definitions of property rights, changing of institutional arrangements, decision, policing

and enforcement of contract costs (Ellis, 2004; Williamson, 1985; Kherallah and Kirsten,

2002). Every transaction involves these costs; the costs in turn are influenced by social,

legal, political and economic institutions.

33.

3131 | Pa g

e

Table 2.1: Institutional groupings

GROUP OF INSTITUTION DEFINITION

Social Institutions Norms of behaviour

Legal Institutions Definition and enforcement of property rights

Political Institutions Mechanisms by which property rights are allocated

Economic Institutions Availability and efficiency of markets

Tavares de Araujo (1997) noted that transaction costs are raised by cumbersome judicial

systems, inefficient public services or lack of human capital; in contrast, they can be

reduced by deregulation, trade liberalization, transparent public procedures and

technical progress. The level of transaction costs or the costs of coordination within an

organisation are influenced by its ability to purchase inputs from other organisations; the

supply of those inputs depends in part on costs of coordination and the level of

transaction costs (Ellis, 2004). This interaction on its own without the additions of other

institutions like laws, social system, culture and the effects of technological changes is a

complex and interrelated structure. The level and nature of transaction costs is

determined by the extent of imperfect information involved in making a transaction,

which in turn influences the ease or difficulty of contracting (Kherallah and Kirsten, 2002).

Information asymmetries yield incomplete contracts, which result in high transaction

costs, market failures and incomplete markets as often observed in developing

countries. Therefore, the key challenge for smallholder farmers is to devise institutional

arrangements, which are able to reduce transactions costs.

Contracts have an essential role in Transaction Costs Economics. They protect parties

from the opportunistic behaviour of seeking private gain at the expense of other parties.

Contracts also enable both parties involved in a transaction to fulfil their obligations, in

the process decreasing the transaction costs (Ortmann and King, 2006). It should also be

noted that contracts are not equally effective. Effectiveness of a contract in facilitating

exchange depends on its completeness and the relevant body of contract law.

Incomplete contracts will manifestly result in transaction costs and opportunism. Causal

factors of incomplete contracts are bounded rationality, information lop-sidedness and

complications in measuring performance (Royer, 1999). Williamson (1985) mentioned

that all transaction costs are derived from a combination of bounded rationality and

opportunism.

34.

3232 | Pa g

e

The principal dimensions describing a transaction, according to Williamson (1985), are

uncertainty, frequency of exchange, and asset specificity. These three dimensions are

critical in designing an optimal institutional arrangement. In the agricultural sector,

available studies have tended to focus on distance to market as a single indicator of

transaction costs (Omamo, 1995; Oruko, 1999). Conclusively, high transaction costs result

in bad economic performance as it will be costly for human beings to interact and

engage in various kinds of economic activity. The ultimate result will be poor

performance leading to poverty.

35.

3333 | Pa g

e

SESSION 5:

Demonstrate knowledge of the legislative framework for

integrated development planning and apply requirements

of legislation.

Learning Outcomes

Legislative pre-requisites are interpreted with regard to the adoption of an

integrated development plan.

Core components of an integrated development plan are identified based on

legislative requirements

An integrated development plan is completed in terms of relevant legislative

requirements

An integrated development plan is reviewed in terms of the requirements of the

legislated annual review and amendment process.

5.1. Integrated development planning

Integrated development planning is an approach to planning that is aimed at involving

the municipality and the community in finding the best solutions towards sustainable

development.

An Integrated Development Plan (IDP) is a super plan for an area that gives an overall

framework for development. It aims to co-ordinate the work of local and other spheres

of government in a coherent plan to improve the quality of life for all the people living in

an area. It takes into account the existing conditions and problems and resources

available for development.

Through Integrated Development Planning, which necessitates the involvement of all

relevant stakeholders, a municipality?

Identifies its key development priorities

Formulates a clear vision, mission and values

Formulates appropriate strategies

Develops the appropriate organisational structure and systems to realise the vision

and mission

36.

3434 | Pa g

e

Aligns resources with developmental priorities

5.2. Legal status of IDP.

In terms of the Systems Act, all municipalities (i.e. metropolitan, district and local) have to

undertake an IDP process to produce IDP’s. As the IDP is a legislative requirement it has a

legal status and it supersedes all other plans that guide development at local

government level.

Chapter 5 Municipal Systems Act Section 25(1)

25.(1) Each municipal council must, within a prescribed period after the start of its

elected term, adopt a single, inclusive and strategic plan for the development of the

municipality which –

(a) links, integrates and co-ordinates plans and takes into account proposals for the

development of the municipality;

(b) aligns the resources and capacity of the municipality with the implementation of the

plan;

(c) forms the policy framework and general basis on which annual budgets must be

based;

(d) complies with the provisions of this Chapter; and

(e) is compatible with national and provincial development plans and planning

requirements binding on the municipality in terms of legislation

5.3. Core components of an integrated development plan

In a nutshell, the IDP process entails an assessment of the existing level of development

and the identification of key development priorities. The vision and mission statements for

long term development flow from the aforesaid, with specific reference to critical

developmental and internal transformational needs. The development strategies and

objectives will be directed at bridging the gap between the existing level of

development and the vision and mission.

A very critical phase of the IDP process is to link planning to the municipal budget (i.e.

allocation of internal or external funding to the identified projects), because this will

ensure that the IDP directs the development and implementation of projects.

37.

3535 | Pa g

e

Municipal Systems Act, 2000, Section 26:-

26. An integrated development plan must reflect –

(a) the municipal council’s vision for the long term development of the municipality with

special emphasis on the municipality’s most critical development and internal

transformation needs;

(b) an assessment of the existing level of development in the municipality, which must

include an identification of communities which do not have access to basic municipal

services;

(c) the council’s development priorities and objectives for its elected term, including its

local economic development aims and its internal transformation needs;

(d) the council’s development strategies which must be aligned with any national or

provincial sectoral plans and planning requirements binding on the municipality in terms

of legislation;

(e) a spatial development framework which must include the provision of basic

guidelines for a land use management system for the municipality;

(f) the council’s operational strategies;

(g) applicable disaster management plans;

(h) a financial plan, which must include a budget projection for at least the next three

years; and

(i) the key performance indicators and performance targets determined in terms of

section 41.

38.

The following isa proposed IDP process that a municipality can follow:

36 | P a g e

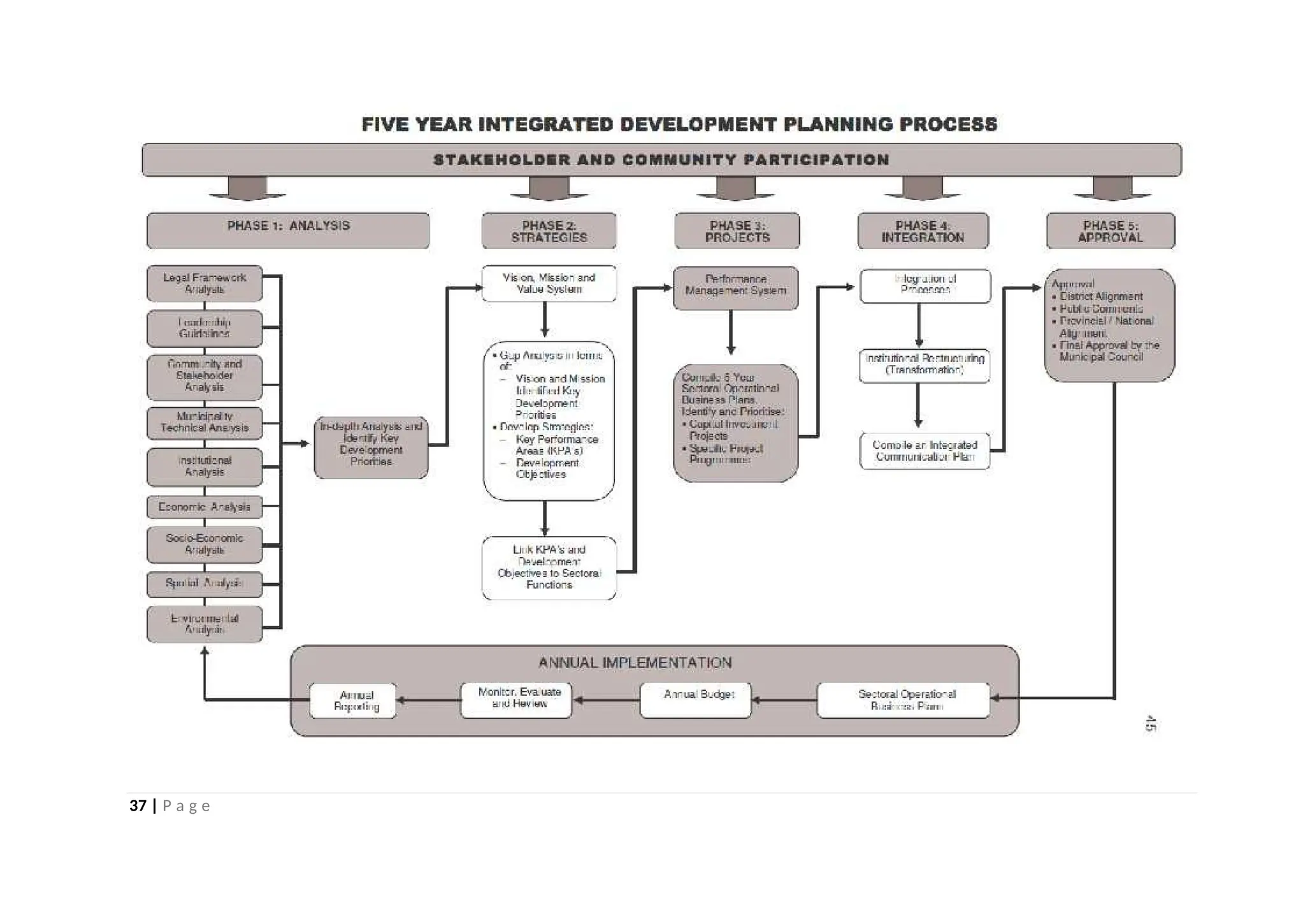

5.4. The IDPplanning process

Strategic management is the process whereby managers establish an organisation’s long-term direction, set specific

performance objectives and develop strategies to achieve these objectives in the light of all the relevant internal and external

circumstances, and undertake to execute the chosen action plans.

Strategic management basically comprises of the following:

Defining the organisation’s business and developing a strategic vision and mission as a basis for establishing what the

organisation does and doesn’t do and where it is heading;

Formulate strategies as well as strategic objectives and performance targets;

Implementing and executing the chosen strategic plan; and evaluating strategic performance and making corrective

adjustments in strategy and/or how it is being implemented in light of actual experience, changing conditions, and new

ideas and opportunities.

Integrated development planning may be defined as the strategic management process utilised by local government. It is a

process through which municipalities prepare a strategic development plan, for a five (5) year period. The IDP is the product of

the IDP process. The IDP is the principal strategy planning instrument which guides and informs all planning, budgeting,

management and decision-making processes in a municipality.

38 | P a g e

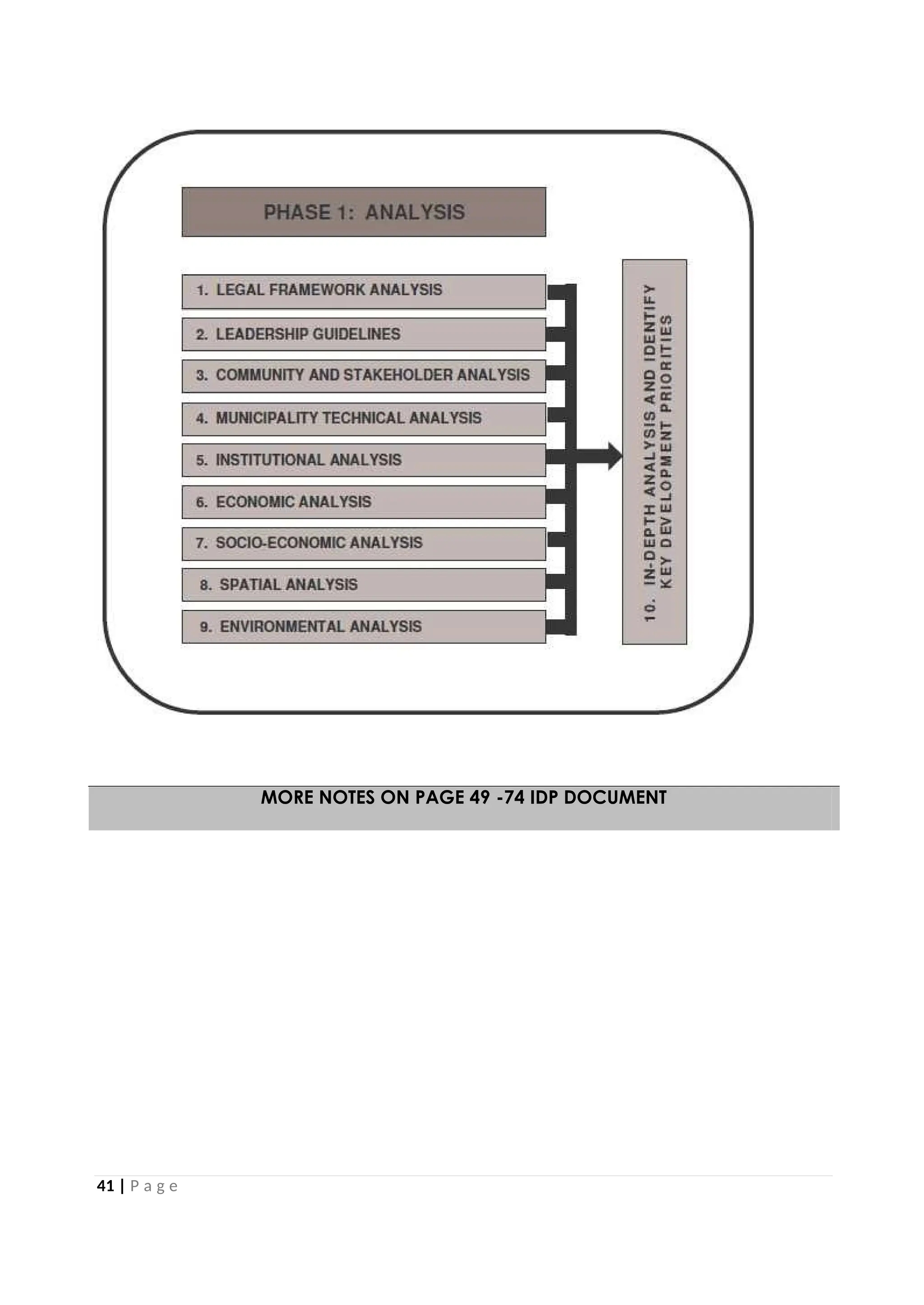

PHASE 1: ANALYSIS

Duringthis phase an analysis of the existing problems faced by people in a specific

municipal area is conducted. The issues normally range from lack of basic services to

crime and unemployment. The identified problems are considered and prioritised

according to levels of urgency and/or

importance, thus constituting the key

development priorities.

During this phase it is important that a

municipality understands not only the

symptoms, but also the causes of

problems in order to make informed

decisions on appropriate solutions.

Stakeholder and community

participation is very critical in this phase.

The municipality must not make assumptions on what the problems are in its area. The

people affected should be involved in determining the problems and priorities.

It is important to determine the key development priorities, due to the fact that the

municipality will not have sufficient resources to address all the issues identified by

different segments of the community. Prioritisation assists the municipality to allocate

scarce resources to those issues highlighted as more important and/or urgent.

The municipality must be aware of existing and accessible resources and of resource

limitations in order to devise realistic strategies.

40 | P a g e

4343 | Pa g

e

SESSION 6:

Formulate programs and develop methods for monitoring

the implementation of a strategic plan and related

programmes.

Learning Outcomes

Methods are developed which will allow the implementation of the plan to be

monitored throughout the time period of the planned program.

Indicators are developed to be used in the measurement of the delivery of all

elements of a plan.

SEE YOUR SUMMATIVE ASSESSMENT PROJECT.

46.

2

4444 | Pa g

e

Apply approaches to managing

municipal income and expenditure within

Learning Unit

a multi-year framework

UNIT STANDARD NUMBER : 116342

LEVEL ON THE NQF : 6

CREDITS : 15

FIELD : Business, Commerce and Management Studies

SUB FIELD : Public Administration

PURPOSE:

This Unit Standard is for all people involved in municipal financial management. The unit

standard can contribute to social and economic transformation through equipping municipal

practitioners with skills in managing income and expenditure, which could transla te into

better use of resources and improved delivery of services that will benefit the economy and

social development.

The qualifying learner will be able to:

Advise on, and choose from a range of approaches that will ensure a municipality uses

its resources and revenue raising instruments in an efficient and sustainable manner.

Contribute to managing municipal income and expenditure over the medium term.

Budget in a manner, which conforms to the legislative framework for local

government.

LEARNING ASSUMED TO BE IN PLACE:

It is assumed that the Learners are competent in:

• Communication at Level 4.

• Mathematical Literacy at Level 4.

• Economics at Level 4.

47.

4545 | Pa g

e

SESSION 1:

Develop approaches to managing a municipality's revenue

in a sustainable manner.

Learning Outcomes

The Criteria for assessing tax instruments and user charges are applied in the local

government context.

Recommendations for achieving sustainability are provided in relation to municipal

revenue.

Tax incidence of revenue levying collection legislation is explained as it relates to

the local government context.

The incentive effects of municipal tariffs and user charges are estimated in the local

government context.

2.1. Taxes and user changes

To tax is to impose a financial charge or other levy upon a taxpayer (an individual or

legal entity) by a state or the functional equivalent of a state such that failure to pay is

punishable by law.

Taxes are also imposed by many subnational entities. Taxes consist of direct tax or

indirect tax, and may be paid in money or as its labour equivalent (often but not always

unpaid labour). A tax may be defined as a "pecuniary burden laid upon individuals or

property owners to support the government; a payment exacted by legislative

authority." A tax "is not a voluntary payment or donation, but an enforced contribution,

exacted pursuant to legislative authority" and is "any contribution imposed by

government [...] whether under the name of toll, tribute, tallage, gabel, impost, duty,

custom, excise, subsidy, aid, supply, or other name.

Taxation has four main purposes or effects: Revenue, Redistribution, Repricing, and

Representation.

48.

4646 | Pa g

e

The main purpose is revenue: taxes raise money to spend on armies, roads,

schools and hospitals, and on more indirect government functions like market

regulation or legal systems.

A second is redistribution. Normally, this means transferring wealth from the richer

sections of society to poorer sections.

A third purpose of taxation is repricing. Taxes are levied to address externalities; for

example, tobacco is taxed to discourage smoking, and a carbon tax discourages

use of carbon-based fuels.

A fourth, consequential effect of taxation in its historical setting has been

representation. The American revolutionary slogan "no taxation without

representation" implied this: rulers tax citizens, and citizens demand accountability

from their rulers as the other part of this bargain. Studies have shown that direct

taxation (such as income taxes) generates the greatest degree of accountability

and better governance, while indirect taxation tends to have smaller effects.

Dedicated taxes and user charges in use at present

Dedicated taxes are usually based on some indirect link between the incidence of the

tax and utilisation of the services in question. Dedicated taxes currently employed in

South Africa include levies on the sale of fuel (assigned to the Multilateral Motor Vehicle

Accident (MVA) Fund, the Equalization Fund for subsidisation of Sasol and Mossgas and

the National Road Safety Fund), social security taxes (unemployment insurance

contributions and workmen's compensation levies) and RSC levies on turnover and

payroll (for financing local infrastructure). In addition, minor selective taxes, levies or fees

are assigned to various extra-budgetary agencies (see appendix 1) and local property

taxes and surpluses on municipal water and electricity trading accounts are earmarked

for municipal services.

User charges, on the other hand, imply a direct link between financing and the use of

services or exercise of certain rights. Examples include admission charges to museums

and public parks, sales of agricultural or forestry produce, road tolls, charges for

passports or ID documents, licence fees, mining leases, and hospital or school fees. User

charges, like taxes, can be either collected as part of general revenue or retained as

income of service providers. In some cases, the distinction between dedicated levies

49.

4747 | Pa g

e

and user charges is hard to draw. TV licence fees and training board levies, for example,

can be thought of as selective "benefit taxes" or as earmarked user charges

50.

4848 | Pa g

e

It appears that earmarked taxes outside of the national and provincial budget

appropriations amount to about 1,5 per cent of GDP, or about 6 per cent of total tax

revenue. During 1993 or 1993/94, social security taxes amounted to about R2 billion,

levies on fuel contributed R1,11 billion to the Motor Vehicle Accident Fund and R1,15

billion to the subsidisation of Sasol and Mossgas, and RSC levies amounted to R1,7 billion.

Selective taxes or levies contributed R167 million to the financing of other extra-

budgetary accounts or funds

User charges and sales contribute at least a further 1,5 per cent of GDP to public sector

revenue. Departmental and other non-tax current receipts generated R721 million at the

national level of Government in 1993/94 and R1,6 billion at the provincial level in 1992/93.

In addition to these contributions of user charges to the fiscus, sales of goods and

services accounted for R1,5 billion of the income of government enterprises in 1993/94,

R1,8 billion of the 1993 income of universities and technikons, and R726 million of the

1993/94 income of extra-budgetary accounts and funds.

Arguments for and against tax earmarking and user charges

The main argument for selective taxes or user charges is that they provide a link between

the costs and benefits of public services, and accordingly enhance the efficiency and

fairness of public sector resource allocation. User fees impose a direct cost on consumers

of services. Where this is not possible, selective taxes can provide an indirect substitute

linkage. It is also sometimes argued that dedicated taxes serve to enhance public

awareness of the general links between services and the required burden of financing,

or that public expenditure management is enhanced by restricting funding of specific

programmes to specific sources of revenue.

It must immediately be pointed out that the above arguments in favour of dedicated

taxes do not encompass the proposition that important functions of government might

derive additional resources from the employment of such financing arrangements. The

overall quantum of resources available to the public sector is unavoidably constrained

by macroeconomic considerations, so that financing mechanisms which enhance

resource flows of one kind must be offset by reduced allocations elsewhere. The case for

vesting particular departments or agencies of government with the right to impose

selective taxes or fees cannot be made on the grounds of need for additional sources of

finance, but must rather be sought in the efficiency and fairness of such assignments.

51.

4949 | Pa g

e

Levies and User Charges

Enterprises of all sizes are directly impacted by the rates, tariffs and levies imposed by

municipalities for the delivery of certain services. Due to the range of services provided

by municipalities, the rates and tariffs faced by enterprises include tariffs for water,

sanitation; refuse removal and electricity and regional service council (RSC) levies. Figure

2.1 indicates the different income categories for municipalities based on data from 6

metropolitan and 17 local municipalities. From the graph it is clear that user charges

make up a significant source of revenue for municipalities and therefore have a direct

impact on their financial position. Thus it is imperative to include policies that guide the

levying of user charges in any discussion about the impact of local government

regulation on small businesses.

2.2. Recommendations for achieving sustainability.

Like any private enterprise, a public utility will face financial obligations in the normal

course of its operations. If society expects the service to be provided indefinitely, it must

ensure that the utility has sufficient funds to meet its financial obligations as they occur.

The funds required to sustain the utility can come from a variety of sources, including

52.

5050 | Pa g

e

transfers from the government’s general revenue (direct subsidies), from loans or equity,

or from revenue collected through user charges.

Financial sustainability, like good governance, is always a relevant goal, but it is most

important when the utility has not been subject to strict financial discipline. For example,

even if the utility charged for its services, the government might have implicitly assumed

responsibility for sustaining the utility, thereby removing any effective budget constraint.

Focusing on financial sustainability can limit or reduce the government’s financial

commitment, and improve the utility’s performance.

A public utility is financially sustainable (or “sustainable”) if it has sufficient funding to

meet the financial obligations it will incur in the future. The identified financial obligations

must be consistent with maintaining the targeted level of service, and the funding must

be secure, regardless of the source.

Financial sustainability

Pursuing financial sustainability involves two different kinds of analyses: (i) a financial

analysis, to determine the funds that the utility requires to maintain the targeted level of

service; and (ii) if the utility is to be subsidized, an analysis of the rationale and security of

the subsidy.

The financial analysis is largely a cash flow or accounting exercise, focused on

establishing the financial obligations the utility would necessarily face in both the short

and medium run. Measuring and identifying costs is an important part of this step, but

the focus is not strictly on costs. Instead, the focus is on establishing the funds required to

sustain the utility.

Costs are also important in other goals, such as economic efficiency and price fairness,

where the term may have different meanings and implications, and so it is important

that “costs” be defined and used precisely. In the context of financial sustainability,

“cost” is strictly a financial or accounting concept, and the only costs that are relevant

are those that are part of the utility’s future financial obligations. These obligations may

include a profit element, at whatever level the public decides.

For example, the utility may be required to pay income or property tax. Such a tax may

not represent a social cost, but since the utility is obligated to pay the tax, it is a financial

obligation that is relevant to sustainability. Similarly, a utility may purchase inputs, such as

fuel, whose price is subsidized by the government. The cost of the fuel to the utility may

53.

5050 | Pa g

e

be less than the cost to the society, but as long as the subsidy is stable and likely to

persist into the future, the price the utility pays is the only thing relevant to financial

sustainability

Although subsidies may pose problems for other goals, subsidies are consistent with

financial sustainability as long as they are explicit and secure. Such subsidies could be

specific (for example, the government will provide a given amount per poor person

served) or open-ended. A non-toll road network, for example, is a public service that is

guaranteed to be funded by subsidies.

If the utility is directly subsidized, analysis of the subsidy should establish its rationale,

timing, and extent; the government’s commitment to the subsidy; and the government’s

financial capacity to fulfill that commitment. This involves social, economic, and political

analyses, and so establishing the security of a subsidy significantly increases the effort

required to develop a financially sustainable tariff. Without such an analysis, however,

the financial sustainability of the utility cannot be assured, and the tariff should be

designed to generate sufficient revenue without the subsidy.

The difference between the funds required to sustain the utility, and the fund available

from subsidies (or other sources of income) determines the revenue required from the

tariff. The aim of a tariff, with respect to sustainability, is only to generate this required

level of revenue. How the tariff generates that revenue is irrelevant to achieving

sustainability, and so sustainability does not directly restrict the structure of the tariff.

Conflicts with Other Goal

As mentioned above, financial sustainability can conflict with predictability, if

sustainability requires a significant increase in charges. In that case, both goals cannot

be achieved in the short term.

A gradual increase in charges can preserve predictability, and achieve financial

sustainability in the medium term.

Financial sustainability can conflict with distributive justice, if a sufficient number of the

utility’s customers cannot afford the service at a charge consistent with financial

sustainability. The next section discusses further the potential conflict between

sustainability and justice.

54.

5151 | Pa g

e

2.3. Tax incidence of revenue levying collection legislation

Tax incidence is an economic term for the division of a tax burden between buyers and

sellers. Tax incidence is related to the price elasticity of supply and demand. When

supply is more elastic than demand, the tax burden falls on the buyers. If demand is

more elastic than supply, producers will bear the cost of the tax.

Tax incidence reveals which group, the consumers or producers, will pay the price of a

new tax. For example, the demand for cigarettes is fairly inelastic, which means that

despite changes in price, the demand for cigarettes will remain relatively constant. Let's

imagine the government decided to impose an increased tax on cigarettes. In this

case, the producers may increase the sale price by the full amount of the tax. If

consumers still purchased cigarettes in the same amount after the increase in price, it

would be said that the tax incidence fell entirely on the buyers.

55.

5252 | Pa g

e

SESSION 2:

Develop a subsidy framework for municipal rates and tariffs

that encourages efficient and effective use of resources

while promoting equity.

Learning Outcomes

The need for subsidies is identified at a municipal level.

An indigent policy for payment is developed which is legislatively compliant and

municipally specific

The socio-economic impact is calculated for a subsidy framework

A range of subsidy designs is applied and control instruments are designed for

"subsidy leakages".

Information sets are developed to manage an effective subsidy framework

2.1. The need for subsidies

A municipality should base its decisions about target options on its knowledge of local

conditions. There are at least seven steps that will aid the decision-making process. One

set of decisions often needs to be informed by another, making the process long,

cyclical and difficult.

TYPE OF SERVICE

The municipality should define precisely the levels of service it wishes to subsidise based

on its knowledge of the pressing service needs of the population in its jurisdiction. This

decision should also be informed by the amount of resources available for targeted

subsidies.

TARGET GROUPS

The municipality should decide who is most severely affected by a lack of access to

services. It should then identify and assess the available information sets that will help to

identify the beneficiaries. If the municipality requires other information, it must work out

how it will collect it. The municipality should also understand its own ability to analyse

and manipulate data. Using all the collected information, the target group can then be

rigorously defined.

56.

5353 | Pa g

e

The way the target is defined determines the size of the beneficiary group. The definition

of the target group should also be informed by the size of the available budget. The

municipality will have to make trade-offs on the accuracy of targeting using the

information it has available (and resources for collecting more information), and the size

of the target based on the budget it has available for targeting.

BUDGET FOR THE SUBSIDY

Municipalities can draw resources for targeting from existing sources:

the equitable share, CMIP grants and other capital grants;