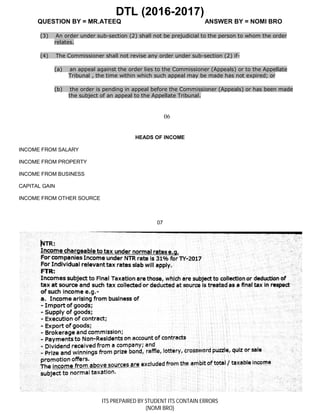

This document contains sections from Pakistan's Income Tax Ordinance relating to income tax returns, appeals, assessments, and definitions of taxable income. It discusses requirements for individuals and companies to file annual income tax returns under sections 114 and 115, including circumstances where returns are not required. Section 116 covers requirements to file annual wealth statements declaring assets and expenditures. The document is a study guide prepared by Nomi Bro in response to questions from Mr. Ateeq, and notes that it may contain errors as it was prepared by a student.

![Income tax-notes [compatibility mode]](https://cdn.slidesharecdn.com/ss_thumbnails/income-tax-notescompatibilitymode-180105070813-thumbnail.jpg?width=640&height=640&fit=bounds)