1. The Motives Behind Russia’s Gas Export Strategy: An Economic

Assessment of the Nord Stream Project’s Effect on Gazprom Profit

Roman Kucinskij roman.kucinskij.09@abdn.ac.uk +44 (0) 751-8520-558 www.abdn.ac.uk

MSc (Econ) International Business, Energy and Petroleum , University of Aberdeen, Aberdeen.

Background and Research Motivation

It is difficult to underestimate the influence Russia has over

the European gas market. Serving over 27% of European

natural gas market in 2009, Gazprom enjoys a dominant

position in the European gas supply.

Historically, Russia’s behaviour was difficult to predict,

particularly when energy resources are used as a political

tool. Gas disputes with Ukraine in 2006 and 2009 and

Belorussia in June this year are clear examples of this.

Better understanding of Russia’s and Gazprom’s motives

may lay the foundation for better anticipation of Russia’s

actions in the future.

Since Gazprom is a state monopoly and effectively

represents Kremlin policy, the motives behind Gazprom gas

exports strategies and the potential effect of the Nord

Stream pipeline on these strategies were investigated.

Methodology

Strategic and Capital budgeting analyses were undertaken.

Strategic analysis used a simple static numerical

optimisation model, allowing analysis of the Russian gas

transportation choices through various transit countries

Capital budgeting analysis considered net present cash

flows and cost savings associated with the Nord Stream

Project

Main Results

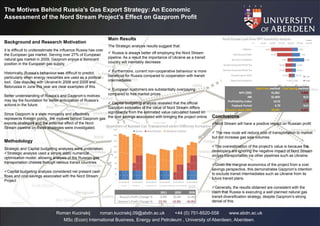

The Strategic analysis results suggest that:

Russia is always better off employing the Nord Stream

pipeline. As a result the importance of Ukraine as a transit

country will inevitably decrease.

Furthermore, current non-cooperative behaviour is more

beneficial for Russia compared to cooperation with transit

intermediates.

European customers are substantially overpaying

compared to free market prices

Capital budgeting analysis revealed that the official

Gazprom estimates of the value of Nord Stream differs

significantly from the estimated value calculated based on

the cost savings associated with bringing the project online. Conclusions

Nord Stream will have a positive impact on Russian profit

The new route will reduce cost of transportation to market

but not increase gas sale volumes.

The overestimation of the project’s value is because the

developers are ignoring the negative impact of Nord Stream

on gas transportation via other pipelines such as Ukraine.

Given the marginal economics of the project from a cost

savings perspective, this demonstrates Gazprom’s intention

to exclude transit intermediates such as Ukraine from its

future transit plans.

Generally, the results obtained are consistent with the

claim that Russia is executing a well planned natural gas

transit diversification strategy, despite Gazprom’s strong

denial of this.

33 33 33 33

27.5

27.5

27.5

133

106

95

78

81

65

33 33 33 33

55

55

55

128

73

93

76

65

49

33 33 33 33

55

55

55

123

68

90

73

62

46

0

20

40

60

80

100

120

140

160

180

201120202030 201120202030 201120202030 201120202030 201120202030 201120202030

UKR+BY UKR+BY+NS Consortium UKR Consortium UKR+BY Consortium UKR+NS Consortium

UKR+BY+NS

Bcm

Yamal Nord Stream Ukrainian Volume

1.0%

7.0%

1.0%

15.0%

10.0%

15.0%

1.0%

8.0%

13.0%

4.0%

30.0%

25.0%

25.0%

5.0%

$- $5.00 $10.00 $15.00 $20.00 $25.00 $30.00

Inflation

Realdiscount Rate

Gas Price Escalation

RussianCorporate Profit Tax

German Corporate Profit Tax

RussianExport Tariff

Opex Cost Escalation

$ Billions

Low

High

Cash Flow method Cost Saving method

NPV ($M) 41,061 -9,068

IRR 32.40% N/A

Profitability index 14.55 -1.99

Payback Period 6.70 N/A

Russia's share ($M) 20,941 -4,625