Downloaded 376 times

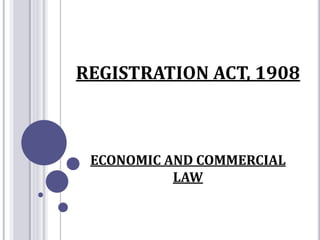

![CLASSIFICATION OF

REGISTRABLE DOCUMENTS

Documents

Registration

Optional

[Sec. 18]

Registration

Compulsory

[Sec. 17]](https://image.slidesharecdn.com/registrationact-170206165715/85/Registration-Act-1908-7-320.jpg)

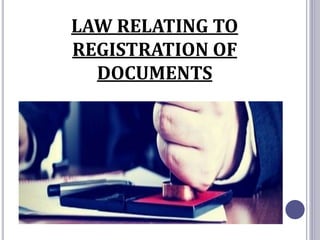

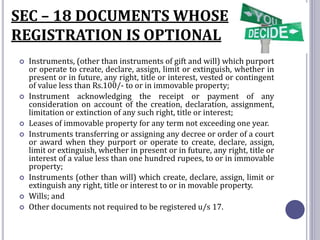

![SEC. 17 - DOCUMENTS WHOSE

REGISTRATION IS COMPULSORY

a. Instruments of gift of immovable property.

b. Other non-testamentary instruments [Other than

instruments of Gift of immovable property]

c. Non-testamentary instruments which purport to

create, declare, assign, limit or extinguish, whether in

present or in future, any such right, title or interest

whether vested or contingent, of the value of Rs.

100/- and above.

d. Leases of immovable property from year to year or

any term exceeding one year or reserving a yearly

rent.

e. Non-testamentary instruments transferring or

assigning any decree or order of a court or any award

in order to create interests as mentioned in clause (c).](https://image.slidesharecdn.com/registrationact-170206165715/85/Registration-Act-1908-8-320.jpg)

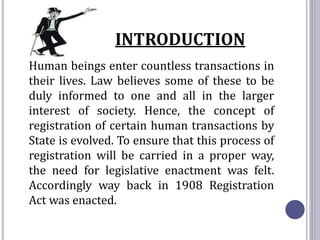

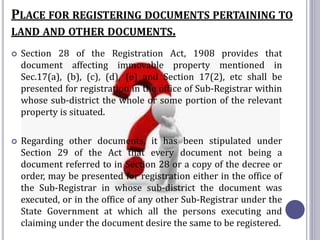

![REGISTRATION OF DOCUMENTS RELATES BACK TO

THE DATE OF THEIR EXECUTION.

Section 47 of the Registration Act, 1908 provides that a

registered document shall operate from the time which it

would have commenced to operate if no registration thereof

had been required or made, and not from the time of its

registration. This means registration of a document relates

back to the date of its execution.

In K.J. Nathan v. S.V. Maruthi Rai, AIR 1965 SC 430, the

Supreme Court laid down that as between two registered

documents, the date of execution determines the priority. Of

the two registered documents, executed by same persons in

respect of the same property to two different persons at two

different times, the one which is executed first gets priority

over the other, although the former deed is registered

subsequently to the later one.

In effect section 47 means that a document operates the date

of execution [as between the parties].

Case Law : Gurubux Singh Vs. Kartar Singh [2002] 2 SSC

611.](https://image.slidesharecdn.com/registrationact-170206165715/85/Registration-Act-1908-16-320.jpg)

The document summarizes the key aspects of the Registration Act of 1908 in India. It discusses (1) why the act was introduced - to record certain transactions and prevent fraud, (2) the classification of registrable documents into those requiring compulsory registration and those where registration is optional, (3) the time limits for registration, and (4) the effects of non-registration of documents that are required to be registered.