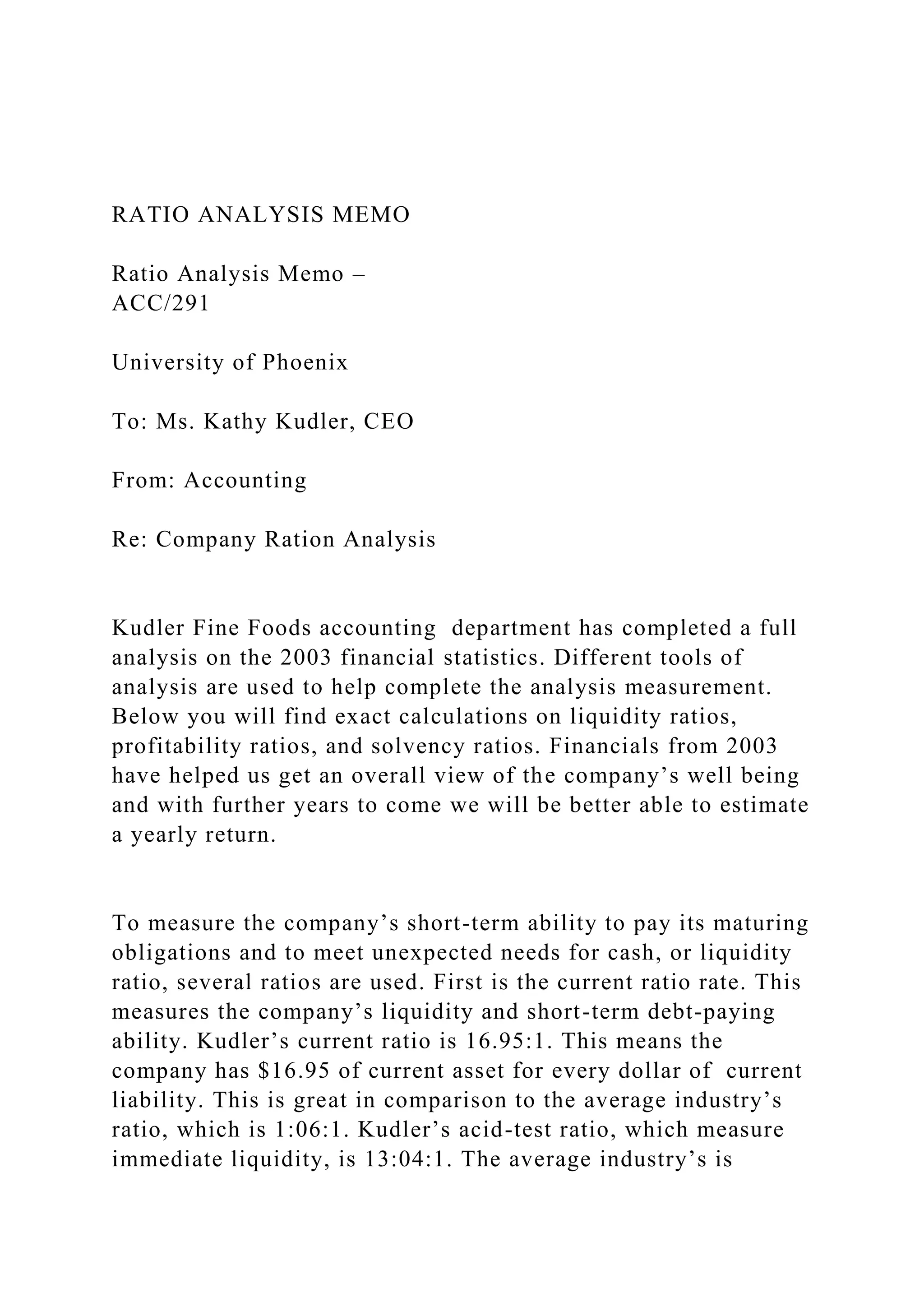

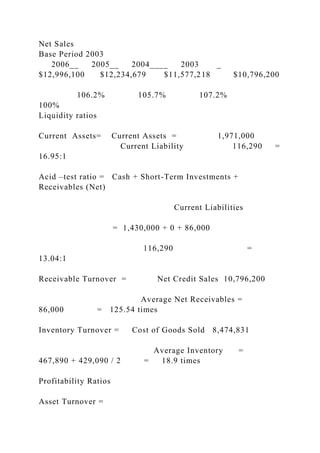

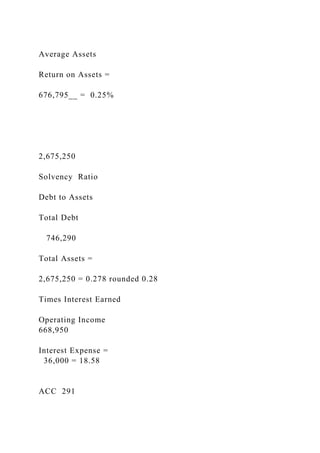

The memo provides a comprehensive ratio analysis of Kudler Fine Foods' 2003 financial statistics, highlighting strong liquidity ratios, profitability ratios, and solvency ratios that indicate the company's overall financial health. Key findings include a current ratio of 16.95:1 and an acid-test ratio of 13.04:1, demonstrating excellent short-term financial stability, along with a profit margin of 6.7% and a return on assets of 25.3%. While the company exhibits robust financial metrics, concerns are raised regarding its profitability performance, suggesting a need for improvement to ensure long-term sustainability.

![Academic Integrity A Letter to My Students[1] Bill T.docx](https://cdn.slidesharecdn.com/ss_thumbnails/academicintegrityalettertomystudents1billt-221203135336-8b2eba57-thumbnail.jpg?width=640&height=640&fit=bounds)