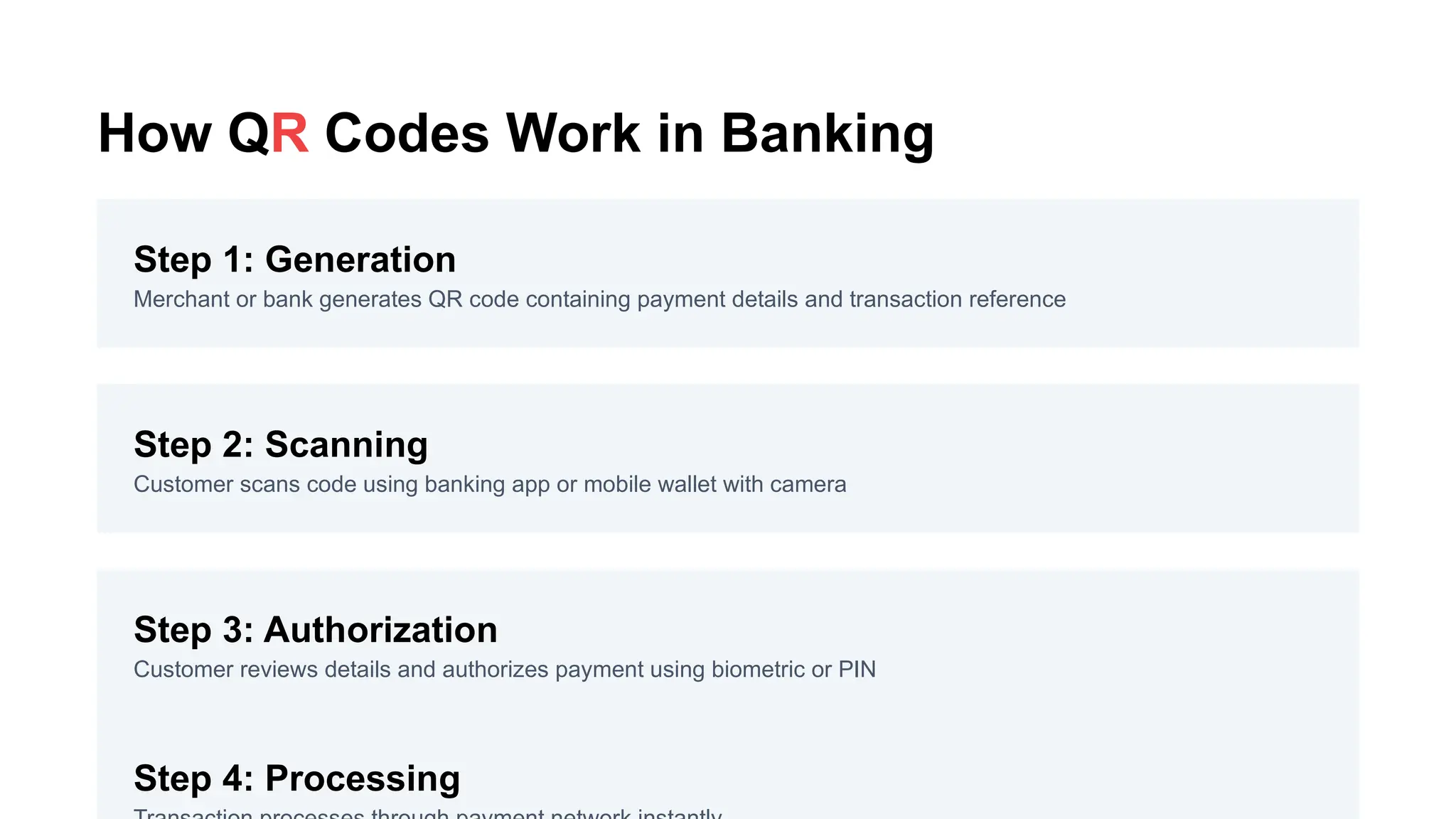

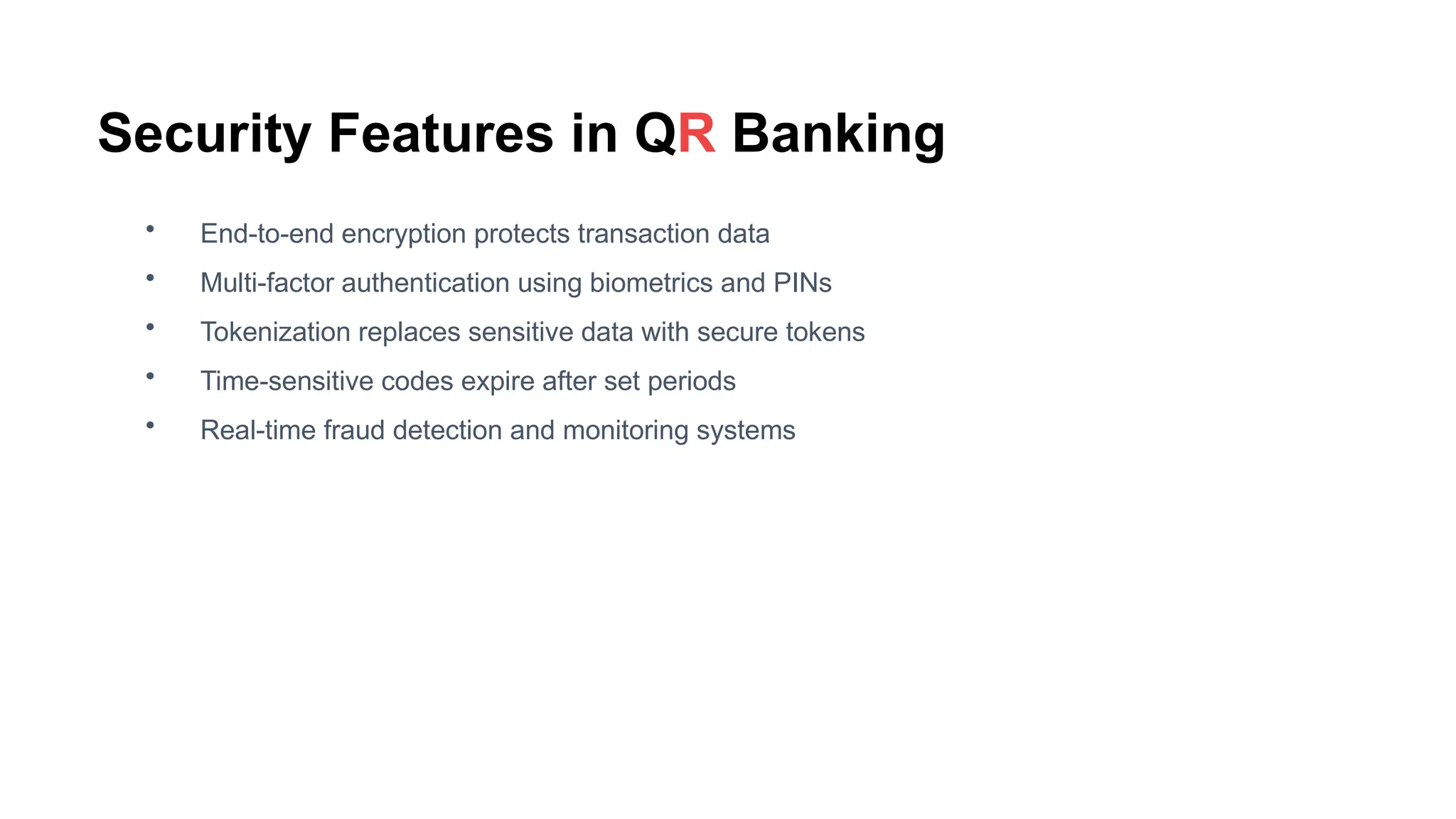

QR codes in banking are machine-readable codes that allow fast and secure data transfer between a bank’s system and a customer’s device.They are used to start payments, verify identity, connect accounts, or trigger specific actions like scanning for ATM withdrawals.

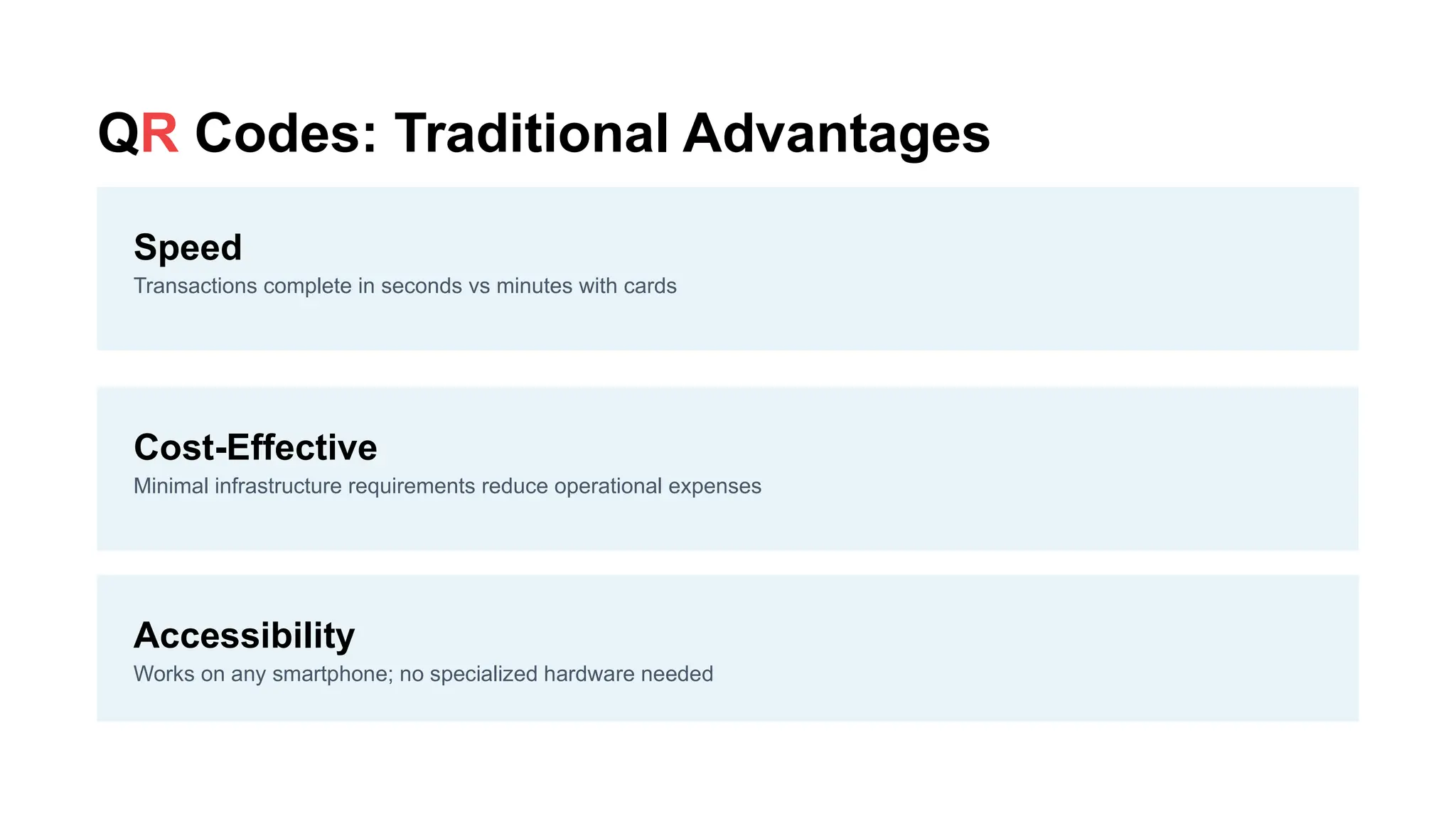

Banks use QR codes because they reduce friction.Customers don’t need cards, cash, or physical devices beyond their phone.A simple scan can begin a payment, confirm a transfer, or approve a transaction.

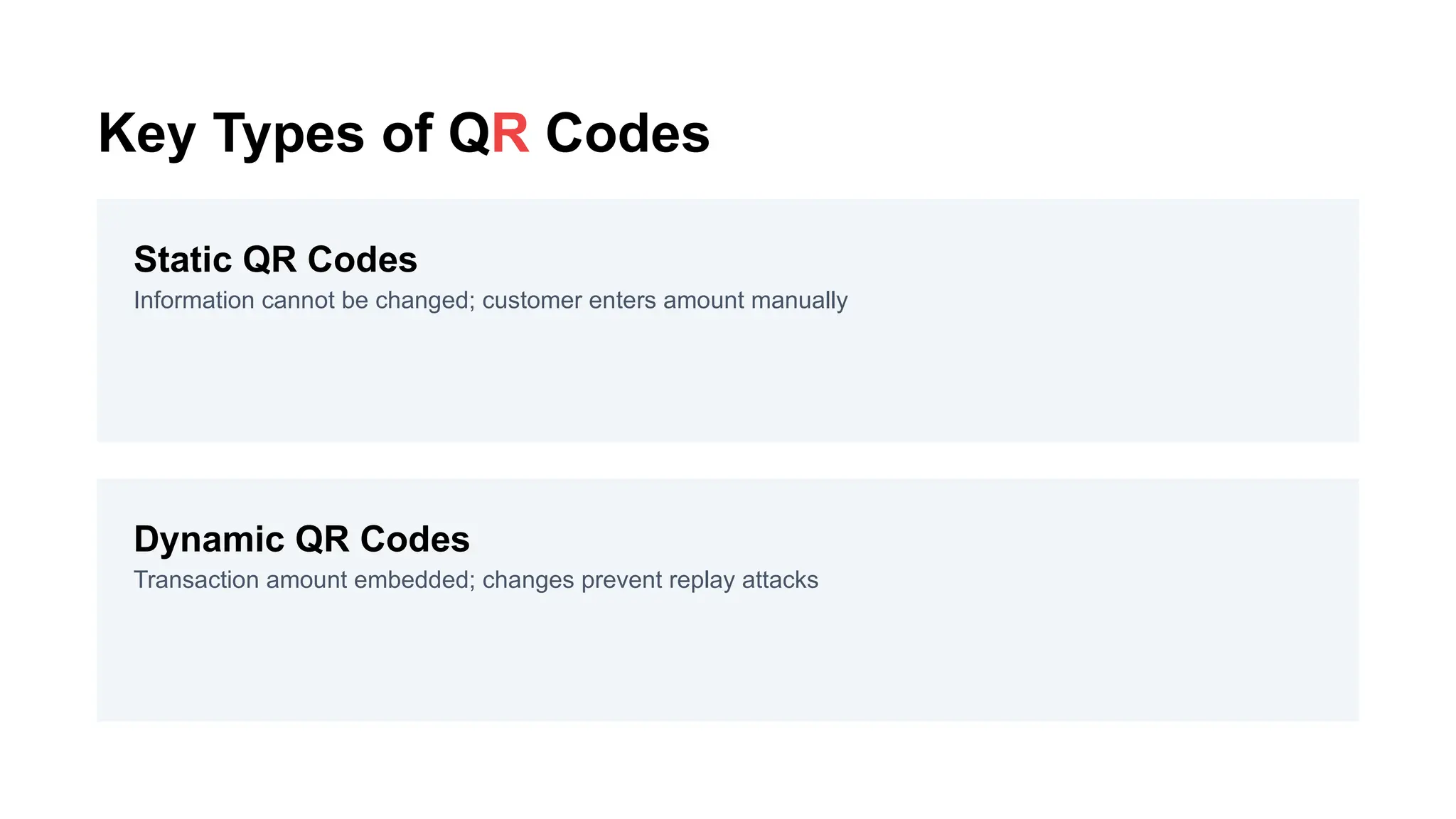

QR codes store information such as account details, transaction amounts, authentication tokens, or merchant data.The code format supports high-speed scanning and works even with damaged or partially obscured codes, making it reliable for crowded banking environments.

Most banking QR systems follow a standard format like UPI QR in India, EMVCo QR globally, or bank-specific QR formats.These standards ensure cross-bank compatibility, allowing customers from different banks to make payments using the same QR infrastructure.

QR codes support both in-person and remote banking.A merchant can display a printed QR code at a shop, or a bank can show a dynamic QR within an app to authenticate a login session.This flexibility makes QR codes a key element in modern banking, especially in regions with high mobile payment adoption.

![HOW DO QR CODES WORK? 8 STEPS TO CREATE YOUR CODES [GUIDE]](https://cdn.slidesharecdn.com/ss_thumbnails/howdoqrcodeswork-docs-221208092333-8965ab80-thumbnail.jpg?width=640&height=640&fit=bounds)