Protection against banking and financial frauds-1.pdf

1.

Protection against banking

andfinancial frauds

SUBMITTED BY : SOHIT KUMAR

HIMANSHU KUMAR

RAUSHAN KUMAR

RANJAN BARMAN

SUBMITTED TO : DR. PREETI DEVI

2.

Introduction

We arecurrently living in the era of digitalization. With the emergence of the internet,

the physical world has set foot into the digital world. India too is not behind in digitalizing

itself by promoting the "Digital India" campaign. Many industries like banking, insurance,

education, etc. are very keen on adopting digitalization. But nothing is perfect in this

world and the same is the case for digital payments as well i.e., with technology comes

vulnerability.

While digital payments offer timeliness and comfort, it is prone to fraud as well.

Nowadays we see so many headlines about people losing their hard-earned money to

financial fraud. The reason being people lack knowledge on how to differentiate

between a genuine offer and a financial offer. They are also not aware of the remedies

which the government has to offer to the public in such circumstances.

3.

Financial Frauds

Financialfraud is any intentional act of deception involving financial

transactions for illegal gain. It can include misrepresenting information, identity

theft, or misusing funds to wrongfully obtain money or assets from a victim.

Surveys and government data show a high incidence of financial fraud in India, with one

Local Circles survey indicating 47% of urban Indians faced financial fraud in the last three

years (as of mid-2024), and PwC reported 59% of organizations experienced financial

fraud in the past two years (as of late 2024). The total financial losses also show an

alarming trend, with the National Cyber Crime Reporting Portal (NCRP) recording over

₹22,000 crore in losses in 2024 alone, a significant increase from previous years.

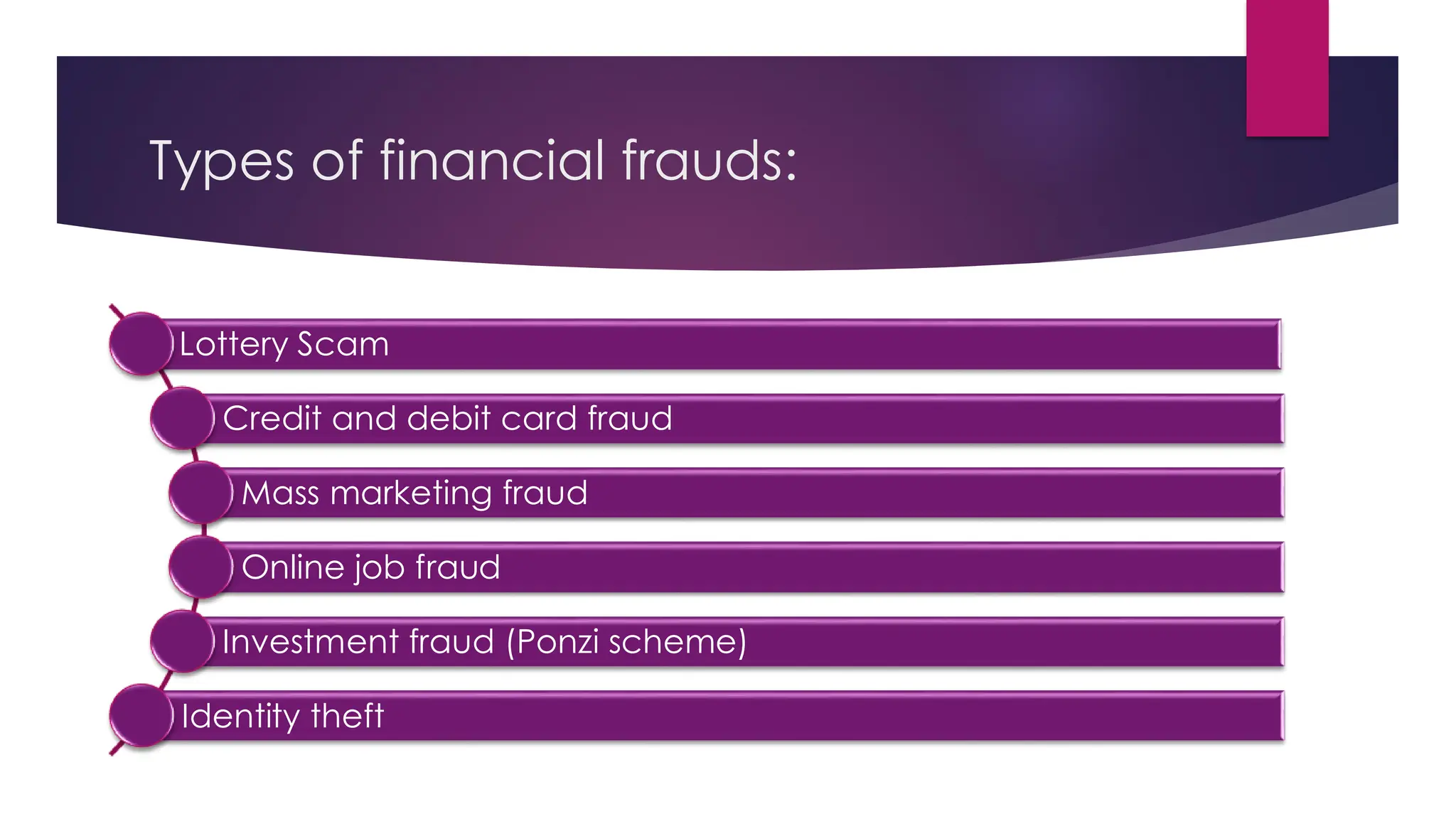

Types of financialfrauds:

Lottery Scam

Credit and debit card fraud

Mass marketing fraud

Online job fraud

Investment fraud (Ponzi scheme)

Identity theft

6.

Ponzi Schemes

APonzi scheme is a type of investment fraud where returns are paid to earlier

investors using the capital of newer investors, rather than from profit earned. The

scheme relies on a continuous influx of new money to keep the illusion of

profitability alive. Eventually, it collapses when there aren’t enough new investors

to pay returns, or when the operator can no longer maintain the illusion.

Named after Charles Ponzi, who became infamous for running this type of scam

in the early 20th century, these schemes are unsustainable and often lead to

significant financial losses for those involved.

7.

Identifying Ponzi schemes:

❖High returns with little or no risk

❖ Overly consistent returns.

❖ Unregistered investments

❖ Unlicensed sellers.

❖ Issues with paperwork

❖ Difficulty receiving payments

8.

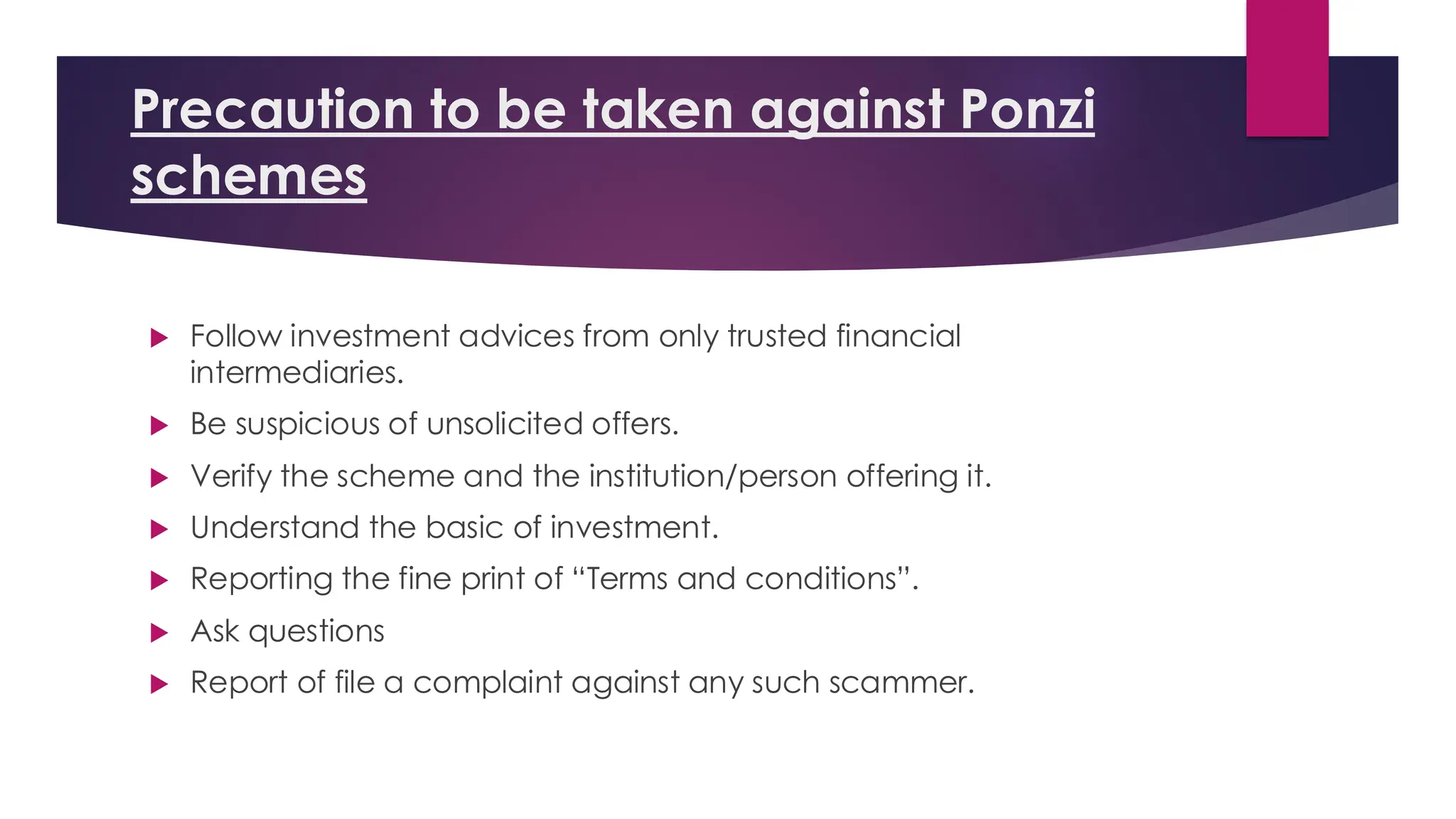

Precaution to betaken against Ponzi

schemes

Follow investment advices from only trusted financial

intermediaries.

Be suspicious of unsolicited offers.

Verify the scheme and the institution/person offering it.

Understand the basic of investment.

Reporting the fine print of “Terms and conditions”.

Ask questions

Report of file a complaint against any such scammer.

9.

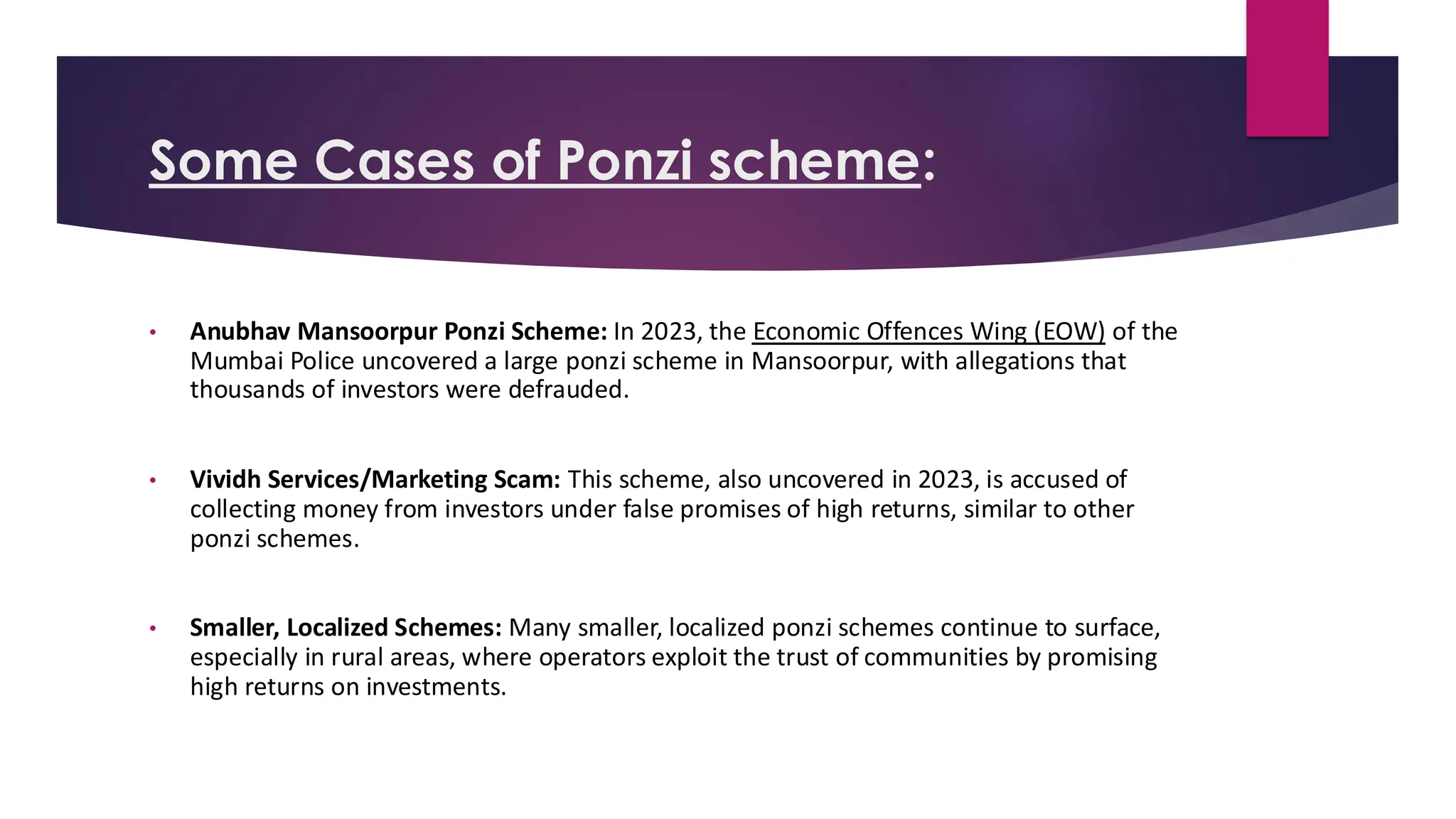

Some Cases ofPonzi scheme:

• Anubhav Mansoorpur Ponzi Scheme: In 2023, the Economic Offences Wing (EOW) of the

Mumbai Police uncovered a large ponzi scheme in Mansoorpur, with allegations that

thousands of investors were defrauded.

• Vividh Services/Marketing Scam: This scheme, also uncovered in 2023, is accused of

collecting money from investors under false promises of high returns, similar to other

ponzi schemes.

• Smaller, Localized Schemes: Many smaller, localized ponzi schemes continue to surface,

especially in rural areas, where operators exploit the trust of communities by promising

high returns on investments.

10.

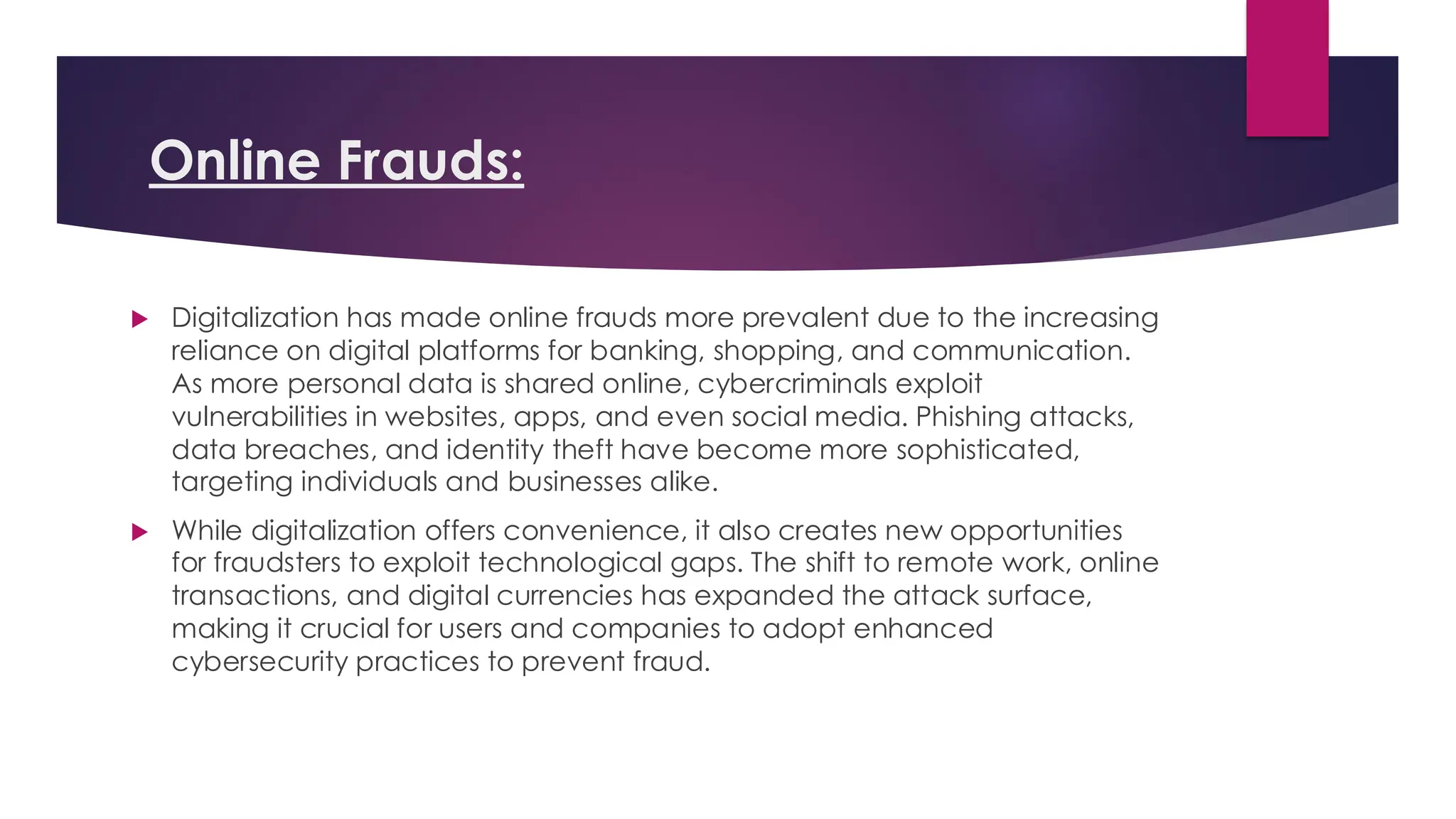

Online Frauds:

Digitalizationhas made online frauds more prevalent due to the increasing

reliance on digital platforms for banking, shopping, and communication.

As more personal data is shared online, cybercriminals exploit

vulnerabilities in websites, apps, and even social media. Phishing attacks,

data breaches, and identity theft have become more sophisticated,

targeting individuals and businesses alike.

While digitalization offers convenience, it also creates new opportunities

for fraudsters to exploit technological gaps. The shift to remote work, online

transactions, and digital currencies has expanded the attack surface,

making it crucial for users and companies to adopt enhanced

cybersecurity practices to prevent fraud.

11.

Online fraud surveyof last few years

42% Indians surveyed say they or someone in their family has been a victim

of financial fraud in the last 3 years.

• The first question in the survey asked citizens, “Have

you or someone in your immediate family been a

victim of financial fraud in the last 3 years?”

• In response, the 54% of citizens said “Thankfully, no

one”. However, 4% said “Yes, multiple members”,

and while 38% revealed “Yes, one of us in the

family”.

• On an aggregate basis, 42% of Indians surveyed

say they or someone in their family have been

victims of financial fraud in the last 3 years.

12.

Types of onlinebanking frauds

Phishing

Vishing

Frauds through unauthorized applications

Skimming

Sim Cloning

QR code scanners

Refund fraud

Impersonation or fake identity on Social media platforms

13.

Protection and securityagainst online frauds

To protect oneself from online fraud and incidents, “Awareness is the key”.

Some of the precautions and security actions that can be taken to avoid

online fraud are:

❖ Use only official and verified mobile phone applications.

❖ Use of a secure website

❖ Don’t share your passwords, bank details, or OTP(one-time password) with

strangers or financial intermediaries you don’t trust.

❖ Gather knowledge about different types of online fraud

❖ Avoid using public computers or wifi.

❖ Conduct research on the intermediary before sharing your details or

making an investment decision.

14.

According to RBI(Reservebank of India)

Steps to be taken in case you become one of the victims of online fraud:

You are required to notify your bank immediately. Upon receipt of such

intimation, the bank will resolve the complaint within 90 days of receiving

the complaint.

The bank is also required to reimburse the amount of loss, depending on

the negligence of the customer himself.

The reimbursement policy further depends on RBI guidelines, the bank's

board policy, and the time taken by the customer to notify the bank

about the fraud.

15.

Cybersecurity Measures byBanks

•Modern banks are increasingly investing in robust cybersecurity frameworks to protect customer data

and prevent fraud.

•Multi-Factor Authentication (MFA): Confirms user identity using passwords, OTPs, or biometrics.

•AI & Machine Learning: Detect suspicious activities and alert the bank in real time.

•Data Encryption: Secures sensitive information during online transactions.

•Regular Security Audits: Identify and fix potential vulnerabilities in banking systems.

•Dedicated Cyber Cells: Operate round the clock to monitor and address online financial crimes.

16.

Role of Governmentand Regulatory

Bodies

•The government and financial regulators play a crucial role in preventing and managing financial

frauds.

•Reserve Bank of India (RBI): Sets guidelines for secure digital payments and customer

protection.

•National Cyber Crime Reporting Portal (NCRP): Allows easy reporting of online frauds by

citizens.

•CERT-In: Investigates cybersecurity threats and provides early warnings.

•Ministry of Finance: Conducts awareness campaigns on safe banking practices.

•Digital India Mission: Promotes secure, inclusive, and transparent online financial systems.

17.

Public Awareness andEducation

•Awareness and digital literacy are essential to protect individuals from fraud.

•Organize workshops and campaigns in schools, colleges, and rural areas.

•Encourage citizens to verify links, offers, and messages before taking any

action.

•Support initiatives like “Think Before You Click” and “Never Share Your OTP.”

•Spread verified information about scams through social media and official

platforms.

•A well-informed public is the strongest defense against financial frauds.

18.

Future of FraudPrevention

•The future of financial safety lies in combining technology, awareness, and regulation.

•Blockchain Technology: Brings transparency and traceability in digital payments.

•Biometric Authentication: Strengthens identity verification using fingerprints or facial

recognition.

•AI-Driven Fraud Detection: Predicts and prevents suspicious activities automatically.

•Cross-Sector Collaboration: Banks, telecom firms, and law enforcement agencies working

together.

•Data Protection Laws: Implementation of the Digital Personal Data Protection Act 2023

ensures better privacy and accountability

19.

Conclusion

Protection againstfinancial frauds is essential to ensure the safety

of individuals, businesses, and the overall financial system. With

increasing digital transactions, awareness, vigilance, and the use of

secure technologies have become crucial. Strong regulations,

effective monitoring, and prompt reporting of suspicious activities

help reduce risks. By adopting safe practices, such as protecting

personal information, using secure banking channels, and staying

alert, individuals and institutions can safeguard themselves and

build trust in the financial system.