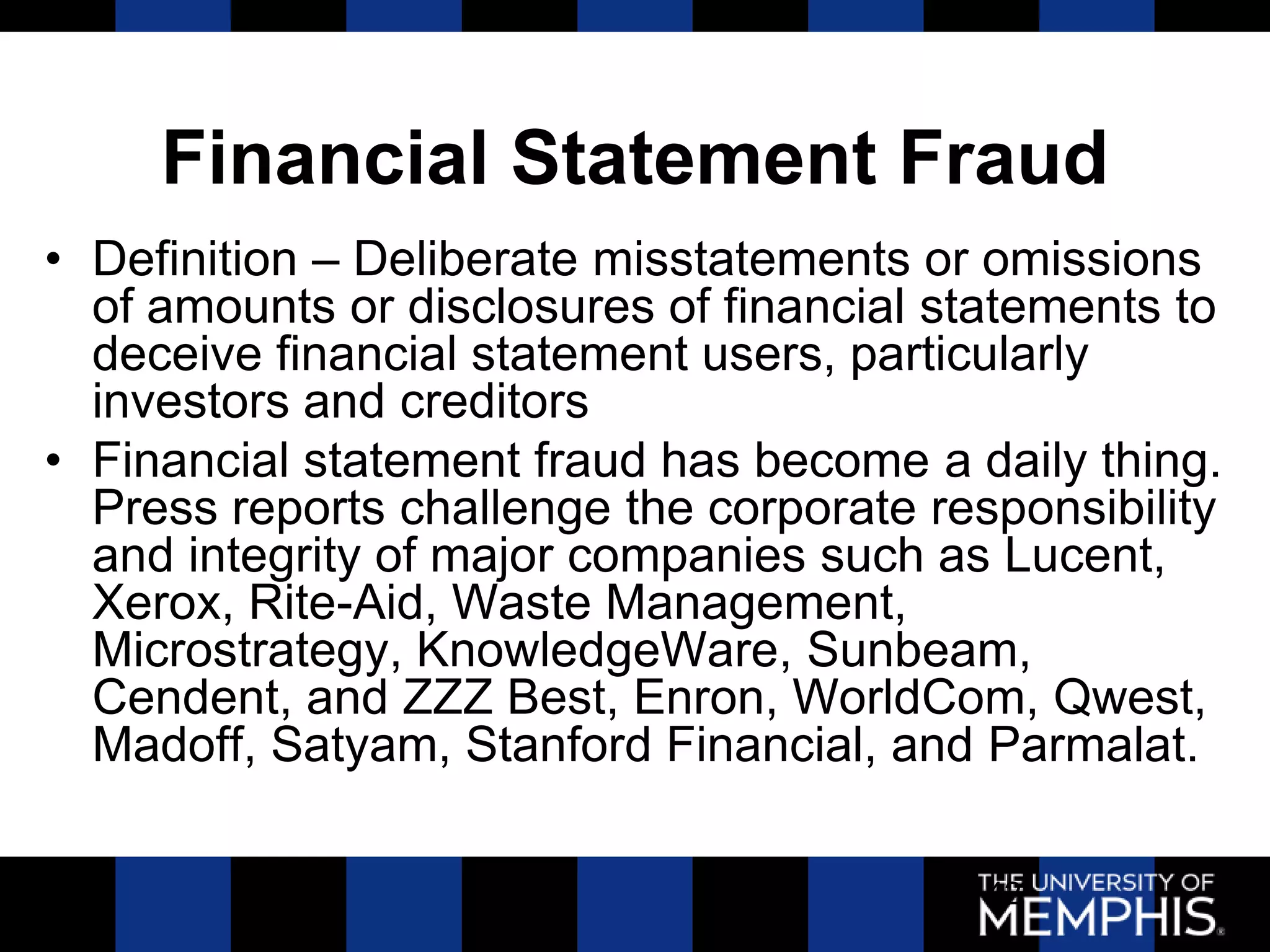

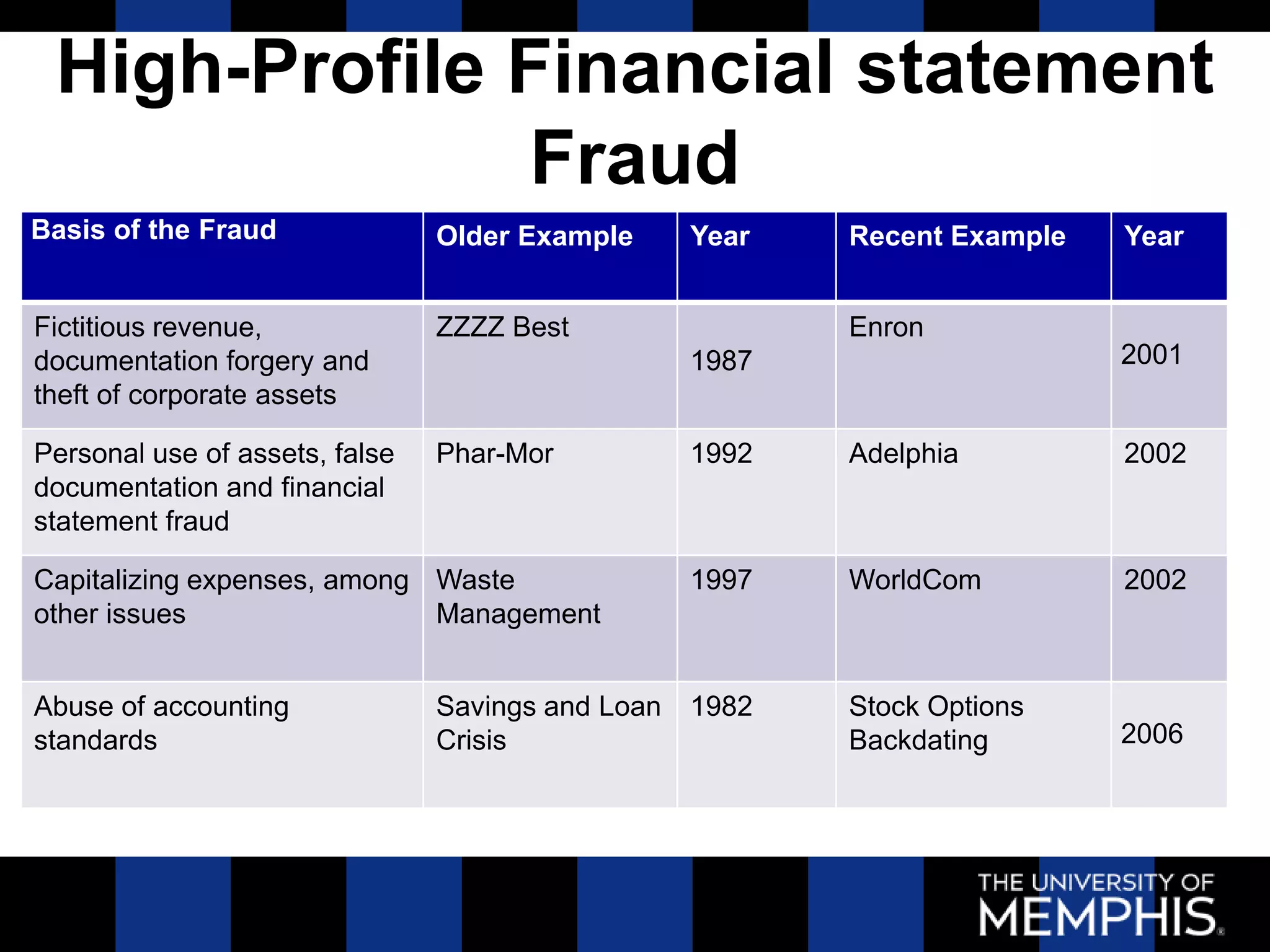

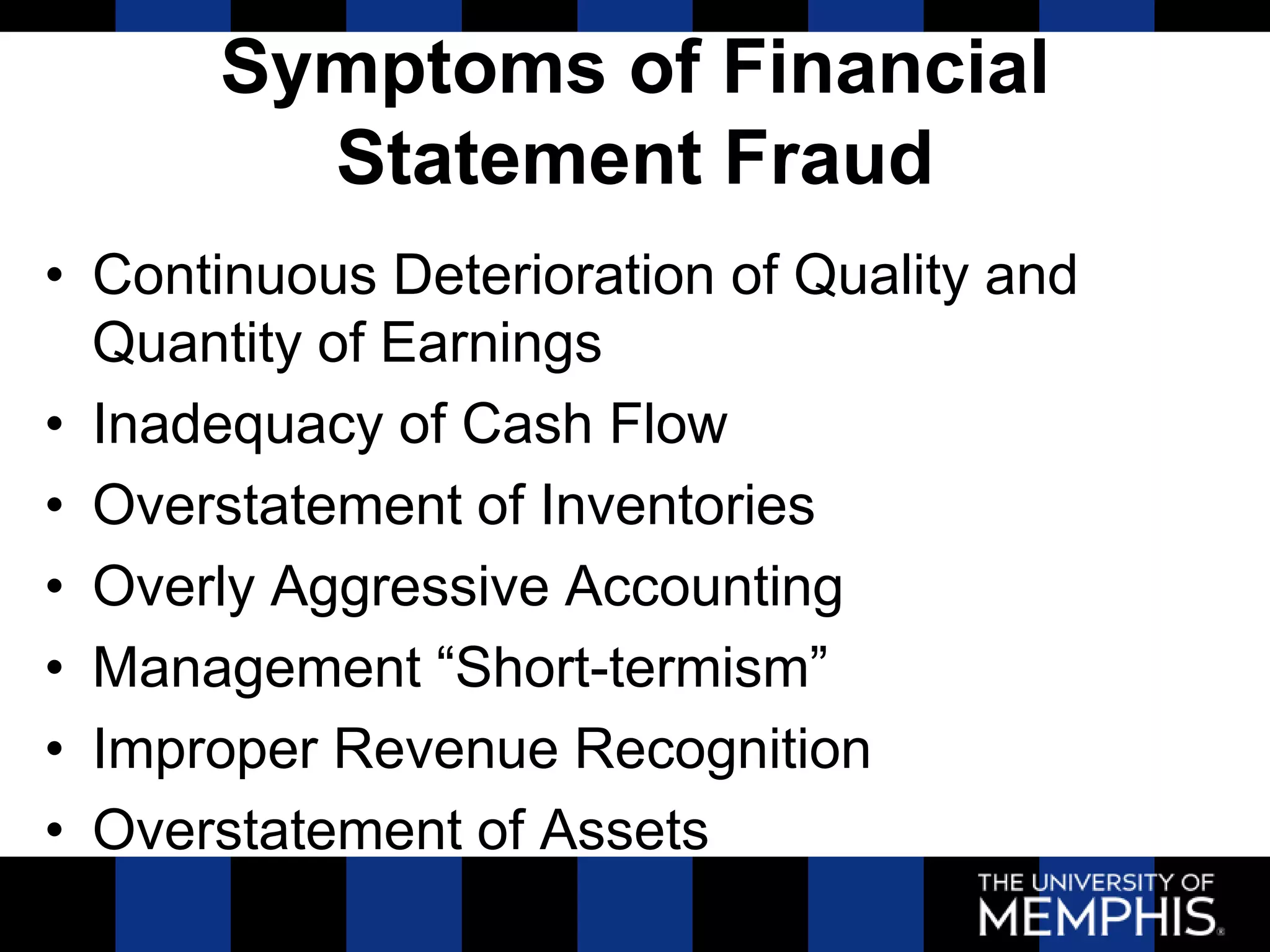

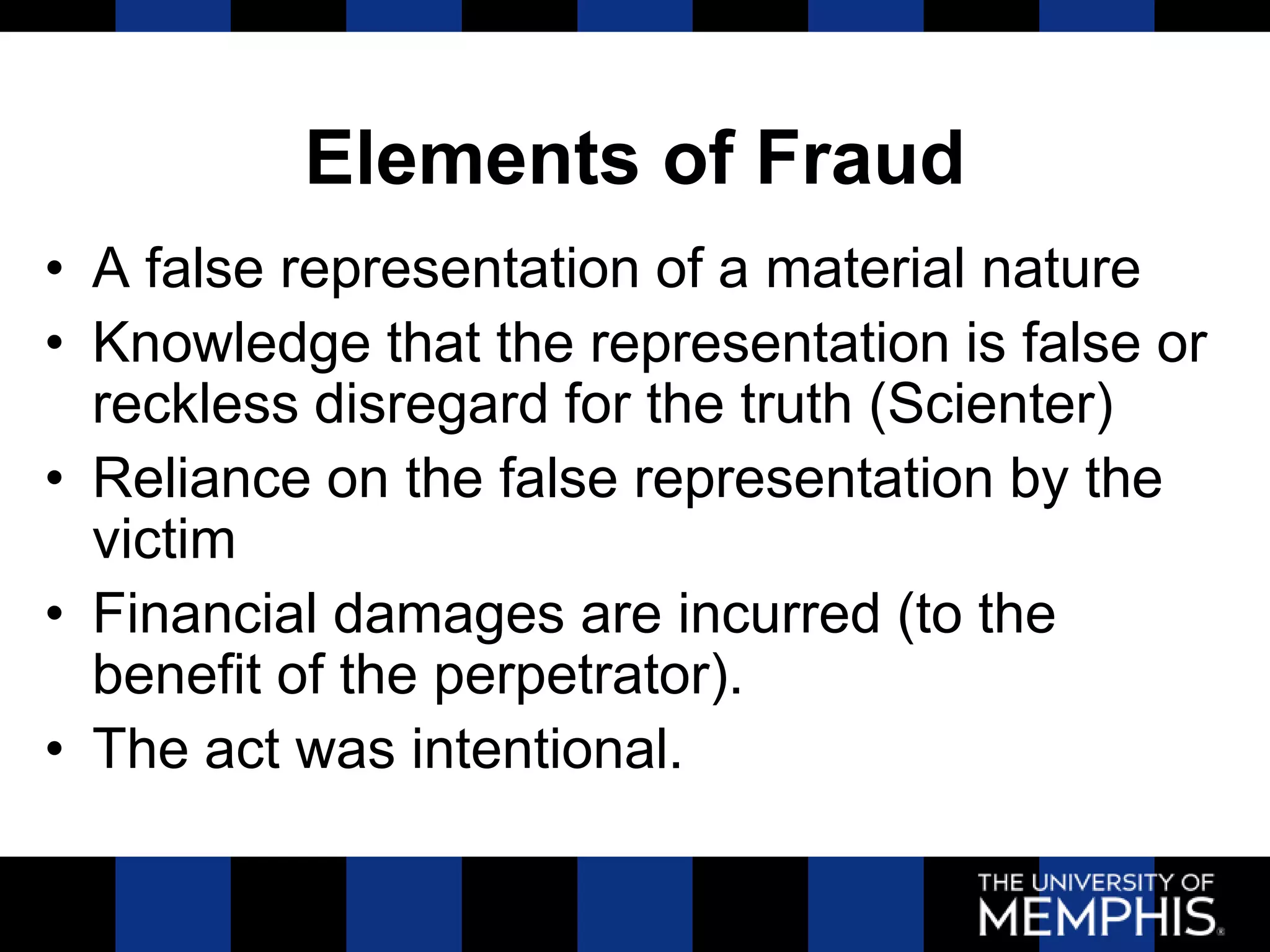

Downloaded 72 times

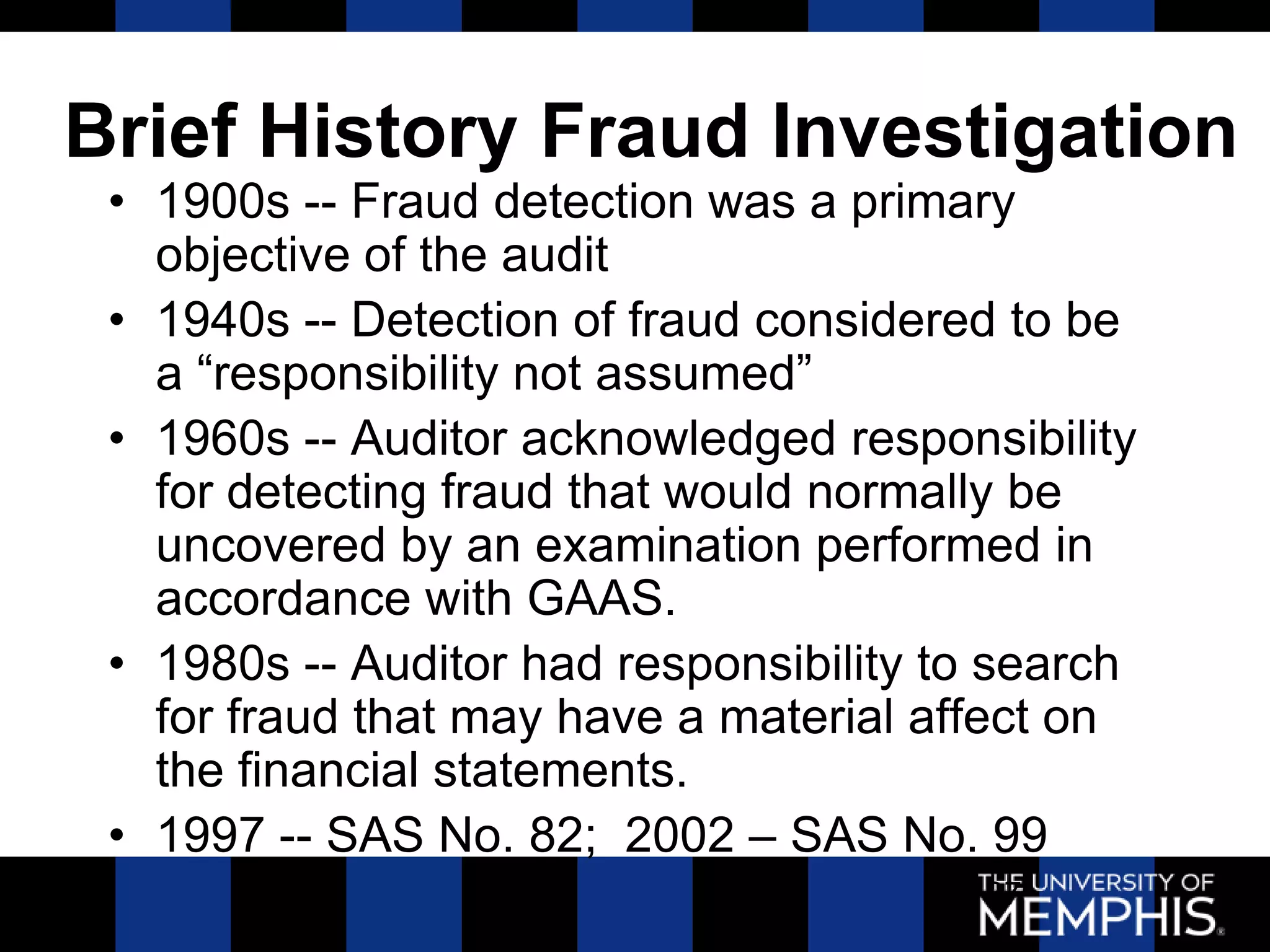

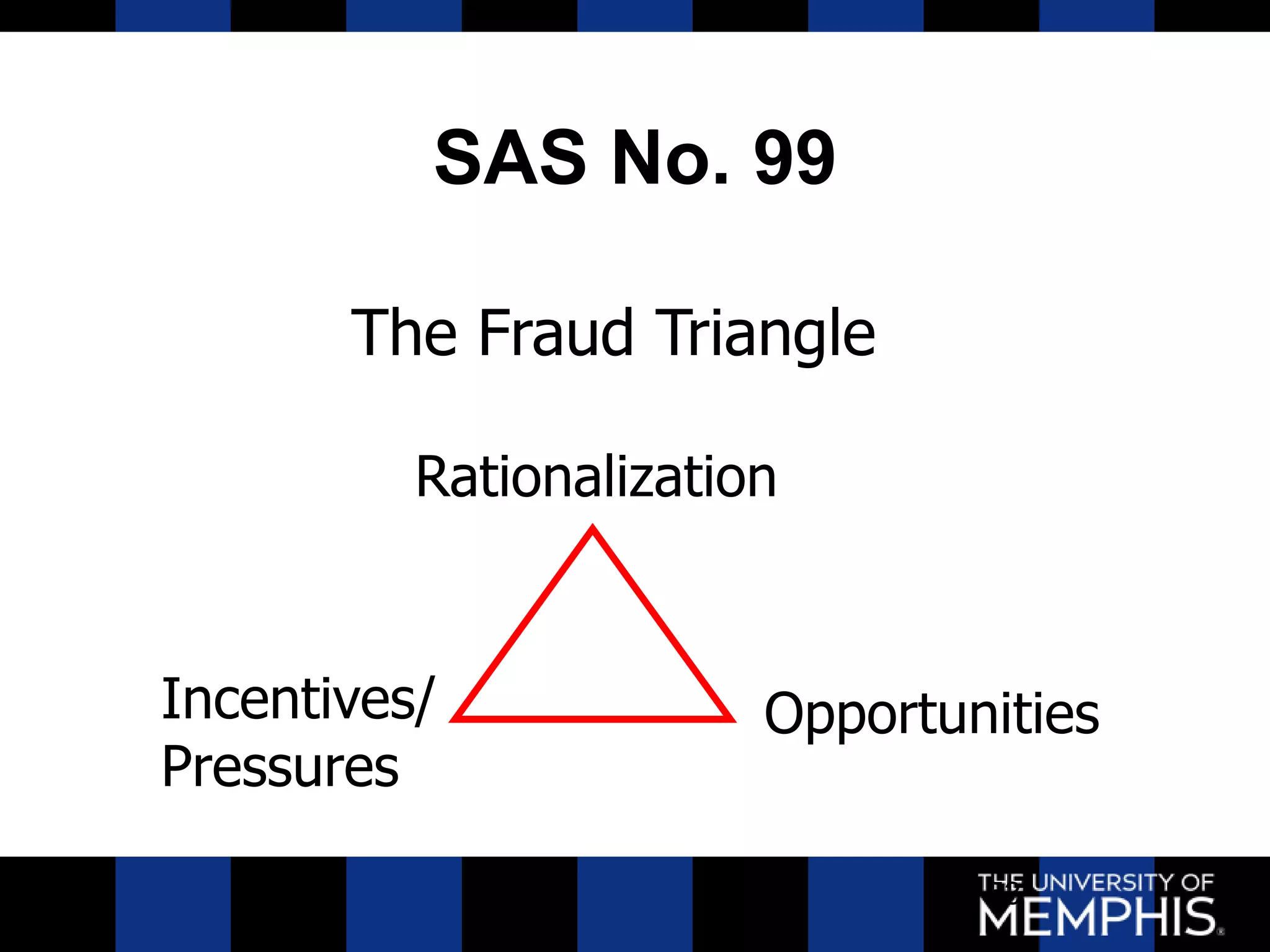

![Embezzlement Formula

MOTIVE +

OPPORTUNITY +

RATIONALIZATION =

CRIME [FRAUD]

40](https://image.slidesharecdn.com/presentationchapter9-121121011820-phpapp01/75/Presentation-chapter-9-40-2048.jpg)

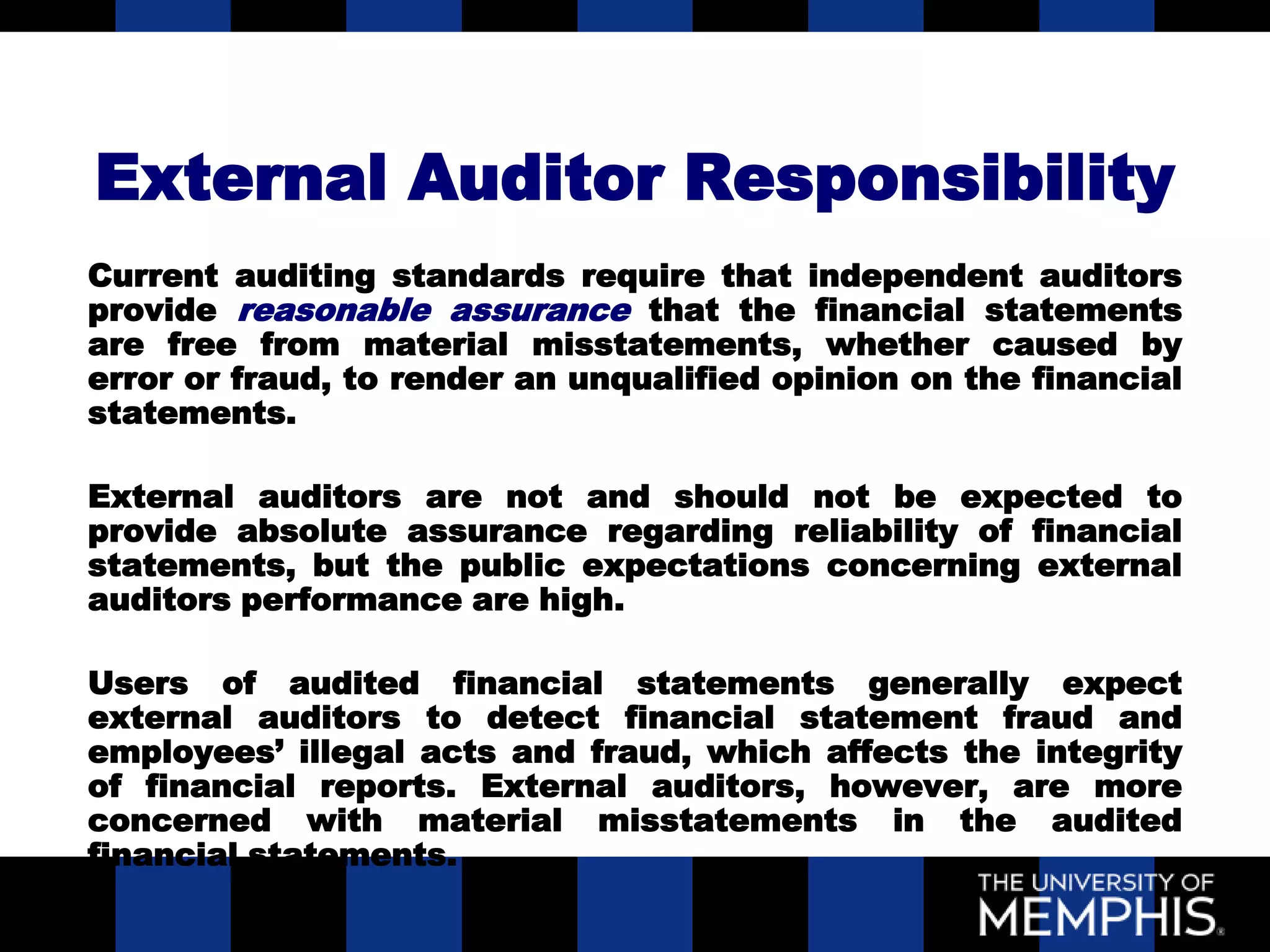

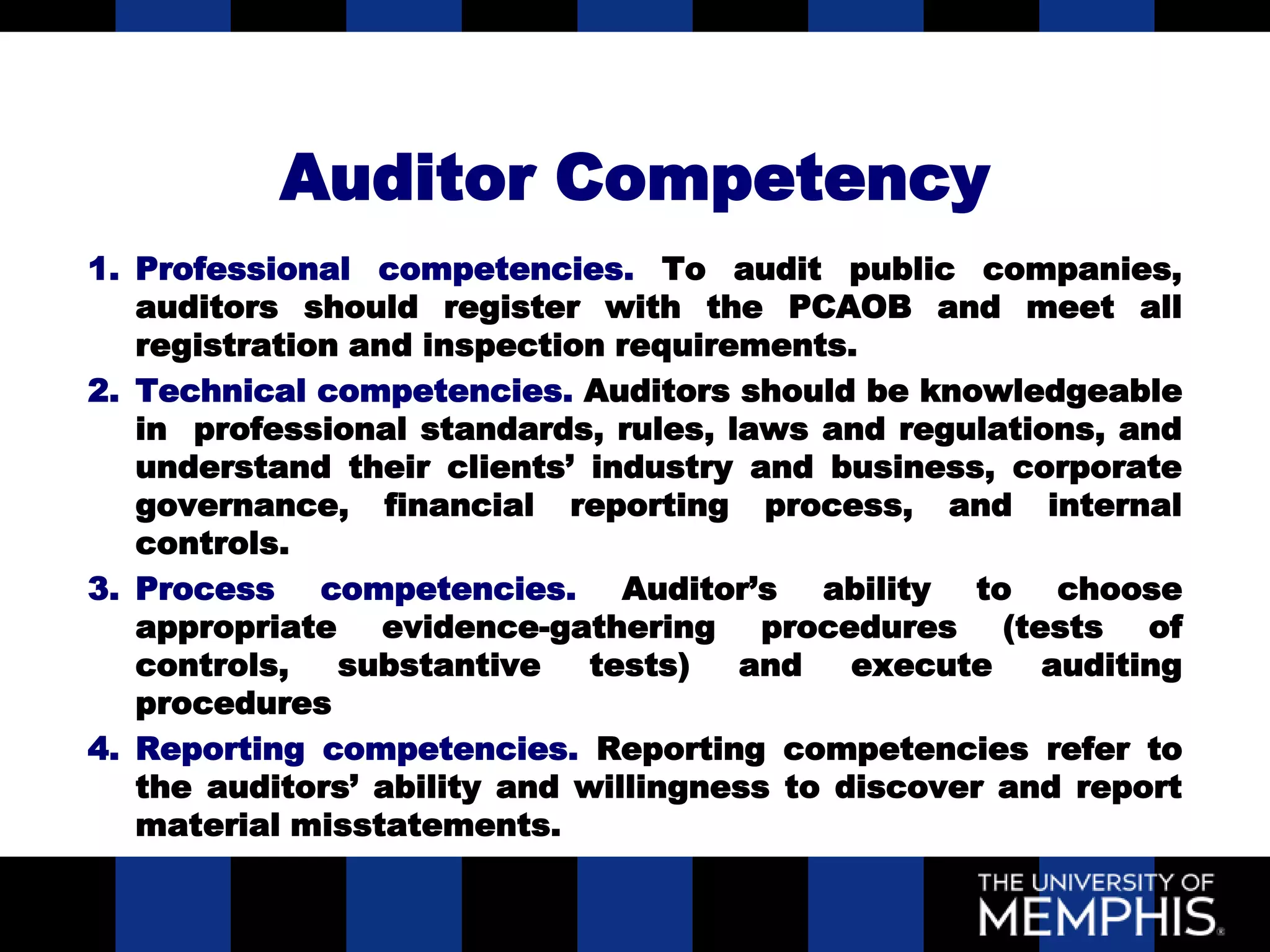

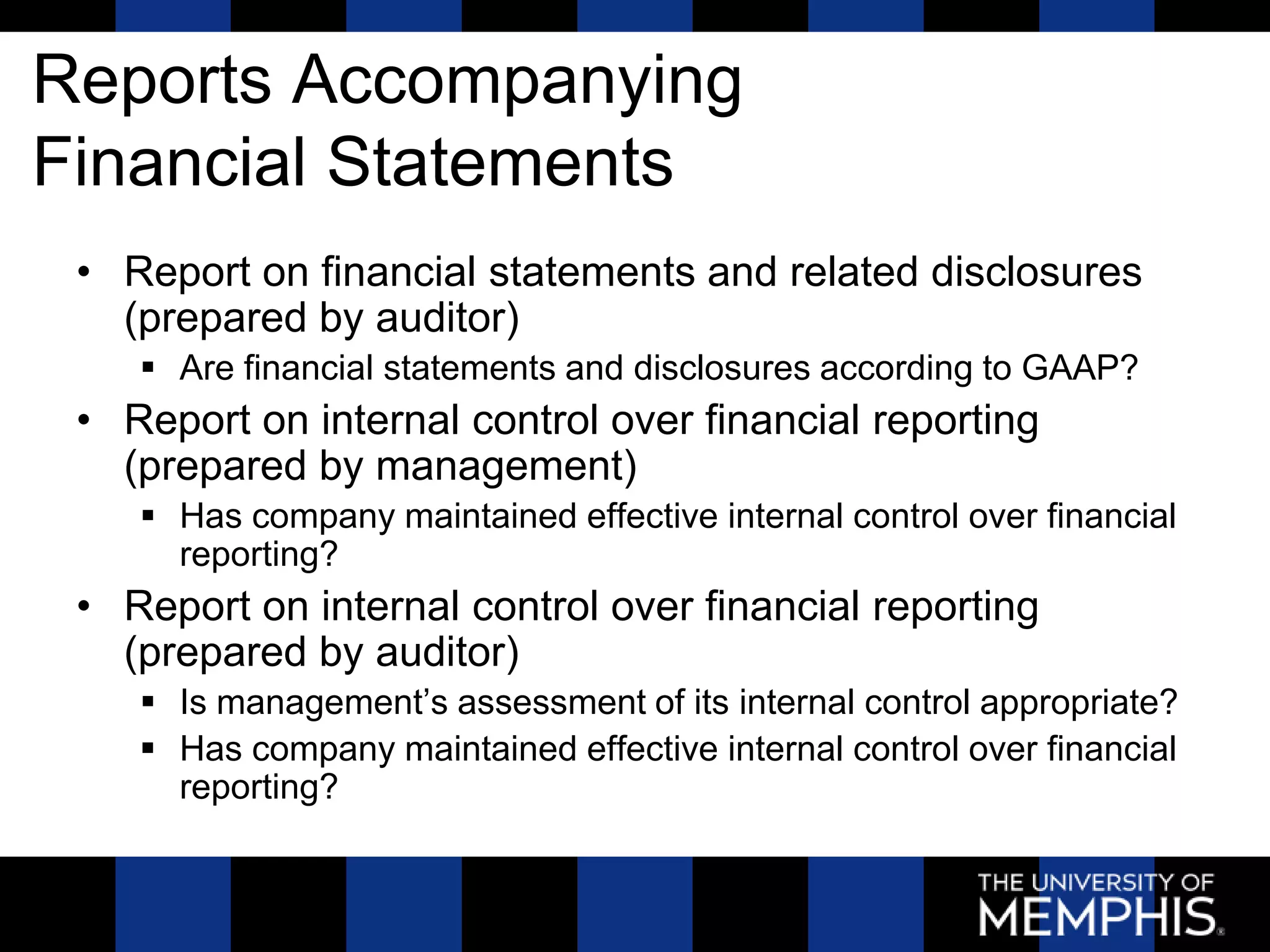

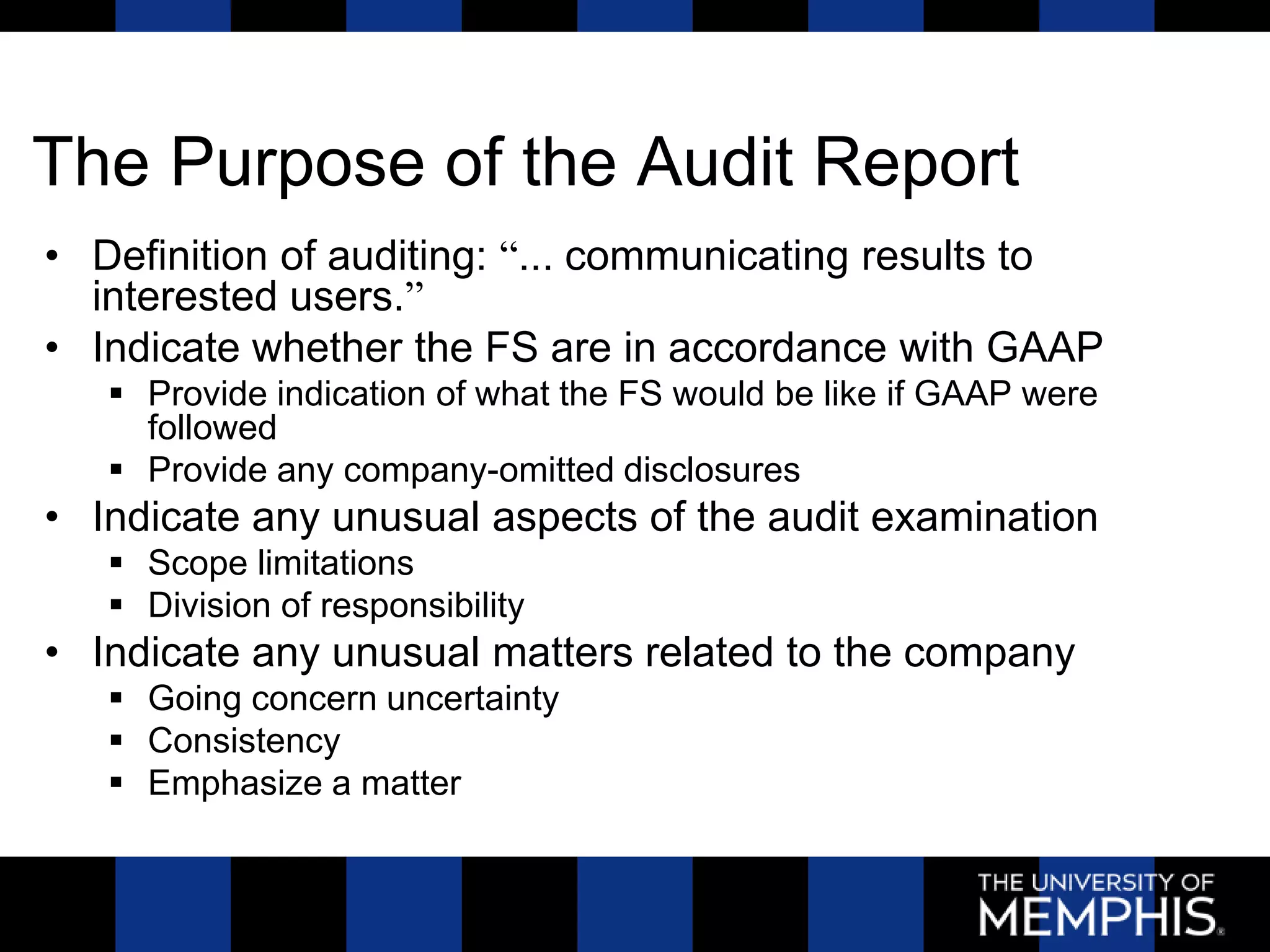

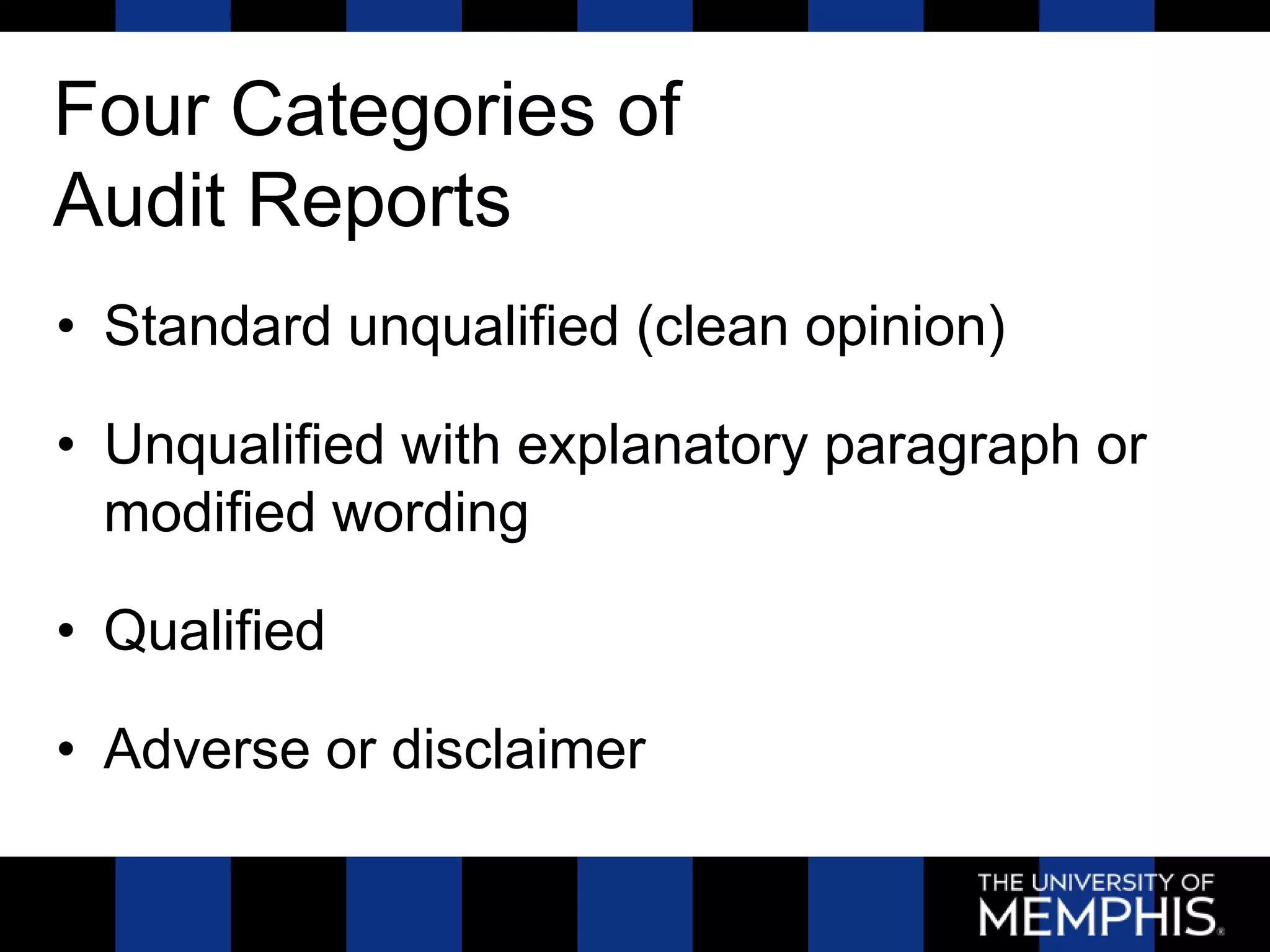

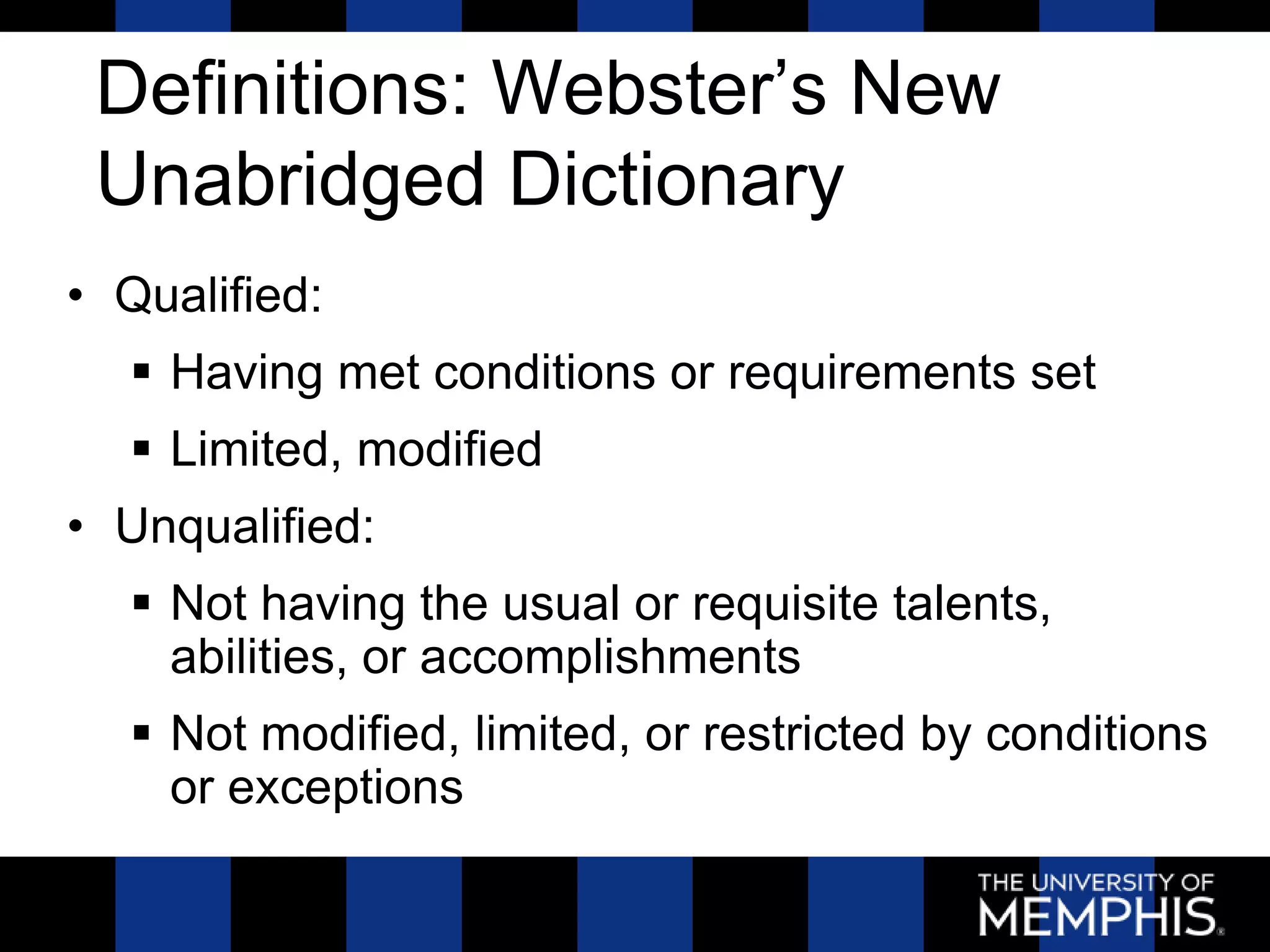

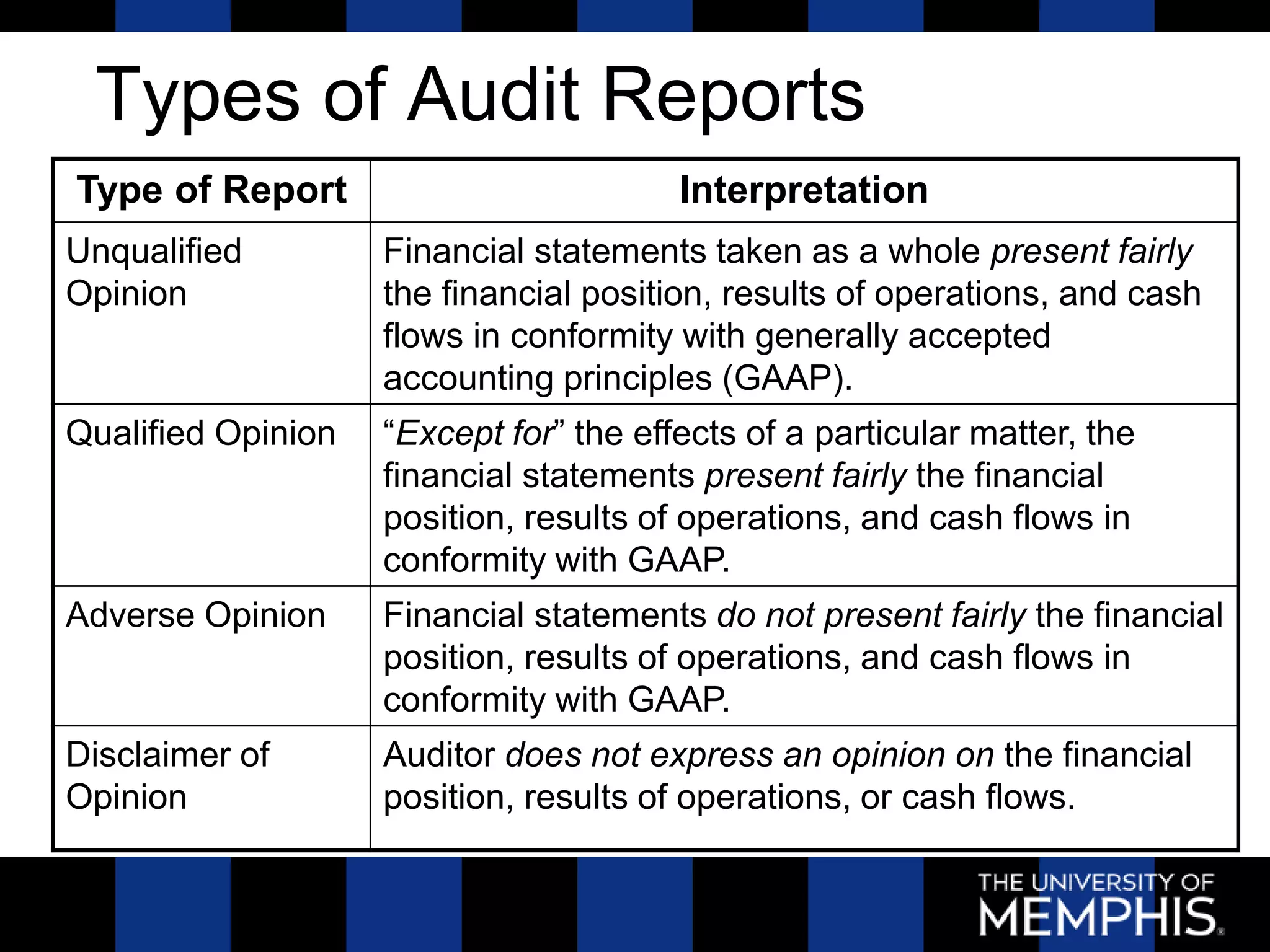

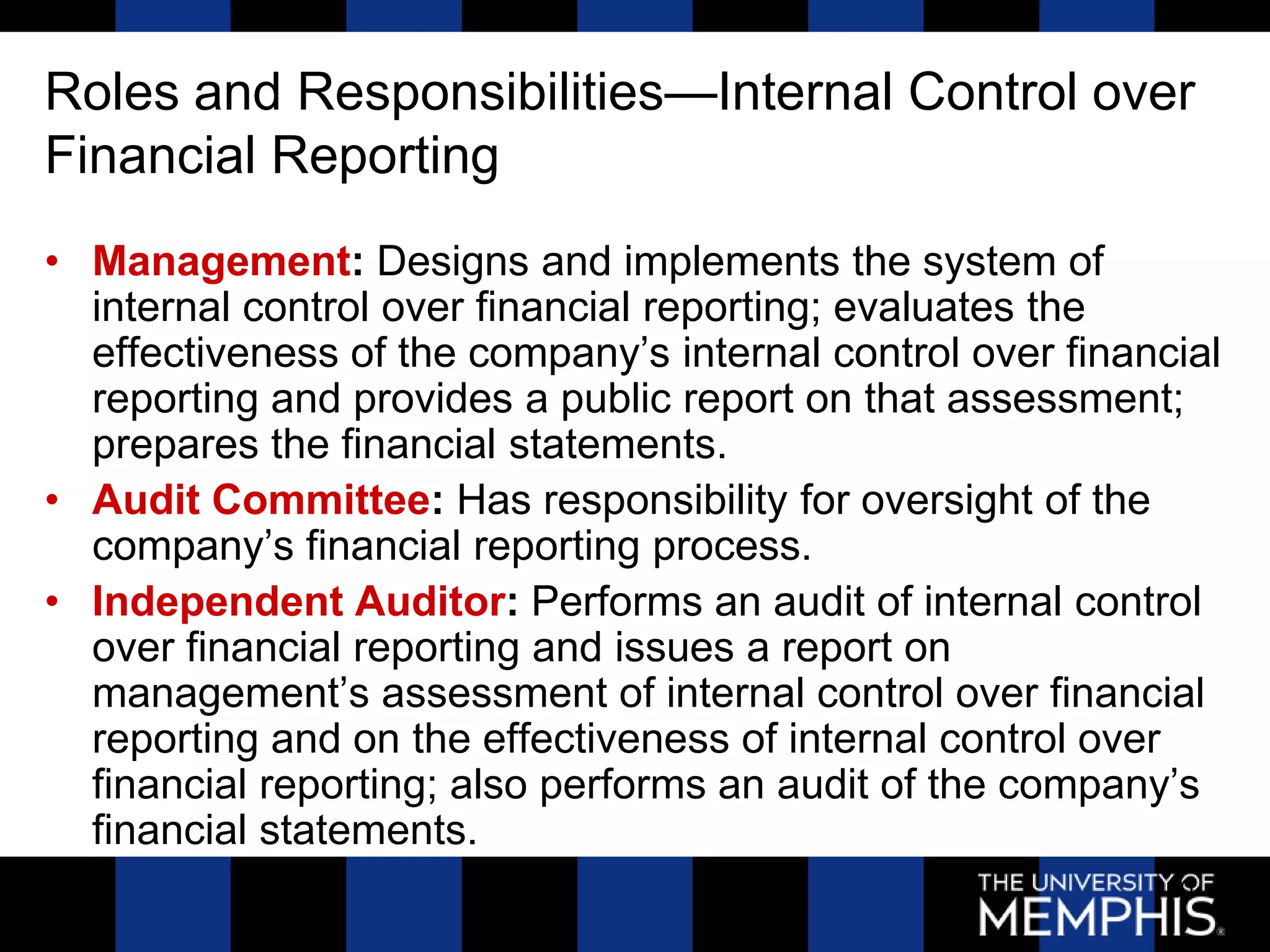

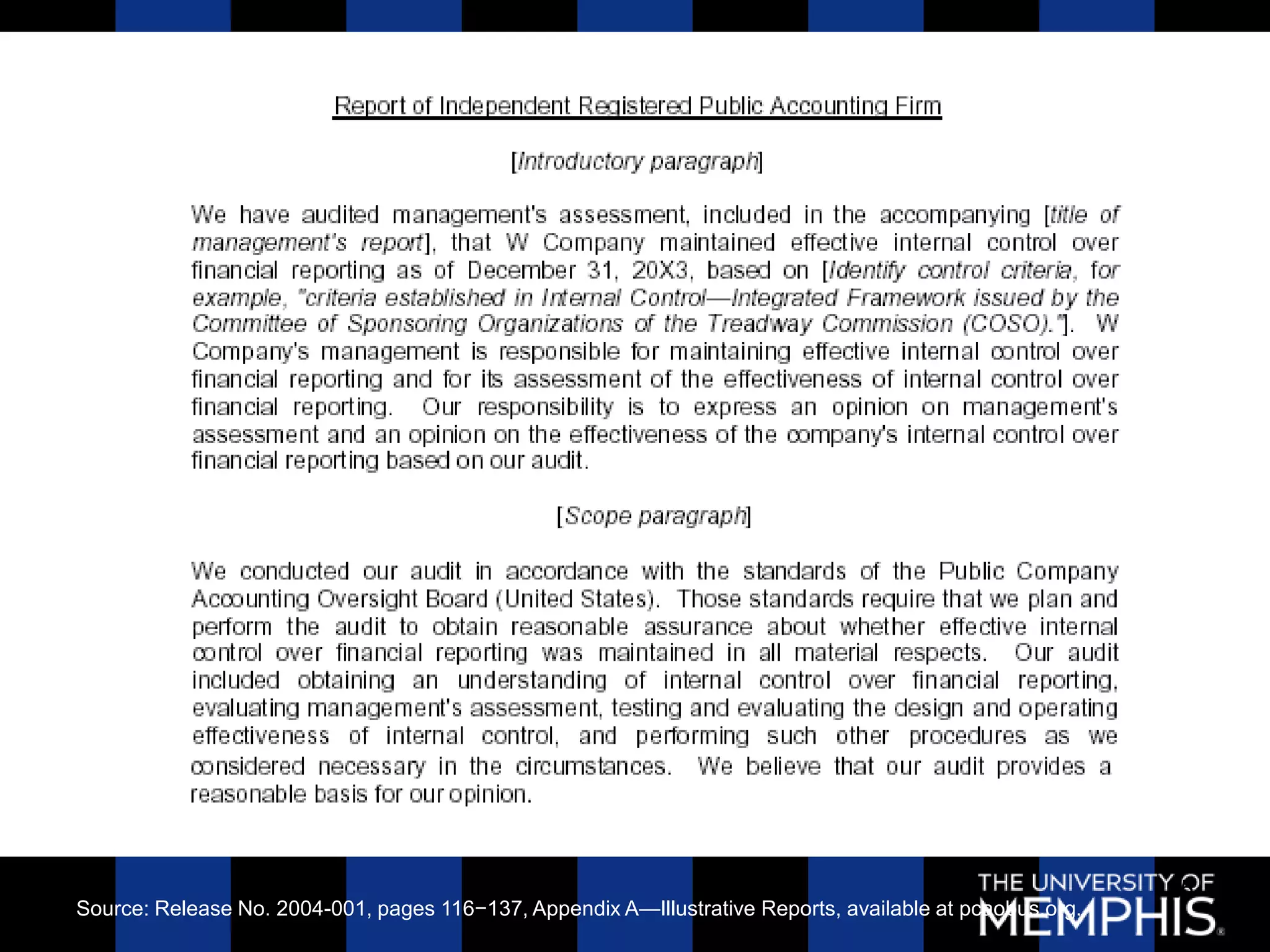

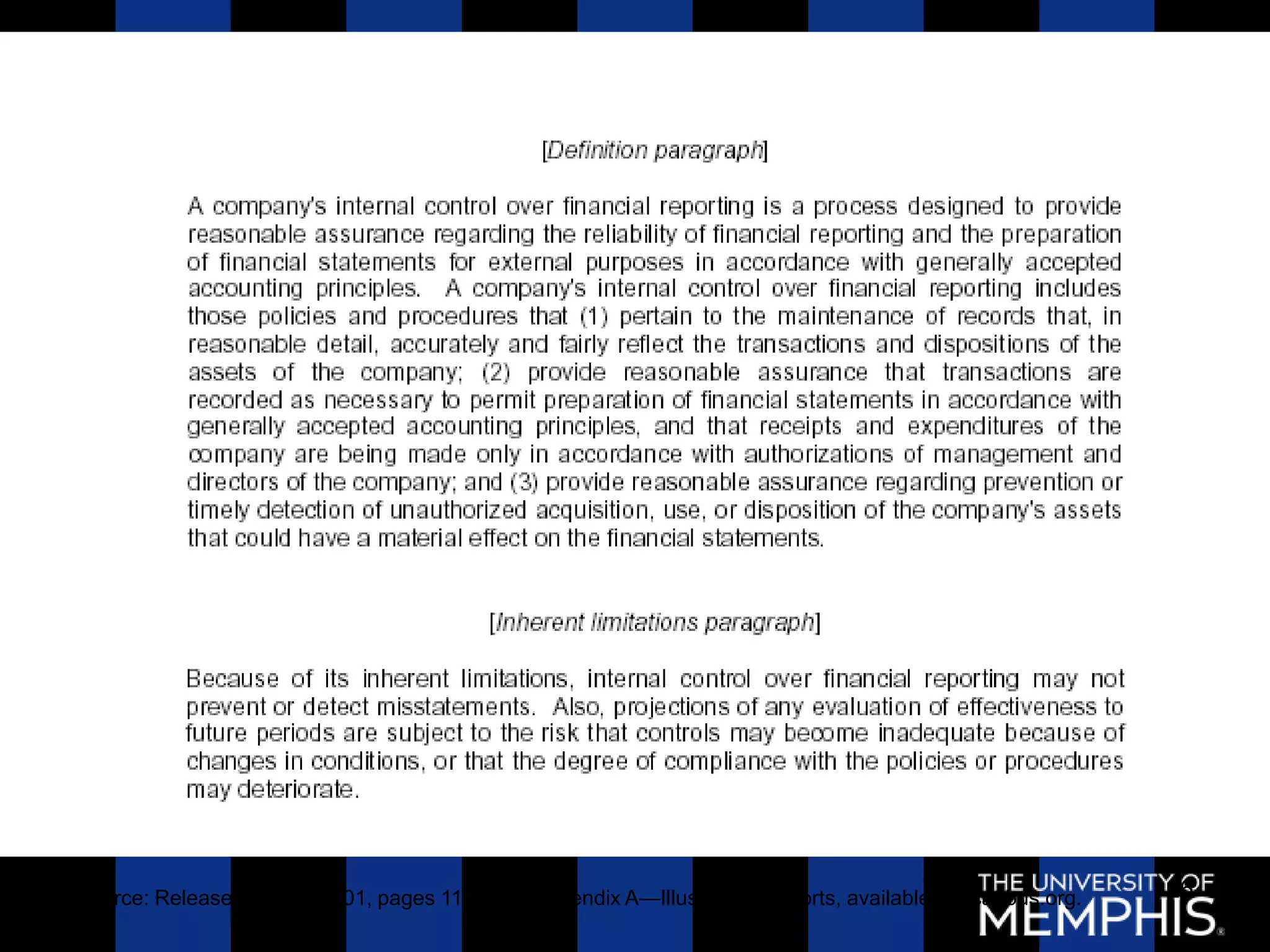

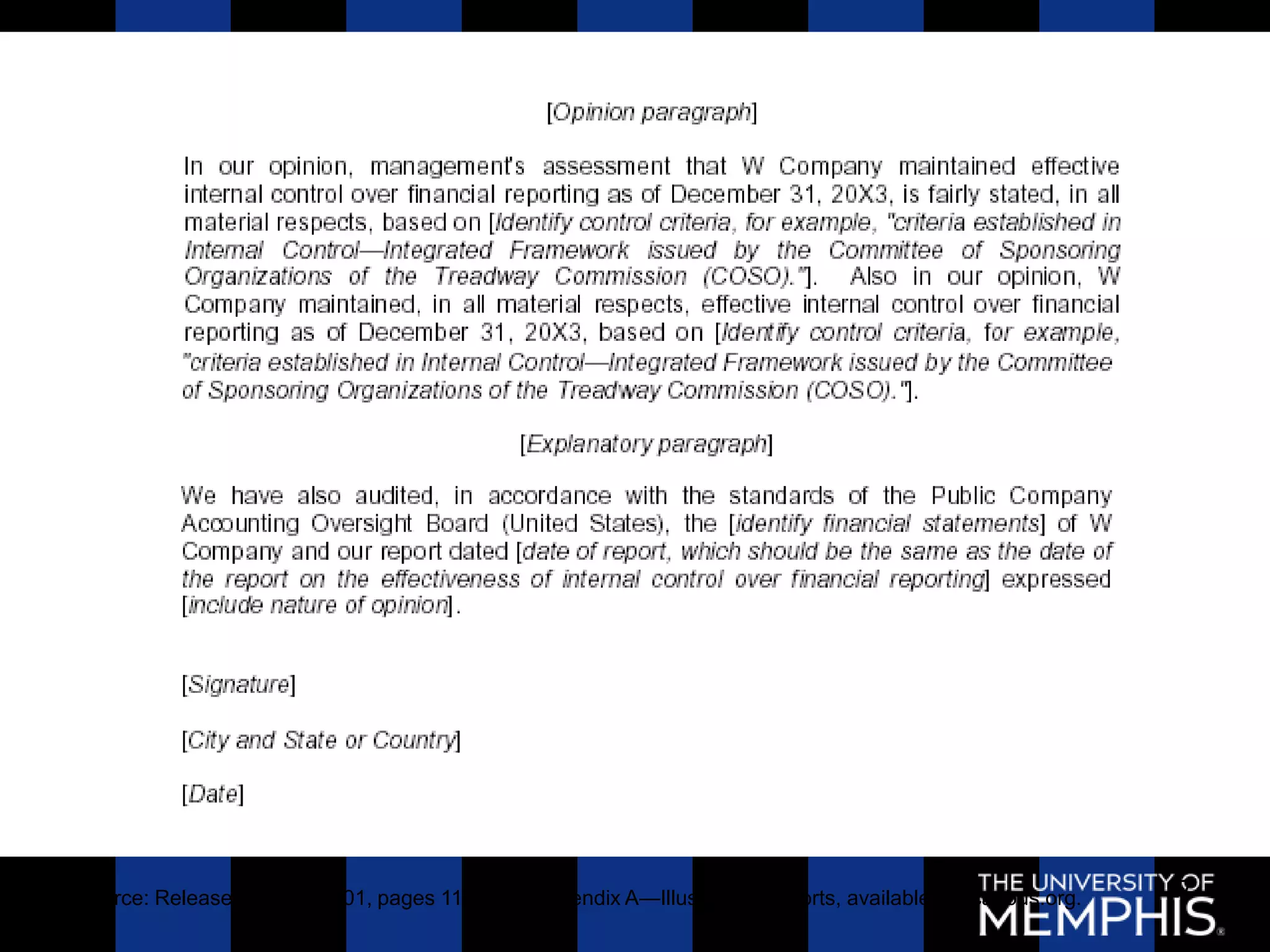

This document discusses the roles and responsibilities of external auditors. It begins by explaining that external auditors provide reasonable but not absolute assurance that financial statements are free from material misstatement. It then covers auditor competency, the different types of audit reports, and the purpose of the audit report. Finally, it discusses public company oversight by the PCAOB and key auditing standards. The document provides an overview of the expectations and regulatory requirements for external auditors.