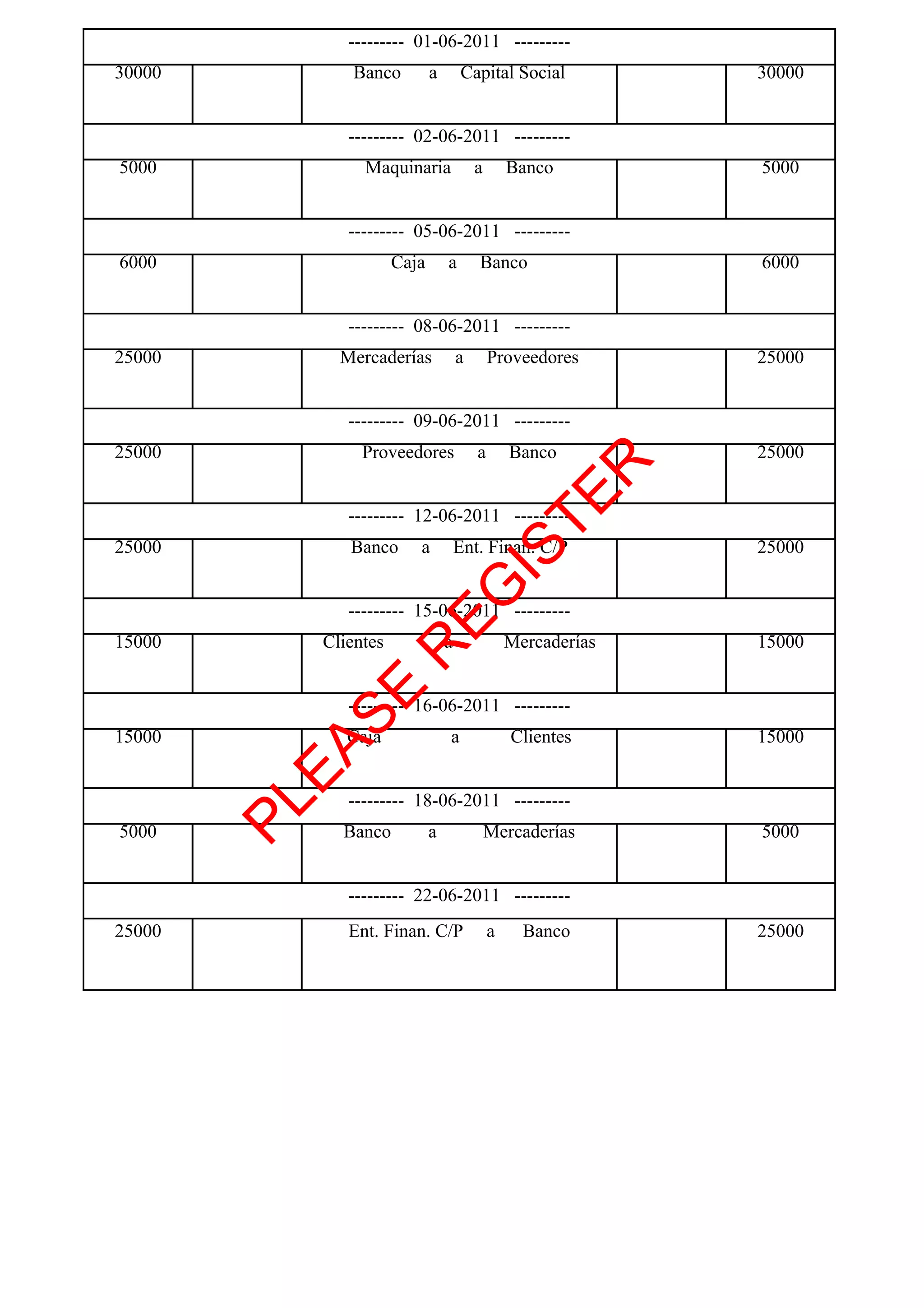

The document contains a series of accounting transactions recorded between June 1st and June 22nd. On June 1st, capital stock of $30,000 was deposited into the bank. Machinery worth $5,000 was purchased from the bank on June 2nd. $6,000 was deposited into the bank from the cashbox on June 5th. Merchandise costing $25,000 was purchased from suppliers on credit on June 8th. The suppliers were paid $25,000 on June 9th. A long-term loan of $25,000 was taken out from the bank on June 12th. Customers purchased $15,000 worth of merchandise on credit on June 15th. The customers paid $