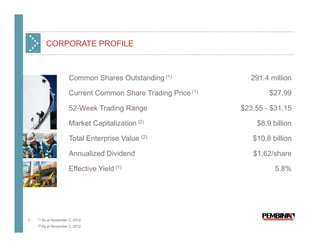

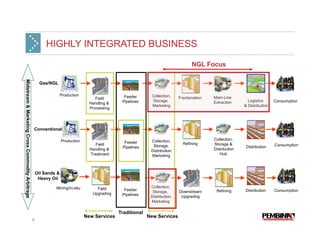

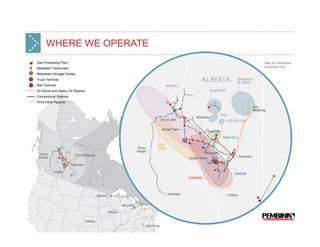

Pembina Pipeline Corporation is a midstream energy company that operates pipelines for the transportation of crude oil, natural gas liquids, and natural gas. It has a highly integrated network of pipelines and gas processing facilities located in Western Canada and North Dakota. Pembina also provides storage and marketing services for its customers. The company has a solid track record of growth through expanding its existing assets and developing new infrastructure projects to meet growing demand.

![[ls머트리얼즈]LS Materials 417200 Algorithm Investment Report](https://cdn.slidesharecdn.com/ss_thumbnails/lsmaterials417200algorithminvestmentreport-260202182715-66072c7b-thumbnail.jpg?width=640&height=640&fit=bounds)