Each week the utility sector of the Financial Markets Program presents a weekly update highlighting the performance of the XLU compared to the specific names we hold. The report provides insight into the weekly news, technical analysis & the catalysts we see going forward.

Each week the utility sector of the Financial Markets Program presents a weekly update highlighting the performance of the XLU compared to the specific names we hold. The report provides insight into the weekly news, technical analysis & the catalysts we see going forward.

While the politically charged Solyndra case made the headlines, the “real news” is the beginning of the phase-out of several federal support programs, which is going to be a game-changing factor in the field of renewable energy in the US.

This webinar addresses the key industry trends impacting transmission development, FERC Order 1000 and the impacts of the removal of the right of first refusal for transmission developers.

Nextera Energy University of Southern California Investment CTimothy O'Brien

This past spring Zane Laws, Quinn Peebles and I competed in the University of Southern California Spring 2018 Investment Competition at USC in Los Angeles. We pitched a long position in NextEra Energy Inc, ticker NEE.

:: CAPITAL RENOVABLE :: "Smart Energy Solutions"

--- 2014 Brochure -_________________________________________________

Capital Renovable is a company dedicated to the

development, construction and operation of projects for

generation and sale of electricity based on nonconventional

renewable energy (NCRE).

1. For Sale: Abortion Pills available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Contact: +971581248768.

2. Safe Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE for sale. Contact: +971581248768.

3. Contact +971581248768 for the availability of Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

4. Looking for Abortion Pills? Contact +971581248768. Available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

5. Abortion Pills on sale! Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Call +971581248768 for details.

6. Get Safe Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Contact +971581248768.

7. Contact +971581248768 to purchase Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

8. Abortion Pills available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Call +971581248768 for more information.

9. Seeking Abortion Pills? Look no further. Contact +971581248768 for availability in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

10. +971581248768 is the number to call for Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

11. Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Contact +971581248768 for purchase.

12. Safe and reliable Abortion Pills available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Call +971581248768.

13. Looking for Abortion Pills? Call +971581248768. Available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

14. Contact +971581248768 for Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

15. Abortion Pills for sale in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Dial +971581248768.

16. Get in touch with +971581248768 to purchase Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

17. Abortion Pills available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Call +971581248768 to order.

18. Need Abortion Pills? Contact +971581248768. Available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

19. Contact +971581248768 for the purchase of Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.1. Contact +971581248768 for 100% original and safe abortion pills available for sale in Dubai and Abu Dhabi!

2. Call +971581248768 to purchase in Dubai and Abu DhabiLooking for 100% original and safe abortion pills?

While the politically charged Solyndra case made the headlines, the “real news” is the beginning of the phase-out of several federal support programs, which is going to be a game-changing factor in the field of renewable energy in the US.

This webinar addresses the key industry trends impacting transmission development, FERC Order 1000 and the impacts of the removal of the right of first refusal for transmission developers.

Nextera Energy University of Southern California Investment CTimothy O'Brien

This past spring Zane Laws, Quinn Peebles and I competed in the University of Southern California Spring 2018 Investment Competition at USC in Los Angeles. We pitched a long position in NextEra Energy Inc, ticker NEE.

:: CAPITAL RENOVABLE :: "Smart Energy Solutions"

--- 2014 Brochure -_________________________________________________

Capital Renovable is a company dedicated to the

development, construction and operation of projects for

generation and sale of electricity based on nonconventional

renewable energy (NCRE).

1. For Sale: Abortion Pills available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Contact: +971581248768.

2. Safe Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE for sale. Contact: +971581248768.

3. Contact +971581248768 for the availability of Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

4. Looking for Abortion Pills? Contact +971581248768. Available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

5. Abortion Pills on sale! Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Call +971581248768 for details.

6. Get Safe Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Contact +971581248768.

7. Contact +971581248768 to purchase Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

8. Abortion Pills available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Call +971581248768 for more information.

9. Seeking Abortion Pills? Look no further. Contact +971581248768 for availability in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

10. +971581248768 is the number to call for Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

11. Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Contact +971581248768 for purchase.

12. Safe and reliable Abortion Pills available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Call +971581248768.

13. Looking for Abortion Pills? Call +971581248768. Available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

14. Contact +971581248768 for Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

15. Abortion Pills for sale in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Dial +971581248768.

16. Get in touch with +971581248768 to purchase Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

17. Abortion Pills available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Call +971581248768 to order.

18. Need Abortion Pills? Contact +971581248768. Available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

19. Contact +971581248768 for the purchase of Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.1. Contact +971581248768 for 100% original and safe abortion pills available for sale in Dubai and Abu Dhabi!

2. Call +971581248768 to purchase in Dubai and Abu DhabiLooking for 100% original and safe abortion pills?

1. For Sale: Abortion Pills available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Contact: +971581248768.

2. Safe Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE for sale. Contact: +971581248768.

3. Contact +971581248768 for the availability of Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

4. Looking for Abortion Pills? Contact +971581248768. Available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

5. Abortion Pills on sale! Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Call +971581248768 for details.

6. Get Safe Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Contact +971581248768.

7. Contact +971581248768 to purchase Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

8. Abortion Pills available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Call +971581248768 for more information.

9. Seeking Abortion Pills? Look no further. Contact +971581248768 for availability in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

10. +971581248768 is the number to call for Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

11. Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Contact +971581248768 for purchase.

12. Safe and reliable Abortion Pills available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Call +971581248768.

13. Looking for Abortion Pills? Call +971581248768. Available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

14. Contact +971581248768 for Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

15. Abortion Pills for sale in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Dial +971581248768.

16. Get in touch with +971581248768 to purchase Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

17. Abortion Pills available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Call +971581248768 to order.

18. Need Abortion Pills? Contact +971581248768. Available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

19. Contact +971581248768 for the purchase of Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.1. Contact +971581248768 for 100% original and safe abortion pills available for sale in Dubai and Abu Dhabi!

2. Call +971581248768 to purchase in Dubai and Abu DhabiLooking for 100% original and safe abortion pills?

1. For Sale: Abortion Pills available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Contact: +971581248768.

2. Safe Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE for sale. Contact: +971581248768.

3. Contact +971581248768 for the availability of Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

4. Looking for Abortion Pills? Contact +971581248768. Available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

5. Abortion Pills on sale! Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Call +971581248768 for details.

6. Get Safe Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Contact +971581248768.

7. Contact +971581248768 to purchase Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

8. Abortion Pills available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Call +971581248768 for more information.

9. Seeking Abortion Pills? Look no further. Contact +971581248768 for availability in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

10. +971581248768 is the number to call for Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

11. Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Contact +971581248768 for purchase.

12. Safe and reliable Abortion Pills available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Call +971581248768.

13. Looking for Abortion Pills? Call +971581248768. Available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

14. Contact +971581248768 for Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

15. Abortion Pills for sale in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Dial +971581248768.

16. Get in touch with +971581248768 to purchase Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

17. Abortion Pills available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Call +971581248768 to order.

18. Need Abortion Pills? Contact +971581248768. Available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

19. Contact +971581248768 for the purchase of Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.1. Contact +971581248768 for 100% original and safe abortion pills available for sale in Dubai and Abu Dhabi!

2. Call +971581248768 to purchase in Dubai and Abu DhabiLooking for 100% original and safe abortion pills?

1. For Sale: Abortion Pills available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Contact: +971581248768.

2. Safe Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE for sale. Contact: +971581248768.

3. Contact +971581248768 for the availability of Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

4. Looking for Abortion Pills? Contact +971581248768. Available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

5. Abortion Pills on sale! Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Call +971581248768 for details.

6. Get Safe Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Contact +971581248768.

7. Contact +971581248768 to purchase Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

8. Abortion Pills available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Call +971581248768 for more information.

9. Seeking Abortion Pills? Look no further. Contact +971581248768 for availability in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

10. +971581248768 is the number to call for Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

11. Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Contact +971581248768 for purchase.

12. Safe and reliable Abortion Pills available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Call +971581248768.

13. Looking for Abortion Pills? Call +971581248768. Available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

14. Contact +971581248768 for Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

15. Abortion Pills for sale in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Dial +971581248768.

16. Get in touch with +971581248768 to purchase Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

17. Abortion Pills available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Call +971581248768 to order.

18. Need Abortion Pills? Contact +971581248768. Available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

19. Contact +971581248768 for the purchase of Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.1. Contact +971581248768 for 100% original and safe abortion pills available for sale in Dubai and Abu Dhabi!

2. Call +971581248768 to purchase in Dubai and Abu DhabiLooking for 100% original and safe abortion pills?

1. For Sale: Abortion Pills available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Contact: +971581248768.

2. Safe Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE for sale. Contact: +971581248768.

3. Contact +971581248768 for the availability of Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

4. Looking for Abortion Pills? Contact +971581248768. Available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

5. Abortion Pills on sale! Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Call +971581248768 for details.

6. Get Safe Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Contact +971581248768.

7. Contact +971581248768 to purchase Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

8. Abortion Pills available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Call +971581248768 for more information.

9. Seeking Abortion Pills? Look no further. Contact +971581248768 for availability in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

10. +971581248768 is the number to call for Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

11. Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Contact +971581248768 for purchase.

12. Safe and reliable Abortion Pills available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Call +971581248768.

13. Looking for Abortion Pills? Call +971581248768. Available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

14. Contact +971581248768 for Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

15. Abortion Pills for sale in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Dial +971581248768.

16. Get in touch with +971581248768 to purchase Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

17. Abortion Pills available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Call +971581248768 to order.

18. Need Abortion Pills? Contact +971581248768. Available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

19. Contact +971581248768 for the purchase of Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.1. Contact +971581248768 for 100% original and safe abortion pills available for sale in Dubai and Abu Dhabi!

2. Call +971581248768 to purchase in Dubai and Abu DhabiLooking for 100% original and safe abortion pills?

1. For Sale: Abortion Pills available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Contact: +971581248768.

2. Safe Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE for sale. Contact: +971581248768.

3. Contact +971581248768 for the availability of Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

4. Looking for Abortion Pills? Contact +971581248768. Available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

5. Abortion Pills on sale! Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Call +971581248768 for details.

6. Get Safe Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Contact +971581248768.

7. Contact +971581248768 to purchase Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

8. Abortion Pills available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Call +971581248768 for more information.

9. Seeking Abortion Pills? Look no further. Contact +971581248768 for availability in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

10. +971581248768 is the number to call for Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

11. Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Contact +971581248768 for purchase.

12. Safe and reliable Abortion Pills available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Call +971581248768.

13. Looking for Abortion Pills? Call +971581248768. Available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

14. Contact +971581248768 for Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

15. Abortion Pills for sale in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Dial +971581248768.

16. Get in touch with +971581248768 to purchase Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

17. Abortion Pills available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE. Call +971581248768 to order.

18. Need Abortion Pills? Contact +971581248768. Available in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.

19. Contact +971581248768 for the purchase of Abortion Pills in Dubai, Abu Dhabi, Sharjah, Ajman, Fujairah, Al Ras Khaimah (RAK) City, Al Ain-UAE.1. Contact +971581248768 for 100% original and safe abortion pills available for sale in Dubai and Abu Dhabi!

2. Call +971581248768 to purchase in Dubai and Abu DhabiLooking for 100% original and safe abortion pills?

1000-1250 words

Table of Contents

Abstract 2

Introduction 3

Organizational analysis 3

Leadership 3

Market 3

Operations 3

Finance 4

Performance 4

Regulatory environment 4

Critical incidents 4

Investment potential 4

Recommendation 4

References 5

Abstract

The goal of this case study is to provide a detailed outline for potential addition into the company’s investment portfolio. The company targeted for potential investment is Pacific Gas and Electric Company or PG&E. Covered herein is the organizational analysis, critical incidents, the company’s investment potential, and recommendations based on findings.

Introduction

PG&E Corporation (PG&E or the company) is an energy-based holding company for Pacific Gas and Electric Company (Pacific Gas and Electric). PG&E subsidiaries provide customers with public utility services, and services relating to the generation of energy, transmission of electricity and natural gas, generation of electricity, and the distribution of energy. The company primarily operates in the US. It is headquartered in San Francisco, California, and employed 21,166 people as on December 31, 2013.Organizational analysisLeadership

PG&E is an energy-based holding company for Pacific Gas and Electric. Pacific Gas and Electric is engaged primarily in the following businesses: electricity and natural gas distribution; electricity generation, procurement, and transmission; and natural gas procurement, transportation, and storage. PG&E operates through two segments: electric and natural gas. The company's strength lies in its strong distribution network in electricity and natural gas segments, which provide it with a competitive edge. However, volatility of the natural gas and electricity markets may adversely impact its financial condition, results of operations, and cash flows.Market

PG&E's subsidiary, Pacific Gas and Electric, has a strong distribution network for the supply of electricity and natural gas. As on December 31, 2013, the company owned approximately 18,115 circuit miles of interconnected transmission lines operated at voltages of 500 kV to 60 kV and transmission substations with a capacity of 62,289 MVA. Pacific Gas and Electric's electricity distribution network consists of approximately 141,000 circuit miles of distribution lines (of which approximately 20% are underground and approximately 80% are overhead), 58 transmission-switching substations, and 603 distribution substations. The strong distribution network provides competitive advantage to the company.Operations

As on December 31, 2013, Pacific Gas and Electric's natural gas system consisted of approximately 42,559 miles of distribution pipelines, over 6,000 miles of backbone and local transmission pipelines, and various storage facilities. Pacific Gas and Electric owns and operates three underground natural gas storage fields connected to its transmission and storage system and has a 25% interest in the new Gill Ranch Storage Field. In addition, three indep.

How cleantech can close the financing gaptonymaull92

The most fundamental element of disruptive business models is financing. the article explores creating, adopting and adapting proven models for new industries.

The global renewable energy market has grown rapidly over the past few years. Driven by improving sector dynamics, renewable energy witnessing emergence of newer investment options in the capital markets segment.

Equity Market Reactions based on Company’s Financial StrategiesRUPANJAN NAYAK

Equity Market Reactions based on Company’s Financial Strategies on a POWER UTILITY COMPANY: CESC PVT LTD.

1. Contains equity stock market reactions based on company financial restructuring strategies like: following a lean business model, layoff and retrenchments, going full digital from offline business model etc.

2. The impact on the shareholders due to diversification.

3. Impact on the shareholders due to company strategic restructuring.

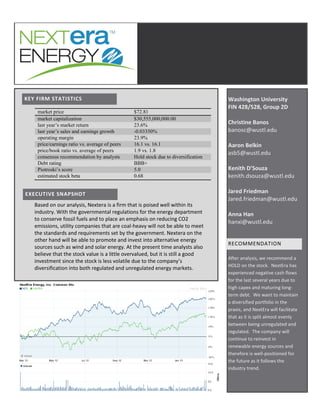

1. market price $72.81

market capitalization $30,555,000,000.00

last year’s market return 23.6%

last year’s sales and earnings growth -0.03350%

operating margin 23.9%

price/earnings ratio vs. average of peers 16.1 vs. 16.1

price/book ratio vs. average of peers 1.9 vs. 1.8

consensus recommendation by analysts Hold stock due to diversification

Debt rating BBB+

Piotroski’s score 5.0

estimated stock beta 0.68

Washington University

FIN 428/528, Group 2D

Christine Banos

banosc@wustl.edu

Aaron Belkin

asb5@wustl.edu

Kenith D’Souza

kenith.dsouza@wustl.edu

Jared Friedman

Jared.friedman@wustl.edu

Anna Han

hanxi@wustl.edu

RECOMMENDATION

After analysis, we recommend a

HOLD on the stock. NextEra has

experienced negative cash flows

for the last several years due to

high capex and maturing long-

term debt. We want to maintain

a diversified portfolio in the

praxis, and NextEra will facilitate

that as it is split almost evenly

between being unregulated and

regulated. The company will

continue to reinvest in

renewable energy sources and

therefore is well-positioned for

the future as it follows the

industry trend.

KEY FIRM STATISTICS

Based on our analysis, Nextera is a firm that is poised well within its

industry. With the governmental regulations for the energy department

to conserve fossil fuels and to place an emphasis on reducing CO2

emissions, utility companies that are coal-heavy will not be able to meet

the standards and requirements set by the government. Nextera on the

other hand will be able to promote and invest into alternative energy

sources such as wind and solar energy. At the present time analysts also

believe that the stock value is a little overvalued, but it is still a good

investment since the stock is less volatile due to the company’s

diversification into both regulated and unregulated energy markets.

EXECUTIVE SNAPSHOT

2. OVERVIEW OF NEXTERA ENERGY, INC.

For a brief introduction into what NextEra Energy, Inc. is, the New York Times explains that the company

“provides retail and wholesale electric services to approximately four million customers and owns

generation, transmission and distribution facilities to support its services. It also purchases electric

power for resale to its customers and provides risk management services related to power and gas

consumption for a limited number of customers.”1

As stated on their company website, “NextEra

Energy, Inc. is a leading clean-energy company with revenues of more than $15.3 billion, more than

41,000 megawatts (MW) of generating capacity, and approximately 15,000 employees in 24 states and

Canada as of year-end 2011.”2

It has garnered several awards over the years, including Forbes 2011-

2012 No.1 overall gas and utilities company, for its countless efforts towards environmental

sustainability and renewable energy procedures.

SUBSIDIARIES

NextEra is currently composed of three subsidiaries:

Florida Power & Light: As U.S.’s third largest utility company and NextEra’s largest subsidiary,

FPL distributes power at regulated rates over four million customers in Florida.

NextEra Energy Resources: NER composes the company’s clean energy portion and serves as

the country’s leader in the production of energy through wind and solar processes.

FPL FiberNet: Started by FPL in the 1980’s, FPL FiberNet provides fiber-optic solutions to

customers in both Florida and Texas.

MAIN PRODUCTS/SERVICES

NextEra provides several products and services for its customers. These include:

Wind energy: One of the world’s largest generators, with facilities throughout the United

States and Canada.

Solar energy: Largest generator using both photovoltaic and solar thermal technologies.

Hydroelectric energy: All 22 facilities located in Maine

Fossil fueled facilities

Nuclear energy: Three nuclear-powered plants in Iowa, Wisconsin, and New Hampshire.

Energy marketing: Leading electricity and natural gas marketers in the country while

additionally responsible for electricity and fuel management of the company’s generation.

Specialized wind: Under its WindLogics program, NextEra “researches historical wind resource

data and wind patterns” by providing “engineering, technical analysis and consulting services in

the field of studying, modeling, and forecasting meteorological air flow.”3

1

http://topics.nytimes.com/top/news/business/companies/fpl_group_inc/index.html

2

http://www.investor.nexteraenergy.com/phoenix.zhtml?c=88486&p=irol-homeProfile

3

http://www.nexteraenergyresources.com/what/specialized_wind.shtml

3. Retail market: Under Gexa Energy, this service provides electricity to both residential and

commercial customers.

Exhibit 1 provides a more detailed breakdown of the products provided.

COMPETITORS

NextEra’s competition includes Progress Energy, Inc. (privately held), Southern Company, and TECO

Energy, Inc with their respective market capitalizations listed below.

4

RECENT DEVELOPMENTS AND NEWS STORIES

FLORIDA POWER AND LIGHT COMPANY

FPL, a subsidiary of NextEra, announced on January 29th

that they have launched a new website,

PoweringFlorida.com, which serves as a resource to help businesses in Florida to start, relocate, or

expand their companies. As CEO of Boyette Strategic Advisors, Del Boyette explains,

“PoweringFlorida.com has achieved a first: bringing the best planning and workforce data together

in one click. What that means for companies and their site selectors is unfiltered and unparalleled

insight – county by county and block by block. What that means for Florida is a competitive

advantage for the right types of jobs and investment.”5

SELLING RESOURCES

On December 21, 2012, NextEra Resources, a subsidiary of NextEra, took part in an agreement to sell its

hydro generating assets to Brookfield Energy Partners, L.P. As Armando Pimentel, the CEO of NextEra

Energy Resources, explains, “While this is an attractive portfolio in many respects, this transaction

enables us to further optimize our power generation portfolio and concentrate our resources on areas

with greater growth potential for our business."6

The transaction is still in its pending stages and is

4

http://finance.yahoo.com/q/co?s=NEE+Competitors

5

http://www.nexteraenergy.com/news/contents/2013/012913_1.shtml

6

http://markets.on.nytimes.com/research/stocks/news/press_release.asp?docTag=201212211920PR_NEWS_USPR

X____FL34195&feedID=600&press_symbol=109578

Competition Market Capitalization

NextEra Energy, Inc. 30.77B

Progress Energy, Inc. N/A

Southern Company 39.11B

TECO Energy, Inc. 3.67B

Industry 6.97B

4. expected to be completed by the end of the first quarter of the 2013 fiscal year. While there is an

anticipated result of a gain upon completion, it is not expected to have a significant impact on the

current or future financial position of NextEra.

WHERE NEXTERA IS HEADED7

NextEra’s future within the utilities industry looks strong and profitable. Both of their main subsidiaries,

FPL and NER, have proven successful over the last decade as they have continued to bring in profits and

spark growth. Overall, the company’s shareholder return maintains an edge over the electric utility

industry and has exceeded expectations. For example, at year-end 2011 NextEra informed the public

that its total shareholder return over the past decade was 209%, a percentage nearly double that of the

S&P 500 Electric Utilities Index.

NextEra will continue to expend the $15 billion of capital it anticipated to use between 2010-2014. This

includes more than $6 billion of major generation and advanced metering projects as well as an

investment of an additional $6 billion in new wind and solar projects. This will not only continue but

expand NextEra’s position as the renewable energy leader.

Additionally, NextEra expects that its adjusted earnings per share for 2013 and 2014 will be from $4.70-

$5.00 and $5.05-$5.65, respectively and its growth to be 5%-7% in the long-run. We were bullish on the

renewable sector of the industry and therefore this increase in stock, however slight, between 2013 and

2014 makes sense as the industry sees an expansion and dominant presence of renewable energy

sources in the utilities industry.

With the recent climatic changes and disasters, new utility infrastructure is being researched and

developed, a trend seen for much of the entire industry. As a result, NextEra will invest nearly $7.5

billion in this area and in turn garner higher returns and drive earnings growth until at least 2015.

In regards to the company’s renewable energy program, NextEra continues to increase its capacity

generation in natural gas-fired plants and wind energy. Specifically concerning its wind energy, NextEra

already experiences great advantages over other companies, including access to wind turbines and

operational excellence. As a result, the company increases its appeal to other utilities looking to have a

greater mix of wind energy in their portfolio.

Overall, with the industry’s and government’s increased focus on environmental regulations, NextEra

appears well-positioned. The company will continue to see growth as Florida’s economy advances.

ANALYST OPINIONS8

Nextera is a company that is deals in both regulated and unregulated energy. Analysts believe that

Nextera is a safe and steady option with annual earnings growth rate of 6.5% and dividend growth rate

of 10%. In terms of regulated energy since the recession there has been a stagnation of growth, but

after the ruling on the rates for energy prices this growth should resume. Also due to its prime

7

http://www.investor.nexteraenergy.com/phoenix.zhtml?c=88486&p=earningsRelease12

8

NEE Morningstar Report

5. geographic location in Florida, Nextera is poised to plunge ahead into multiple alternative energy

markets such as wind energy and solar energy. This is beneficial to the company since it is so diversified.

If the regulated market takes a hit and the prices for energy go down then the company can invest more

in the unregulated market. Also with increased governmental regulation on preserving the environment

and fossil fuel regulation, Nextera’s decision to move ahead into alternative energy is a great idea.

Nextera’s current stock value is a little over-valued, but all in all it seems like a good stock to invest in

terms of steady growth and dividend yield.

SWOT ANALYSIS9

Strengths:

o Established operations in Florida

o Diverse customer base

o Balanced fuel mix

Weaknesses:

o Limited presence

o Substantial debt

o Dependence on subsidiaries

Opportunities:

o Focus on renewable energy

o Rising demand for electricity

Threats:

o Risks associated with nuclear operations

o Weather conditions

o Compliance to environmental regulations

FINANCIAL STATEMENT ANALYSIS

Nextera’s 2012 10-K had not yet been released at the time of our analysis, we will focused our

evaluation on the company’s third quarter 10-Q SEC filing, as well as the unaudited earnings releases for

the fourth quarter of 2012 and the entire year of 2012.

After reviewing Nextera’s 2011 annual report and its quarterly report for the third quarter, we turned to

the most recent earnings release to examine trends in performance and growth. The amount of energy

being sold has noticeably decreased over the past four years, although the drop was not as significant

between 2011 and 2012. This past year, the majority of the decrease occurred in the Residential

segment, which is still the largest customer segment. Total energy sales (in Kilowatt-hours) have

decreased from 105,414 million kwh in 2009 to 81,002 million kwh in 2012. Similarly, the average price

of power is slowly decreasing, from 11.19 cents/kwh to 9.53 center/kwh four years later. Despite these

disappointing trends, we do see that the number of customer accounts is increasing, in both the

commercial and the residential sectors.

9

Market Line

6. To see how these trends fit into the big picture, we evaluated Nextera’s changes in net income over the

past 10 years. Graphing the net income from 2002 to 2012, we noticed a clear cyclical pattern; however,

the profitably was noticeably decreasing over time. Superimposing a linear line over the percentage

changes in net income, we roughly estimate a 4.94% annual decrease in net income (smoothing out the

cyclical patterns). These trends seem to fall in line with our industry analysis: energy consumption per

capita is decreasing, but an overall increase in population is making up for the lost demand marginally.

Change in net income by itself is far from conclusive. We also examined the consolidated balance sheets

from the past five years for trends in a number of items. First, the amount of cash and cash equivalents

has been volatile over the years, with seemingly no clear direction of whether it is increasing or

decreasing. With a high of $535 million in 2008 to a low of $238 million the next year, 2012 was in

between at $329 million. Next, net debt is calculated as the sum of short term and long term debt,

subtracted by the working capital. Over the past four years we see a trend of increasing net debt; from

$18.6 million in 2009 gradually rising to $27.0 million in 2012. This increase is also reflected in the

leverage ratio, which has climbed from 1.4 in 2009 to 1.7 today. In addition, working capital continues

to be below zero and has become more negative in 2012 than in the past five years at -$3,492,000.

This increase in debt could be related to a corresponding increase we see in the amount of fixed asset.

Electric utility plant in service and other property assets have increased by over two million dollars or

more each year. In addition, Nextera remains without any minority interest invested in the company.

To better understand what these financial statement numbers mean going into the future, we

calculated several profitability ratios. First, the gross margin ratio we found to be noticeably increasing

over the past four years, from 0.373 in 2009 to 0.544 in 2012. Similarly, the operating margin ratio has

also increased from 0.166 to 0.230 over the same four years. On the other hand, return on equity and

return on asset both appear to be slowly decreasing; ROE from 0.125 in 2009 down to 0.119 in 2012,

while ROA decreased from 0.0333 in 2009 to 0.0297 in 2012.

DCF VALUATION

In establishing projections for NextEra’s expected free cash flows for the next 5 years we first examined

historical data to uncover operating trends and margins. More specifically, we looked at the 5-year

historical revenue growth rate and how operating costs, depreciation, capital expenditures and net

working capital changed as a percentage of revenue over the same 5-year period. Our analysis showed

that over this 5-year historical period, operating costs trended downward, averaging approximately

71.37% of revenue, depreciation and amortization 10.17%, capital expenditures 34.37%, and net

working capital 7.06%.

Going forward, we projected that almost all of these historical margins will continue at approximately

the same percentages; however, we believe that operating costs and capital expenditures will change

slightly. We believe that operating costs as a percentage of revenue will trend downwards slightly as

higher utility rates are approved by Florida’s regulatory agencies to sustain approved ROE levels,

increasing revenues while maintaining level operating expenses. Additionally, while we believe capital

7. expenditures will drop to their long-term historical average, which is approximately 20%, in the short-

term we expect NextEra to take advantage of the low interest rate environment and maintain capital

expenditures on new solar and wind investments at levels commensurate with their 5-year historical

average of 34.37%.

With respect to revenue growth, we assumed an immediate annual growth of 6% driven primarily by

new wind and solar investment. Subsequently, we believe that revenue growth will trend downwards

and ultimately level off at a terminal growth rate comparable to that of GDP, or 2% (Exhibit 11).

12. EXHIBIT 7

From NextEra 2012 4

th

quarter earnings summary and non-GAAP reconciliations

EXHIBIT 8

-4

-2

0

2

4

6

8

EBITDA and Working Capital of NEE and 18 Utilities in $Billion sorted by

decreasing Market Capitalization

EBITDA $B Working Cap $B

13. EXHIBIT 9

Price-to-Earnings Ratio for NEE and 18 other Utilities Companies

0 5 10 15 20 25 30 35 40 45 50

DUK

SO

NEE

Exelon

PCG

PPL

XEL

NU

ETR

CNP

CPN

AEE

NI

AWK

CMS

PNW

POM

NVE

TE