1. KESTREL CAPITAL

Member of the Nairobi Stock Exchange

December 2010

MUMIAS SUGAR COMPANY LTD

Move Ye Coast and Diversify

We recommend an ACCUMULATE on Mumias Sugar Company (‘Mumias’) based on the

expected future potential upside from the diversification initiatives which include the Tana

& Athi River Development Authority (‘Tarda’) integrated Greenfield project at the coast,

diversification into power co-generation, ethanol production and impending sector reforms.

The miller, and the sector in general, are facing a challenging operating environment ahead

of the expiry of the Common Market for East and Southern Africa (‘Comesa’) safeguard

window in 2012. Under Comesa rules, this period cannot be extended further.

• Mumias is the leading sugar producer in the country with a 45.2% market share (and

plans to increase via acquisition) as at end of 2009 and has a countrywide distribution

network. Brand equity has adequately been exploited as reflected in the premium pric-

ing of its pre-packaged and branded sugar which accounts for 40% of production.

• The sector is faced with serious challenges including over dependence on rain-fed cane,

small and fragmented farm holdings which account for about 94% of area under cane,

declining cane yields (at 6.7 ton per hectare, T/Ha, against the recommended 10.0T/Ha),

higher input and production costs (estimated at USD 500 per ton) which are almost dou-

ble those from other producers in the Comesa region, cane poaching, poor road infra-

structure in some areas and ageing plant machinery. In FY09 operating margins de-

clined by 470bps to 9.2% as a result of a 750bps increase in cost per ton to 36.5%, the

highest in the past 8 years.

• In our view, the Comesa expiry period may not pose a serious threat to Mumias in the

medium term. This is because the Comesa region with 23 countries is in itself as deficit

region as most countries are net importers of sugar from non-Comesa countries. For

Kenya, despite the duty free quota having been set to increase by 40,000 tons annually

from 2008, only 184,531 tons (out of the required quota of 220,000 tons) were imported

in 2009. Most of the imported sugar came from non-Comesa countries like South Af-

rica, Thailand and Saudi Arabia. Also, most of the producers in the Comesa region opt

to export to the more lucrative European markets where they are able to fetch higher

prices. The situation is exacerbated by recent low production amongst world’s top pro-

ducers like India due to drought and Brazil’s export bottlenecks together with the coun-

try’s policy of balancing of ethanol and sugar.

Key Statistics FY2007 FY2008 FY2009 FY2010A FY2011F FY2012F

EPS (KES) 2.73 0.79 1.05 1.03 1.22 1.51

% ch -8.7 -71.0 32.6 -2.3 18.8 23.3

DPS (KES) 1.50 0.40 0.40 0.40 0.40 0.40

% ch -14.3 -73.3 0.0 0.0 0.0 0.0

P/E x 5.4 8.5 6.5 9.3 7.8 6.3

P/B x 0.9 1.1 1.0 1.3 1.1 1.0

Div yield % 10.1 5.9 5.8 4.2 4.2 4.2

Source: Company, Kestrel estimates

Bloomberg Ticker : MSUG KN

Reuters Ticker: MSCL NR

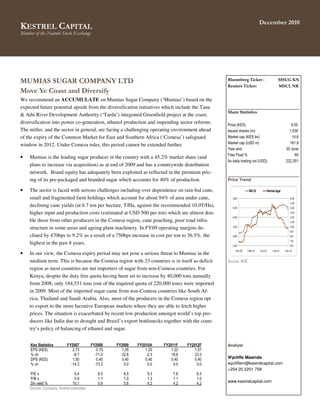

Share Statistics

Price (KES) 9.55

Issued shares (m) 1,530

Market cap (KES bn) 14.6

Market cap (USD m) 181.8

Year end 30 June

Free Float % 80

Av daily trading vol (USD) 222,351

Price Trend

Source: NSE

Analyst

Wycliffe Masinde

wycliffem@kestrelcapital.com

+254 20 2251 758

www.kestrelcapital.com

6.00

7.00

8.00

9.00

10.00

11.00

12.00

13.00

14.00

15.00

16.00

2,500

3,000

3,500

4,000

4,500

5,000

2-Dec-09 3-Mar-10 2-Jun-10 1-Sep-10 1-Dec-10

NSE20 MumiasSugar

2. Mumias Sugar Research Update KESTREL CAPITAL

FY10 Results summary

Mumias Sugar Company Ltd.

Income Statement FY09 FY10 % ch

Gross sales 14,197 18,798 32.4

VAT (1,932) (2,575) 33.2

Sugar Development Levy (462) (605) 31.1

Net sales 11,803 15,618 32.3

Operating profit 1,084 2,145 97.8

Net finance cost 109 35 -67.5

Profit before tax 1,193 2,180 82.7

Taxation (charge)/credit 417 (607) -

Profit after tax 1,610 1,572 -2.3

EPS (KES) 1.05 1.03 -1.9

DPS (KES) 0.40 0.40 -

Source: Company

Mumias released FY10 results showing a 2.3% y-o-y reduction in profit after tax to KES 1.6bn.

The dip in earnings was attributed to a KES 607m taxation charge in FY10. In FY09, the com-

pany benefited from a 150% tax remission on its 38MW cogeneration plant. The plant, commis-

sioned in May 2009 and which commenced full operations in January 2010, contributed KES

359m to gross revenues though it hasn’t started operating at full capacity due to less fuel from

the raw material, bagasse, and reduced uptake by their main customer, Kenya Power.

• Gross sales went up 32.4% y-o-y to KES 18.8bn and net revenue was up 32.3% y-o-y to

KES 15.6bn as a result of an increase in sugar prices and a 2.0% increase in sugar produced

to 235,792 tons. Sugar cane processed went up 7.3% to 2,318,080 tones due to higher fac-

tory availability and efficiency as a result of major repairs and maintenance at the beginning

of FY10 (July 2009). Mumias’ Factory Time Efficiency (FTE) was the highest in the sector

at 90.7% (though still lower than a target FTE of 92%).

• Sugar prices in the Comesa region have been going up occasioned by the deficit in the

world market making it attractive for most countries with surplus in the region (Comesa) to

export their sugar to the European market where they are able to fetch higher prices.

• Plans by the miller to enter into a Greenfield operation at the coast of Kenya at a cost of

KES 32bn are still on course. The main advantage for this project will be the fast maturity of

cane (about 14 months as compared to 20 months in the western region) and economies of

scale that will come with large nucleus farms as opposed to the current small holdings. In a

bid to increase its competitiveness ahead of the expiry of the Comesa safeguard period by

March 2012, Mumias sugar plans to invest in an ethanol plant at its current site capable of

producing up to 24ml of ethanol. The government has already gazetted laws requiring all

petroleum companies in the western region to start blending their petrol with industrial etha-

nol.

3. Mumias Sugar Research Update KESTREL CAPITAL

Industry Overview

Tough Operating Environment

There are currently 9 licensed sugar millers in the country. These include Mumias Sugar, Mi-

wani, Nzoia Sugar, Muhoroni, West Kenya Sugar, Kibos, Soin, South Nyanza (Sony) and Che-

melil. The government owns a 20% stake in Mumias and fully owns another 5 millers (two of

which are under receivership). Mumias Sugar is the leading sugar producer in the country with a

45.2% market share as shown in the chart below.

Source: Kenya Sugar Board

The government plans to privatize the 5 state-owned sugar millers before March 2012 when the

Comesa safeguard period ends. It is estimated that the 5 sugar factories to be privatized have

accumulated debts estimated at KES 42bn owed to the government and out-grower farmers

which have to be cleared from the balance sheet before they are sold off. According to prelimi-

nary plans by the government, some of the debts might be written off and the rest paid off by the

strategic investor. The cabinet has already approved a draft plan by the Privatization Commission

for sale of a 51% stake to a strategic investor who will help turn around the factories into profit-

ability including replacement of the old plant equipments. Another 30% stake will be set aside

for farmers through out-grower companies and the rest (19%) to be sold to the public through

IPOs at a later time when the factories are operating profitably. This proposal is however await-

ing parliamentary approval. Mumias sugar has indicated its willingness to bid for one of the 5

sugar factories as a strategic investor, possibly Nzoia sugar which has a 13% market and is capa-

ble of increasing Mumias’ market share to 58%.

The expiry of the safety window will usher in duty free quota sugar imports into the country

without paying duty. This is expected to offer competition to local millers as some of the Comesa

countries like Zambia, Sudan, Egypt and Swaziland produce their sugar at almost half the cost of

our local millers. As at end of 2009, the cost of locally produced sugar was USD 500 per ton as

compared to Comesa countries at USD 230-300 per ton making imported sugar cheaper than the

one produced locally.

Chemelil

5%

Muhoroni

5%

Mumias

45%Nzoia

13%

South Nyanza

12%

West Kenya

13%

Soin

0%

Kibos

7%

Market Shares for Sugar Production by Factory

2009

4. Mumias Sugar Research Update KESTREL CAPITAL

Constraints facing the sugar sector in Kenya

The sugar sector in the country is faced with several challenges that need to be addressed before

local millers can compete favorably with their peers from Comesa region. These challenges can

be grouped into two main categories; at farm level and factory level. According to a survey done

by Kenya Sugar Research Foundation (‘KESREF’), the main constraints can be summarized as:

• High input and production costs. Kenya has the highest sugar production cost in the Co-

mesa region. It is estimated that it costs USD 500 to produce a ton of Kenyan sugar, while a

ton of sugar from Comesa countries like Zambia, Malawi, Swaziland/Egypt and South Af-

rica (non-Comesa) costs USD 260, USD 230, USD 300, and USD 270, respectively. Inputs

costs for fertilizers and transportation are equally too high. It is estimated that transportation

alone takes about 30%- 40% of the cane price, while production costs like land preparation,

purchase of seed cane and fertilizers plus harvesting costs combine to eat into farmers’ as

well as millers’ margins.

• Small farm holdings: The average land size for cane production has been declining in the

inverse proportion to population growth. Most farmers own land measuring less than an hec-

tare making it un-economical for cane production. On average, the millers’ nucleus estates

account for about 6% of the total area under cane with the bulk of it, 94%, being small farm

holdings controlled by individual farmers. This is the biggest setback to attaining a competi-

tive edge since the companies are unable to exercise proper farming methods on individual

farms due to lack of economies of scale and the difficulty of enforcing proper farming meth-

ods in farms they don't own. In comparison, countries like Zambia, Swaziland and Malawi

are able to use mechanized farming, irrigation and controlled farming because of the large

nucleus estates they own.

Source: Kenya Sugar Board

3,200

3,400

3,600

3,800

4,000

4,200

4,400

40,000

45,000

50,000

55,000

60,000

65,000

2002 2003 2004 2005 2006 2007 2008 2009

Outgrowers Nucleus Estate

5. Mumias Sugar Research Update KESTREL CAPITAL

• Low cane yield, calculated as the total sugar produced per hectare. The sector average cane

yield currently stands at 6.43 T/Ha, which is far below the potential yield of 10.00 T/Ha un-

der rain fed conditions. Mumias’ yield in 2009 was 6.73T/Ha, slightly above the sector aver-

age.

Source: Kenya Sugar

• Over–dependence on rain-fed cane. Over 90% of sugar produced in Kenya is milled in the

western region sugar belt which is a high altitude area and mostly depends on rain-fed cane.

Maturity of such cane is delayed to 18-24 months due to low temperatures and drought. On

its part, Mumias has received all the necessary approvals to set up a Greenfield project at the

coast which is a low altitude area. The company has identified 16,000 ha of land for its nu-

cleus estate (the current nucleus estate in the western region is 3,524 ha).

• Poaching. Most sugar millers have cited poaching as big risk to their businesses. This is

done either by competitors or several sugar jaggeries located in the sugar belts but have no

contracted farmers and neither own nucleus estates.

• Poor planning and coordination of activities by outgrower and sugar companies has led to

poorly timed land preparation and planting, delayed supply of inputs especially fertilizer and

seed cane as well as delayed harvesting for most state owned millers save for Mumias.

• Delayed payment for delivered cane is a big disincentive to farmers who opt to uproot cane

in favor of other more viable crops. Mumias’ farmers are paid within 30 days for cane sup-

plied but some factories can take months.

• Lack of supervision and extension services by agriculture officers and sugar companies

leads to low standards of land preparation, weeding and harvesting.

• Poor road and telecommunication infrastructure serve to exacerbate the problem of cane

spillage and delayed transportation of cut cane to the factory.

• Low crushing capacity and inefficiency: This is occasioned largely by poor maintenance

of the factories and recurrent breakdowns. This in turn has reduced the crushing capacity of

some factories to as low as 50% of their installed capacities and recoveries to below 85%.

5.0

6.0

7.0

8.0

9.0

190,000

200,000

210,000

220,000

230,000

240,000

250,000

2005 2006 2007 2008 2009

Sugar Produced - Mumias (tons)

Area Harvested (ha)

Mumias Yield

Sector Yield

6. Mumias Sugar Research Update KESTREL CAPITAL

Expiry of Comesa Safeguards

In 2007, the government lobbied Comesa to extend the protectionist measure period by a further

4 years. This was based on grounds that the local sugar industry was not competitive enough to

allow duty-free sugar imports from Comesa, according to a study carried out. The Comesa exten-

sion safeguard measures came with the following conditions:

• Government to speed up privatization of all state controlled millers within two years.

• Government to effect a steady rise in sugar import quota in tandem with a graduated fall in

the duty charged with full liberalization by 2012 as shown in the table below.

Source: Comesa

• The pricing formula to be changed from the one based on cane weight to sucrose content

• Government to adopt an energy policy aimed at promoting co-generation and other forms of

bio-energy production to make the sugar industry more competitive

Most of the conditions outlined above have fallen behind schedule despite the remaining period

being less than 15 months. The four year period is the last that Kenya is allowed to have in the

governing rules of the Comesa treaty

Year

Duty Free quota

(Tons) Tariff quota (%)

2008/09 220,000 100

2009/10 260,000 70

2010/11 300,000 40

2011/12 340,000 10

1-Mar-12 Nil 0

7. Mumias Sugar Research Update KESTREL CAPITAL

Increasing annual consumption fuelling deficit

Below is a summary of sugar statistics in Kenya:

Source: Kenya Sugar Board

From the table, it is noteworthy that since the Comesa conditions kicked in from 2008, imports

have been declining which has in turn resulted into a deficit. This has been caused partly because

of the government’s suspension of import licenses in 2008 for some traders (leading to litigation

in court) and competitive prices in European markets for Comesa sugar producing countries.

There is also the effect of deficit in global supply of sugar due to drought in India and Brazil’s

policy governing the balancing of ethanol and sugar.

In the past 5 years, Kenya’s consumption has been growing at an average rate of 2.6% to peak at

762,027 tons in 2009 against a 5 year average production growth rate of 1.3% to 548,207 tons in

2009. This means there is still a lot of headroom for local millers if they are able to increase

their efficiency in sugar production to compete favorably. Some of the factories including

Mumias Sugar and Chemelil have started addressing the major factor that increases cost of pro-

duction; power. Mumias currently produces 38MW of power out of which 12MW is for internal

consumption and the rest, 26MW is sold to the national grid. Chemelil is partnering with Ken-

Gen, a power generation company, to produce 25MW of power.

Mrasurement (Tons) 2005 2006 2007 2008 2009

Production 488,997 475,670 520,404 517,667 548,207

Consumption 695,622 718,396 741,190 751,523 762,027

Imports 167,235 166,280 230,011 218,607 184,531

Exports 21,760 13,533 20,842 44,332 1,952

Defict 61,150 89,979 11,617 59,581 31,241

8. Mumias Sugar Research Update KESTREL CAPITAL

FY11 Forecast

We expect sugar production for Mumias to increase 11.0% to 261,729 tons in 2011 and 11.4%

increase in revenue to KES 17.3bn in 2012 buoyed by:

• Increased amount of rainfall in the sugar growing areas in western sugar belt that started in

4Q09 and has continued to date. In FY10 that ended 30 June 2010, the total rainfall recorded

in this region stood at 2,798mm, a 40% increase against a long term mean of 2,003mm. This

has the effect of improving cane yield and reducing maturity period from the normal 18-24

months to less. Excessive wet conditions may however result in damage to the road network

thereby increasing transportation costs and insufficient feedstock for milling.

• The company plans to increase area under cane by 10.5% from the current 57,393 ha to

63,393 ha over the next two years in the neighboring Busia Sugar zone. This is expected to

boost cane production by about 3% during the two years. Mumias has indicated that they

might bid for a stake in one of the government owned sugar companies when they are avail-

able for sale. This might significantly increase area under cane and boost its sugar produc-

tion. There has been suggestions that the neighboring Nzoia sugar which is less than 50km

from Mumias would be the more viable choice. If this happens, it has the potential of in-

creasing Mumias' area under cane by 28.8% to 80,650 ha.

• Increased efficiency. In 2009 Mumias recorded the highest Factory Time Efficiency (‘FTE’)

of 90.7%. Though this was below the recommended standard FTE of 92%, the factory is

addressing factors that result into low FTE. These include industrial action by workers over

pay, lack of cane due to strikes, bad roads, low feedstock and breakdown of equipment due

to ageing plant machinery. At the beginning of 1H10, the company carried out major repairs

and maintenance at a cost of KES 3bn which is expected to lead to increased availability of

the plant for longer grinding hours and increased efficiency. Also, improved sugar prices

which have been going up in tandem with a surge in global sugar prices will offer an upside.

Improved industry relations between the factory and workers, an increase in sugar prices

paid to farmers (19% increase to KES 2,768) is an incentive to farmers. Below is the trend in

for world sugar prices versus local prices in 2009.

Kenya Sugar Board , Bloomberg

9. Mumias Sugar Research Update KESTREL CAPITAL

Declining Profitability Margins

The high input costs are attributed to rising fuel prices, transport and fertilizer costs as well as an

increase in price of cane per ton paid to farmers have resulted in declining margins since 2005. Y

-o-y, operating margins declined 470bps to 9.2% Mumias paid an average of KES 2,768 per ton

to farmers in 2009 an increase of 19% as compared to 2009. It is estimated that transportation

alone takes about 30%- 40% of the cane price. The miller however cut back on cost of distribu-

tion by 3% to KES 2,788 per ton in FY10, compared to the previous year’s figure of KES 2,872

per metric ton as a result of direct sales deliveries to the customers.

Source: Company, Kestrel Capital Estimates

Sugar

Mumias plans to increase its production of its pre-packaged sugar to 40% of sugar produced after

commissioning of a new packaging plant in September 2009 and fortification of some of its

sugar with nutrients to make it attractive to consumers. Sugar is still the biggest contributor to

revenues for Mumias. In FY10, Sugar sales accounted for 97% of net revenues as compared to

electricity with 2% and molasses (to be used for ethanol production) 1%. Mumias’ plans to di-

versify into the smaller two revenue streams is informed by the above concentration risk in sugar

products. The target is to have the other two categories of power and ethanol contributing 10%

each so that sugar sales proportion can come down to 80%.

Power Generation

The KES 4.2 billion power plant, commissioned in May 2009 and which commenced full opera-

tions in January 2010, generates 38MW of power The company sells 26 MW of power at a price

of US cents 6/KWh to Kenya Power. In FY10, power sales contributed 2.3% to net revenues

(KES 359m). The low sales were attributed to low cane supply (hence less bagasse) and a low

uptake by Kenya Power. We project power to contribute at least KES 700m (approximately 4.5%

of net revenues) to revenues if the plant is operating at full capacity.

-5%

0%

5%

10%

15%

20%

0%

5%

10%

15%

20%

25%

30%

35%

40%

2002 2003 2004 2005 2006 2007 2008 2009

Gross margin (%) - RHS Operating margin - LHS

10. Mumias Sugar Research Update KESTREL CAPITAL

Ethanol Production

Mumias plans to start large scale industrial production of ethanol in a project to be financed

through debt and equity. The miller has signed a KES 1.6bn loan agreement with a consortium of

three banks; Ecobank, Nedbank and Commercial Bank of Africa for construction of an ethanol

plant that is estimated to cost KES 4bn. Some of the cash might be raised from the company’s

reserves (in FY09/10, Mumias Sugar reported KES 6.4bn in retained earnings). The company’s

80,000Mt of molasses is able to produce 24m hectolitres annually of Anhydrous Alcohol (AA)

for blending with petrol once complete from end of next year. The government has already put a

policy framework in place requiring all oil companies operating in western major towns of El-

doret, Kisumu and Nakuru to blend gasoline with 10% ethanol to produce ethanol. The imple-

mentation of this directive is however behind schedule due to capacity constraints.

Bottled Water

Mumias will start bottling water from its excess water from the co-generation treatment plant

with a capacity to produce 16m litres per year. This is expected to be completed by mid next

year.

Tarda Project

Mumias signed a deal with the Tana and Athi Rivers Development Authority (‘Tarda’) to set up

a sugar factory project in the Tana region. This project is expected to boost sugar production by

220,000 metric tons annually on completion. The project, expected to cost KES 32 billion, was

supported by an Environmental Impact Assessment (EIA) study report prepared by M.A. Con-

sulting Group (Kenyan) and HVA International (Danish). The project has already received ap-

proval from the National Environmental Authority (‘Nema’).

Results from the study indicate that cane from the delta region matures faster at 14 months as a

result of the low altitude, high temperatures and irrigation. This will be a sharp contrast to the

current 18-24 months in the western region which are 100% rain-fed and are grown in the high

altitude and low temperatures.

The company will be able to bring down the cost of production in this region by almost 40%

from the current USD 500 per ton to about USD 300 per ton. Also, the sucrose content will be

higher, making it comparable to more efficient sugar producers in the region such as Swaziland,

Malawi, Sudan and Zambia. If successful, the project’s capacity is estimated at 6,000 tons per

day will include power co-generation of 45 MW and ethanol production of up to 24 million li-

ters. The project will be supported by a nucleus estate of about 16,000 ha with the remaining

4,000 ha being used for development of other cane varieties or held by out-grower farmers.

The structure of the project will be such that Mumias will hold a 51% stake, Tarda 29%, the

local community 10% and a strategic investor 10%.The company is still in the process of sourc-

ing for funds and a strategic investor to finance this project; expected to be a mix of debt and

equity.

11. Mumias Sugar Research Update KESTREL CAPITAL

Income statement year to June FY2007 FY2008 FY2009 FY2010 FY2011 FY2012

Sales 10,318 11,954 11,738 15,568 17,336 19,538

Gross profit 3,588 4,266 3,311 4,885 5,547 6,545

Operating profit 1,880 1,666 1,084 1,965 2,138 2,764

Finance cost/income 29 (77) 109 215 307 307

Profit before tax 1,910 1,589 1,193 2,180 2,445 3,071

Taxation (516) (375) 417 (607) (577) (768)

Profit after tax 1,394 1,214 1,610 1,572 1,867 2,303

Dividends 765 612 612 612 612 612

Retained earnings 629 602 998 960 1,255 1,691

Balance sheet year to June

Fixed assets 8,003 9,280 12,098 11,586 15,886 15,886

Other non-current assets 210 292 265 241 241 241

Current assets 3,704 4,581 5,112 6,507 6,465 7,184

Total Assets 11,917 14,153 17,476 18,334 22,592 23,312

Shareholders equity 8,338 9,041 10,039 11,000 13,459 15,151

Non current liabilities 1,966 1,713 3,676 4,084 3,029 2,802

Current liabilities 1,613 3,398 4,158 3,250 7,790 7,046

Total equity and liabilities 11,917 14,153 17,873 18,334 24,279 24,999

Cash flow statement year to June

Cash generated by operations 2,472 2,258 1,847 2,897 3,295 4,035

Working capital (1,215) (551) 246 (248) (13) (193)

Operating Cash Flow 1,257 1,707 2,093 2,828 3,282 3,841

Net interest received/(paid) 34 (35) 67 181 307 307

Cash taxes (415) (217) (596) (5) (577) (768)

Net cashflow before investing 876 1,455 1,563 3,004 3,012 3,381

Net cash invested (1,343) (1,974) (3,173) (323) (5,458) (1,271)

Free cash flow (468) (519) (1,610) 2,682 (2,446) 2,110

Net financing cash flow (805) 86 1,020 (938) (1,973) (840)

Net cash flow for the year (1,273) (433) (590) 1,743 (4,419) 1,270

Opening cash balance 1,899 626 193 (397) 1,346 (3,072)

Closing cash balance 626 193 (397) 1,346 (3,072) (1,802)

12. Mumias Sugar Research Update KESTREL CAPITAL

Recommendation guide

STRONG BUY: Highly undervalued/ strong fundamentals

BUY: Good value/ strong fundamentals

ACCUMULATE: Buy on price dips

HOLD: Correctly valued with little pricing upside or downside

LIGHTEN: Overvalued by the market/ Reduce exposure/Declining fundamentals/

industry concerns

SELL: Weak fundamentals and challenging operating environment/Highly

overpriced

Disclaimer

Note: Readers should be aware that Kestrel Capital (EA) Ltd does and seeks to do business with companies covered in its research

reports. Consequently, a conflict of interest may arise that could affect the objectivity of this report. This document should only be

considered a single factor used by investors in making their investment decisions. The reader should independently evaluate the

investment risks and is solely responsible for their investment decisions.

The opinions and information portrayed in this report may change without prior notice to investors. This publication may not be distrib-

uted to the public media or quoted or used by the public media without prior and express written consent of Kestrel Capital (EA) Ltd.

Directors, staff of Kestrel Capital (EA) Ltd and their family members, may from time to time hold shares in the company it recommends

to either buy or sell and as such the investor should determine for themselves the applicability of this recommendation.

This document does not constitute an offer, or the solicitation of an offer, for the sale or purchase of any security. Whilst every care

has been taken in preparing this document, no representation, warranty or undertaking (express or implied) is given and no responsi-

bility or liability is accepted by Kestrel Capital or any employee of Kestrel Capital as to the accuracy of the information contained and

opinions expressed herein.