Why This Mattersto You

• ACCOUNTING You need to understand mergers, leveraged buyouts, and divestitures of assets to record and

report these organizational changes; you also need to understand bankruptcy procedures because you will play a

large part in any reorganization or liquidation.

• MANAGEMENT You need to understand the motives for mergers so that you will know when and why a merger is

a good idea. Also, you may need to know how to fend off an unwelcome takeover attempt, when to divest the firm

of assets for strategic reasons, and what options are available in the case of business failure.

• MARKETING You need to understand mergers and divestitures, which may enable the firm to grow, diversify, or

achieve synergy and therefore require changes in the firm’s marketing organization, plans, and goals.

• OPERATIONS You need to understand mergers and divestitures because ongoing operations will be significantly

affected by these organizational changes. Also, you should know that business failure may result in reorganization

of the firm to provide adequate financing for ongoing operations.

3.

Learning Objectives:

1. Understandmerger fundamentals,

2. motives for merging,

3. types of mergers.

4. Acquisitions , definition and types

5. LBOs and Divestitures

6. Analyzing and Negotiating Mergers

4.

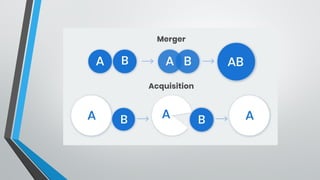

Fundamentals

• Mergers andacquisitions are transactions of shifting ownership

between two companies, wherein a merger is a fusing or combining

of two companies and acquisition is one company acquiring or

buying another. The ultimate goal of mergers and acquisitions is to

create synergy, which typically makes the two combined companies

worth more valuable than the two separate companies.

6.

First : Merger

•Definition:

• A merger is a corporate strategy of combining or fusing two separate companies into a single company in order

to enhance financial and operational strengths.

There are mainly two concepts in a merger:

• ● Acquiring Company: The company which purchases the majority of equity shares of other companies.

• ● Acquired Company: It sells most of the shares to the acquiring company.

• Friendly versus Hostile Takeovers

• friendly merger : A merger transaction endorsed by the target firm’s management, approved by its stakeholders, and easily

consummated.

• hostile merger: A merger transaction that the target firm’s management does not support, forcing the acquiring company to try to

gain control of the firm by buying shares in the Marketplace.

Forms of Acquisition

•Generally, there are two forms of acquisition- stock purchase and asset purchase.

• Stock Purchase

• In a stock purchase, the acquiring company pays cash or shares to the shareholders of the target firm for the shares of the

target company. Here the target company's shareholders receive compensation.

• In this case;

• ● The acquirer company takes all the assets and liabilities from the target company.

• ● Shareholders must approve the transaction through a majority vote to receive the

• compensation by the acquirer. This can be a long process.

• ● Shareholders bear tax responsibility as they receive the compensation.

• Asset Purchase

• Asset purchase means the acquirer purchases the target company's assets and pays the target directly.

• Here;

• ● The acquirer will avoid assuming any of the acquired company's liabilities, as it

• purchases only the assets.

• ● In this purchase, no shareholder approval is needed unless the assets are significant.

11.

Motives and Benefitsof Mergers and Acquisitions

• Unlocking Synergies

The most common goal of M&A is to create synergies, in which the merged company is worth

more than two individual companies.

• Economies of scale

When two companies merge together, it becomes more potent with abundant resources. After

merging, the newly developed company will get access to a more skilled workforce that will help

in increasing its scale of operations. Economies of scale will occur when a company uses its

resources efficiently and has an optimum distribution of networks, research, and development

facilities.

• Higher Growth

Mergers and acquisitions are the faster ways for a company to get higher revenues as

compared to growing organically and individually.

12.

Motives and Benefitsof Mergers and

Acquisitions

• Diversification of Products and Services

One of the most significant reasons for M&A is to introduce diversification into the products and services of a

company. Sometimes it reduces the risk of failure as it facilitates a company to merge with a company that is already

established. It also allows the former to explore new business operations.

• Eliminations of Competition

M&A of two or more companies eliminate competition in an industry. It saves the advertising cost of the company,

and it enables the merged company to reduce the cost of its products and services. It will also favor the customers

since they will get the products at lower prices.

• Stronger Market Power

The merged or acquired companies will attain a higher market share and will gain the power to manipulate prices

due to cost-cutting.

• Best Financial Planning

When one or more companies decide for a merger or acquisition, they can plan to utilize their resources in the best

possible way. The funds and finances of a merged or acquired company will be more and their utilization may

accordingly be better than in the separate units.

13.

LBOs and Divestitures

•leveraged buyout (LBO) An acquisition technique involving the use of a large amount of debt to purchase a firm; an example of a financial

merger..

• operating unit A part of a business, such as a plant, division, product line, or subsidiary, that contributes to the actual operations of the firm.

• Divestiture The selling of some of a firm’s assets for various strategic reasons.

• spin-off A form of divestiture in which an operating unit becomes an independent company through the issuance of shares in it, on a pro rata

basis, to the parent

company’s shareholders An attractive candidate for acquisition via a leveraged buyout should possess

three key attributes:

1. It must have a good position in its industry, with a solid profit history and

reasonable expectations of growth.

2. The firm should have a relatively low level of debt and a high level of “bankable”

assets that can be used as loan collateral.

3. It must have stable and predictable cash flows that are adequate to meet

interest and principal payments on the debt and provide adequate working

capital.

14.

• Four methodscompanies used to divest themselves of operating units

the sale of a product line to another firm.

The sale of the unit to existing management through the use of leveraged buyout (LBO)

spin-off, which results in an operating unit becoming an independent company

liquidation of the operating unit’s individual assets.

breakup value The value of a firm measured as the sum of the values of its operating units if each were

sold separately.

LBOs and Divestitures

15.

Acquisitions of Assets

Occasionally,a firm is acquired not for its income-earning potential but as a collection

of assets (generally fixed assets) that the acquiring company needs.

Acquisitions of Going Concerns

Acquisitions of target companies that are going concerns are best analyzed by

using capital budgeting techniques similar to those described for asset acquisitions.

The methods of estimating expected cash flows from an acquisition are

similar to those used in estimating capital budgeting cash flows.

Analyzing and Negotiating

Mergers

16.

• stock swaptransaction

An acquisition method in which the acquiring firm exchanges its shares for shares of the

target company according to a predetermined ratio.

ratio of exchange

The ratio of the amount paid per share of the target company to the market price per share

of the acquiring firm

Analyzing and Negotiating

Mergers

17.

Initial Effect Whenthe ratio of exchange is equal to 1 and both the

acquiring firm and the target firm have the same premerger earnings per share,

the merged firm’s earnings per share will initially remain constant. In this rare

instance, both the acquiring firm and the target firm would also have equal

price/earnings (P/E) ratios. In actuality, the earnings per share of the merged firm

are generally above the premerger earnings per share of one firm and below the

premerger earnings per share of the other, after the necessary adjustment has been

made for the ratio of exchange.

Analyzing and Negotiating

Mergers

18.

Long-Run Effect Thelong-run effect of a merger on the earnings per share of

the merged company depends largely on whether the earnings of the merged firm

grow. Often, although an initial decrease in the per-share earnings of the stock held

by the original owners of the acquiring firm is expected, the long-run effects of the

merger on earnings per share are quite favorable. Because firms generally expect

growth in earnings, the key factor enabling the acquiring company to experience

higher future EPS than it would have without the merger is that the earnings attributable

to the target company’s assets grow more rapidly than those resulting from

the acquiring company’s premerger assets. An example will clarify this point..

Analyzing and Negotiating

Mergers

19.

Effect on MarketPrice per Share

The market price per share does not necessarily remain constant after the acquisition

of one firm by another. Adjustments occur in the marketplace in response

to changes in expected earnings, the dilution of ownership, changes in risk, and

certain other operating and financial changes

RE = ratio of exchange

MP target = market price per share of the target firm

MP acquiring = market price per share of the acquiring firm

MPR = market price ratio of exchange

MPR = MP acquiring*RE/MP target

Analyzing and Negotiating

Mergers