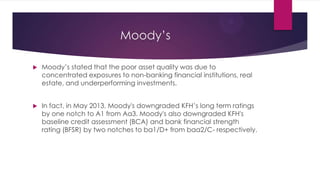

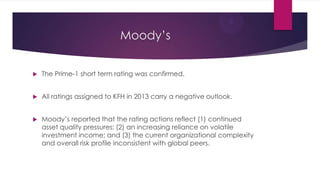

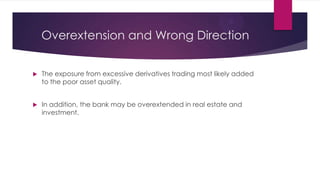

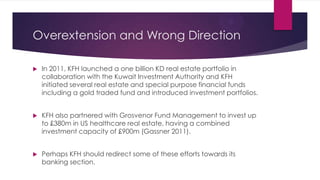

Downloaded 76 times

Through analyzing Kuwait Finance House's financial ratios and accounting practices, this document aims to evaluate the current state of financial reporting in Islamic banking. The analysis finds that KFH has weak liquidity and declining profitability ratios from 2009-2011. Its use of debt financing has also increased its credit risk. KFH's accounting practices are also inconsistent, as it selectively follows IFRS and AAOIFI standards without fully adhering to either. This creates gaps in disclosure and transparency. Moody's has downgraded KFH's ratings due to asset quality issues and an overreliance on volatile investment income. The document recommends KFH improve its financial reporting consistency and practices.