Download to read offline

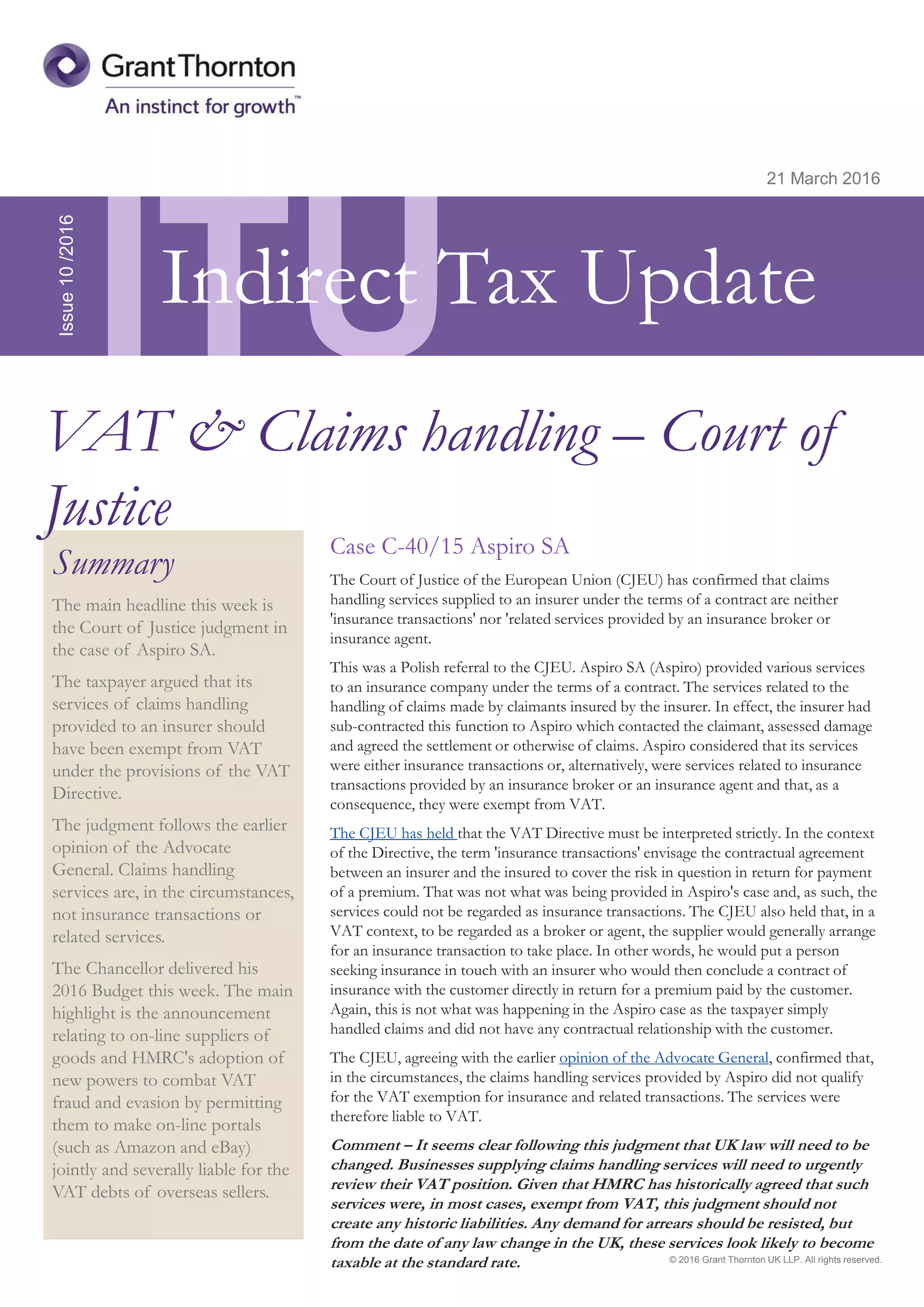

The document summarizes two key developments from the past week: 1) A Court of Justice ruling found that claims handling services provided to an insurer are not exempt from VAT as insurance transactions or related services. UK law will need to change and businesses providing these services should review their VAT position. 2) The UK budget announced new powers for HMRC to make online marketplaces jointly liable for VAT debts of overseas sellers on their platforms. This aims to reduce the estimated £365 million annual VAT loss from non-compliant foreign traders. Online portals will need to strengthen due diligence of sellers.