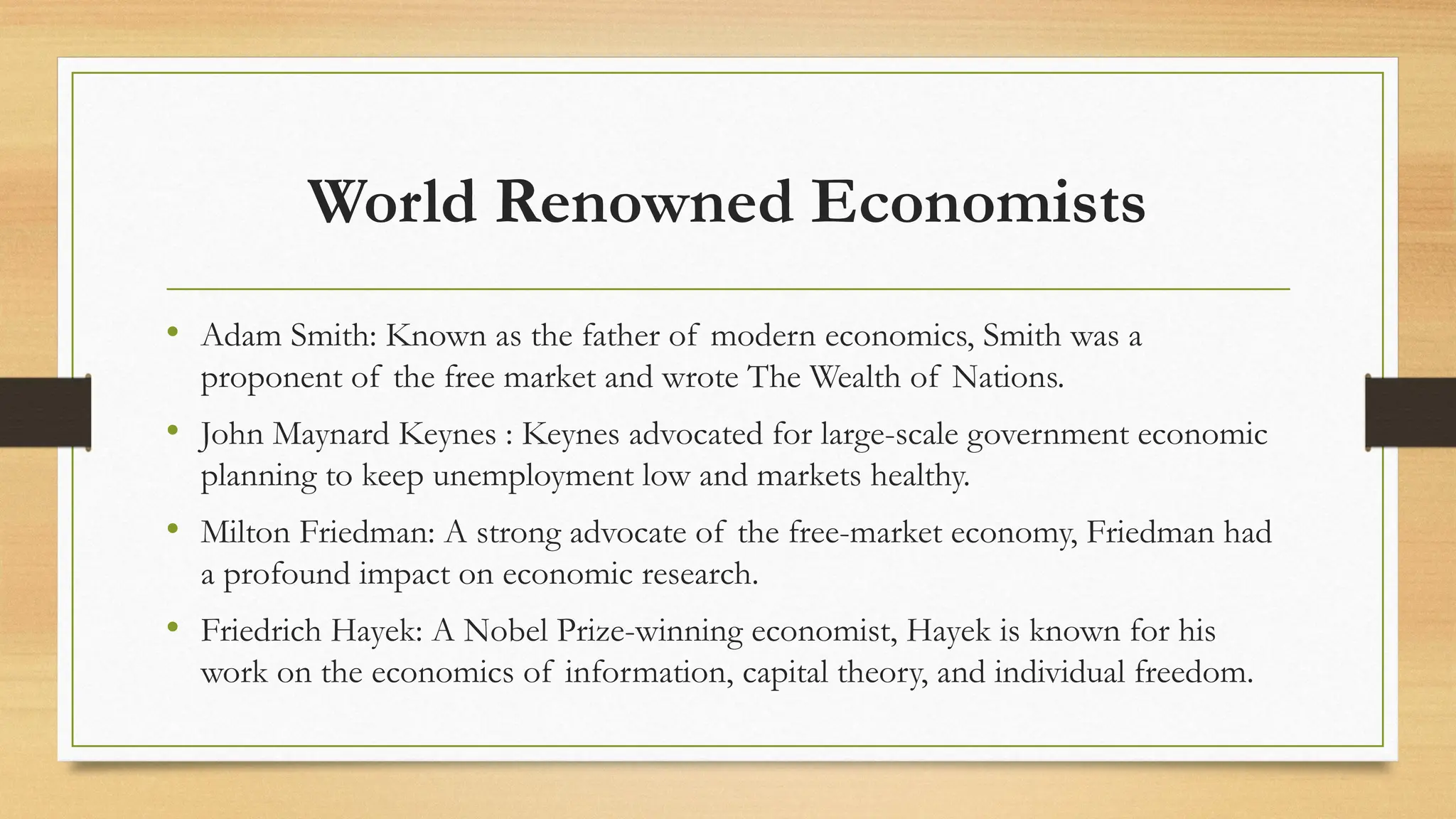

World Renowned Economists

•Adam Smith: Known as the father of modern economics, Smith was a

proponent of the free market and wrote The Wealth of Nations.

• John Maynard Keynes : Keynes advocated for large-scale government economic

planning to keep unemployment low and markets healthy.

• Milton Friedman: A strong advocate of the free-market economy, Friedman had

a profound impact on economic research.

• Friedrich Hayek: A Nobel Prize-winning economist, Hayek is known for his

work on the economics of information, capital theory, and individual freedom.

3.

• David Ricardo:A British political economist and stock trader, Ricardo is often

credited with systematizing economics.

• Karl Marx: Known for his theories on capitalism and communism.

• Amartya Sen: An Indian economist who won the 1998 Nobel Prize in Economic

Sciences for his contributions to welfare economics and social choice.

• Alan Greenspan: The Chairman of the Federal Reserve from 1987 to 2006,

Greenspan is believed to be one of the most influential economists of our time.

• Elinor Ostrom: The first and only woman to win the Nobel Prize for Economics,

Ostrom's theorizing of the commons opened the way for non-capitalist economic

alternatives.

4.

PRINCIPLES OF ECONOMICS

•Gregory Mankiw in his Principles of Economics outlines Ten Principles of Economics that we will replicate here, they are:

• People face trade-offs.

• The cost of something is what you give up getting it.

• Rational people think at the marginal cost and marginal revenue.

• People respond to incentives.

• Trade can make everyone better off.

• Markets are usually a good way to organize economic activity.

• Governments can sometimes improve market outcomes.

• A country's standard of living depends on its ability to produce goods and services.

• Growth of money leads to inflation

• Society faces a short-run tradeoff between Inflation and unemployment.

5.

Definition of Economics

•British economist Alfred Marshall defined economics as the study of how people earn and spend their

income in the course of their ordinary lives. He believed economics was a social science, not a natural

science like chemistry or physics.

• Marshall's definition of economics included the following ideas:

• Wealth and well-being: Economics is the study of wealth creation and how people use the wealth they

create.

• People at the center: Economics is centered on people, and other material aspects revolve around them.

• Social science: Economics is a social science, not a natural science like physics or chemistry.

• Marshall founded the Cambridge School, which focused on welfare economics, the theory of the firm,

and increasing returns.

Economic Analysis

• Economicanalysis is the evaluation of costs and benefits. It can help governments make the best use

of taxpayers' funds and generate maximum benefit for society.

• Budget impact analysis: Estimates the financial consequences of a proposed intervention

• Economic forecasting: Determines the future prosperity of an investment pattern

• Return-on-investment analysis: Measures the efficiency of an investment by dividing the benefit by

the intervention cost

• Economic assessment: Compares the expected costs and benefits of a proposal, policy, or regulation

• Business analysis: Helps companies identify needs, overcome difficulties, and attract capital

• Factor analysis: A specific type of economic analysis

• Financial and management analysis: Used by financial and credit organizations to improve

efficiency

8.

Economic Decisions

• Economicdecisions are made in a variety of ways, depending on the economic system in place:

• Mixed economy: Economic decisions are made by both the government and individuals. This

system is a combination of a command economy and a free market economy.

• Market economy: Economic decisions are made through markets, and are guided by price signals.

(USA, Canada, Germany )

• Traditional economic system: This basic system is based on established trends for goods, services,

and work. There is little specialization or division of labor.

• Command economic system: The government controls economic decision-making, including what

to produce, how much to produce, and who gets the products.

• Microeconomic decisions: This branch of economics focuses on the economic and financial

decisions made by individuals, households, and businesses.

• Capitalist economy: Private investors own the forms of equity and make economic decisions for

their businesses. (Hong Kong, Singapore, New Zealand, Switzerland, Australia, United States)

• All economies must make three basic decisions: what to produce, how to produce it, and who will

consume it.

9.

MICRO ECONOMIC ANALYSIS

•Microeconomics is concerned with how supply and demand interact in

individual markets for goods and services.

• Microeconomics shows how and why different goods have different values.

It addresses how individuals and businesses conduct and benefit from

efficient production and exchange and how individuals can best coordinate

and cooperate with each other.

10.

Basic Concepts ofMicroeconomics

• Incentives and behaviours

• Utility theory

• Production theory

• Price theory

11.

Where Is MicroeconomicsUsed?

• Policymakers may use microeconomics to understand the effect of setting a

minimum wage or subsidizing the production of certain commodities.

• Businesses may use microeconomics to analyze pricing or production

choices.

• Individuals may use it to assess purchasing and spending decisions.

12.

Theory of Firms

•In neoclassical economics—an approach to economics focusing on the

determination of goods, outputs, and income distributions in markets

through supply and demand—the theory of the firm is a microeconomic

concept that states that a firm exists and make decisions to maximize profits.

• Whether a company's goal is to maximize profits in the short-term or long-

term. Modern takes on the theory of the firm sometimes distinguish

between long-run motivations, such as sustainability, and short-run

motivations, such as profit maximization.

13.

• If acompany's goal is to maximize short-term profits, it might find ways to increase

efficiency, boost revenue and reduce costs. However, companies that utilize fixed

assets, like equipment, would ultimately need to make capital investments to ensure

the company is profitable in the long-term.

• If competition is strong, the company will need to not only maximize profits but

also stay one step ahead of its competitors by reinventing itself and adapting its

offerings. Therefore, long-term profits could only be maximized if there's a balance

between short-term profits and investing in the future.

14.

Forms of Ownership

•Limited Liability Company: A business that is a separate legal entity from its owners and directors. The company

enters into contracts, owns assets, and can be sued

• Sole proprietorship

• Partnership

• Publicly listed company

• One person company: A One Person Company (OPC) is a business structure in India that allows a single person to

own and operate a company. The Companies Act of 2013 introduced the concept of OPCs to promote entrepreneurship

and formalize small and medium-sized businesses.

• Private limited company

• Cooperative

• Hindu Undivided Family

• Section 8 Company: A Section 8 company is a non-profit organization (NPO) in India that promotes social welfare, the

arts, education, sports, science, research, and other causes. Section 8 companies are registered under the Companies Act

of 2013 and are exempt from some requirements of other commercial companies.

15.

PROFIT MAXIMIZATION THEORY

•Profit maximization theory is an economic theory that assumes a company's primary goal is to maximize

its profits. The theory also assumes that companies will choose the least expensive way to achieve this

goal.

• Profit maximization

• The point at which a company's profit is at its highest. This occurs when marginal revenue (MR) equals

marginal cost (MC). MR is the price per unit of a product or service, and MC is the cost per unit.

• Economic efficiency

• The theory suggests that profit-maximizing behavior leads to economic efficiency, which is the efficient

allocation of resources.

• Utilitarian thought

• The idea that maximizing both private and social benefit is the foundation of utilitarian thought.

• Competition

• The theory suggests that businesses should develop a sustainable competitive advantage over their rivals.