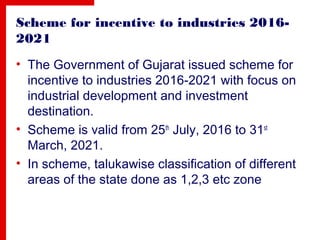

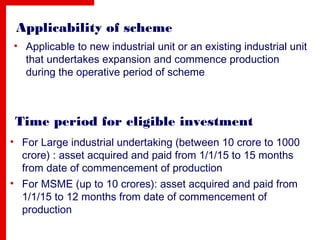

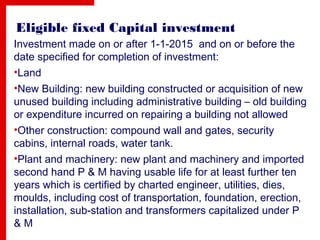

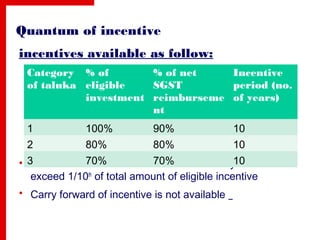

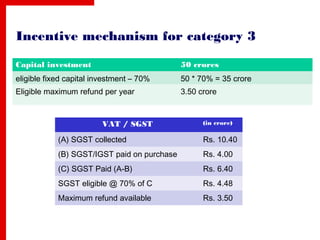

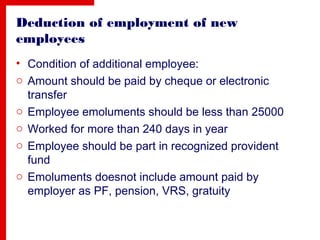

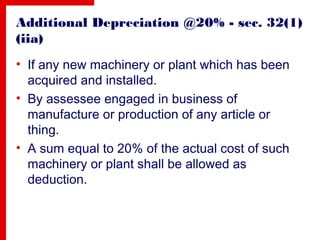

The Gujarat Industrial Policy 2016-2021 offers direct and indirect tax benefits aimed at boosting industrial development, applicable to both new and expanding existing units. The scheme includes a talukawise classification for incentive applicability, with specific eligibility criteria for investments and various categories of fixed capital investment. Additionally, it provides tax deductions for hiring new employees and outlines the incentive mechanisms based on eligible investment percentages and SGST reimbursement.

![[UPDATED] Gujarat Industrial Policy, 2020](https://cdn.slidesharecdn.com/ss_thumbnails/grupdated-gujaratindustrialpolicy2020-ppt-201008053258-thumbnail.jpg?width=640&height=640&fit=bounds)

![[UPDATED] Gujarat Industrial Policy, 2020](https://cdn.slidesharecdn.com/ss_thumbnails/grupdated-gujaratindustrialpolicy2020-ppt-201008053856-thumbnail.jpg?width=640&height=640&fit=bounds)