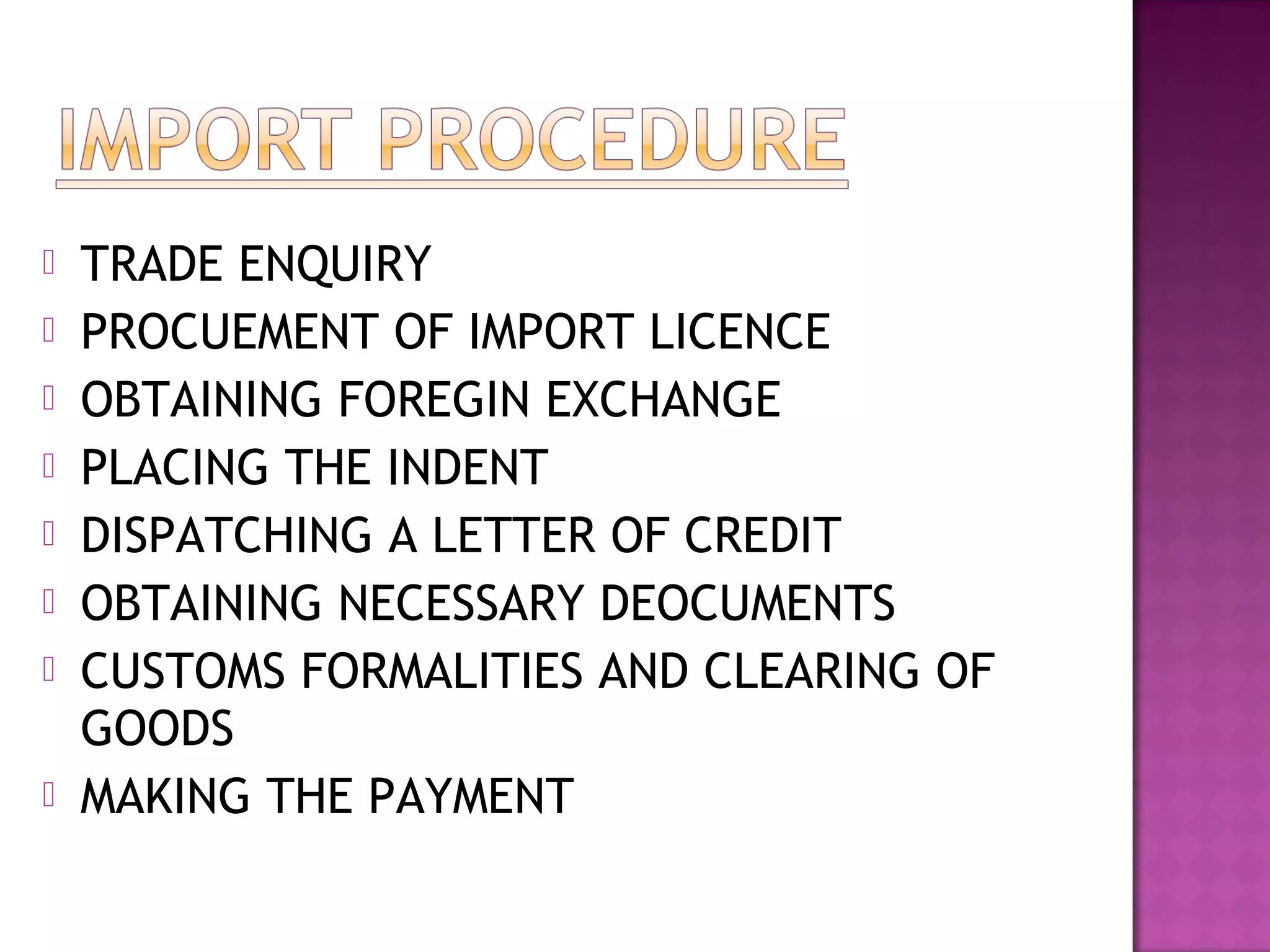

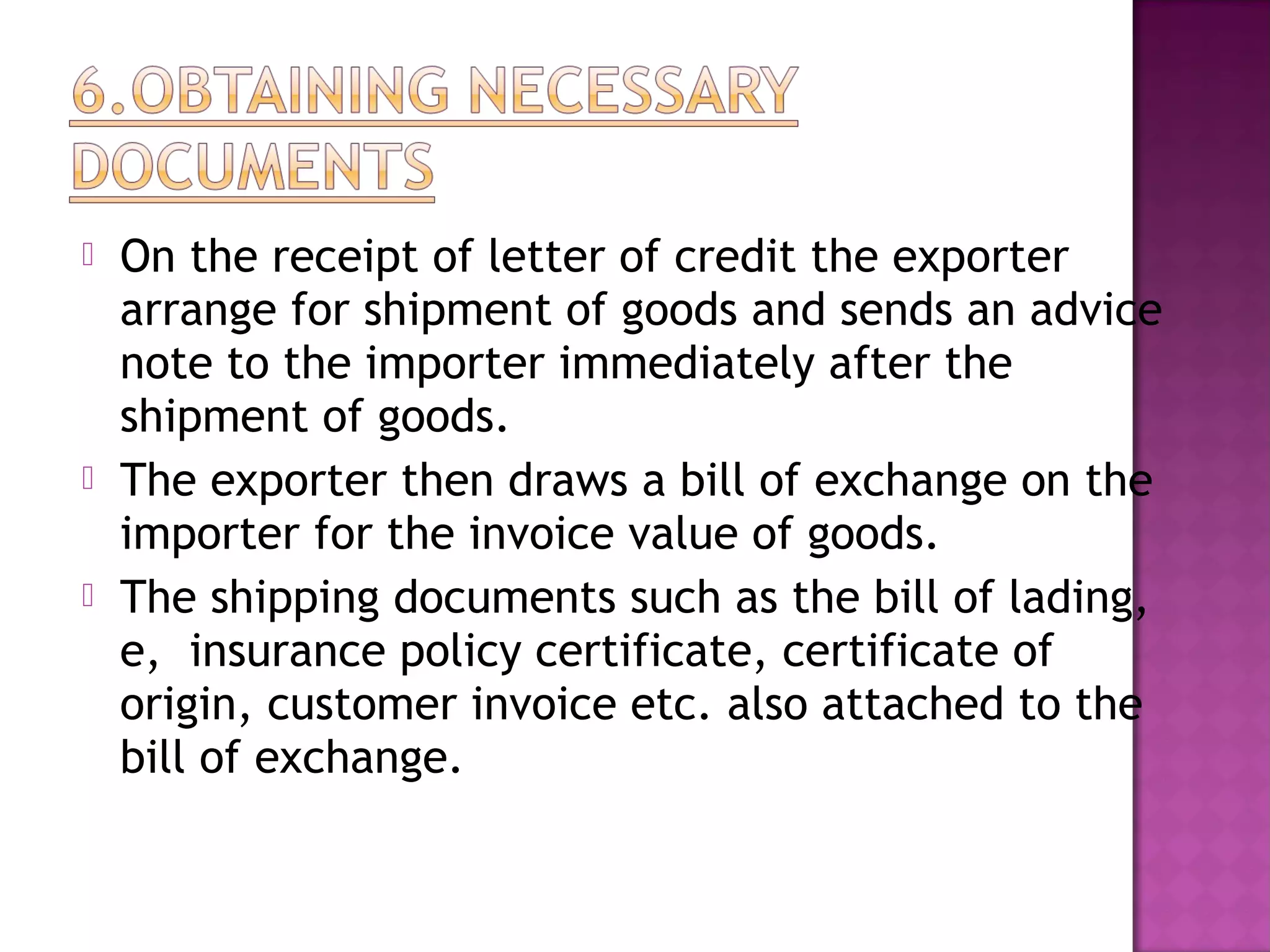

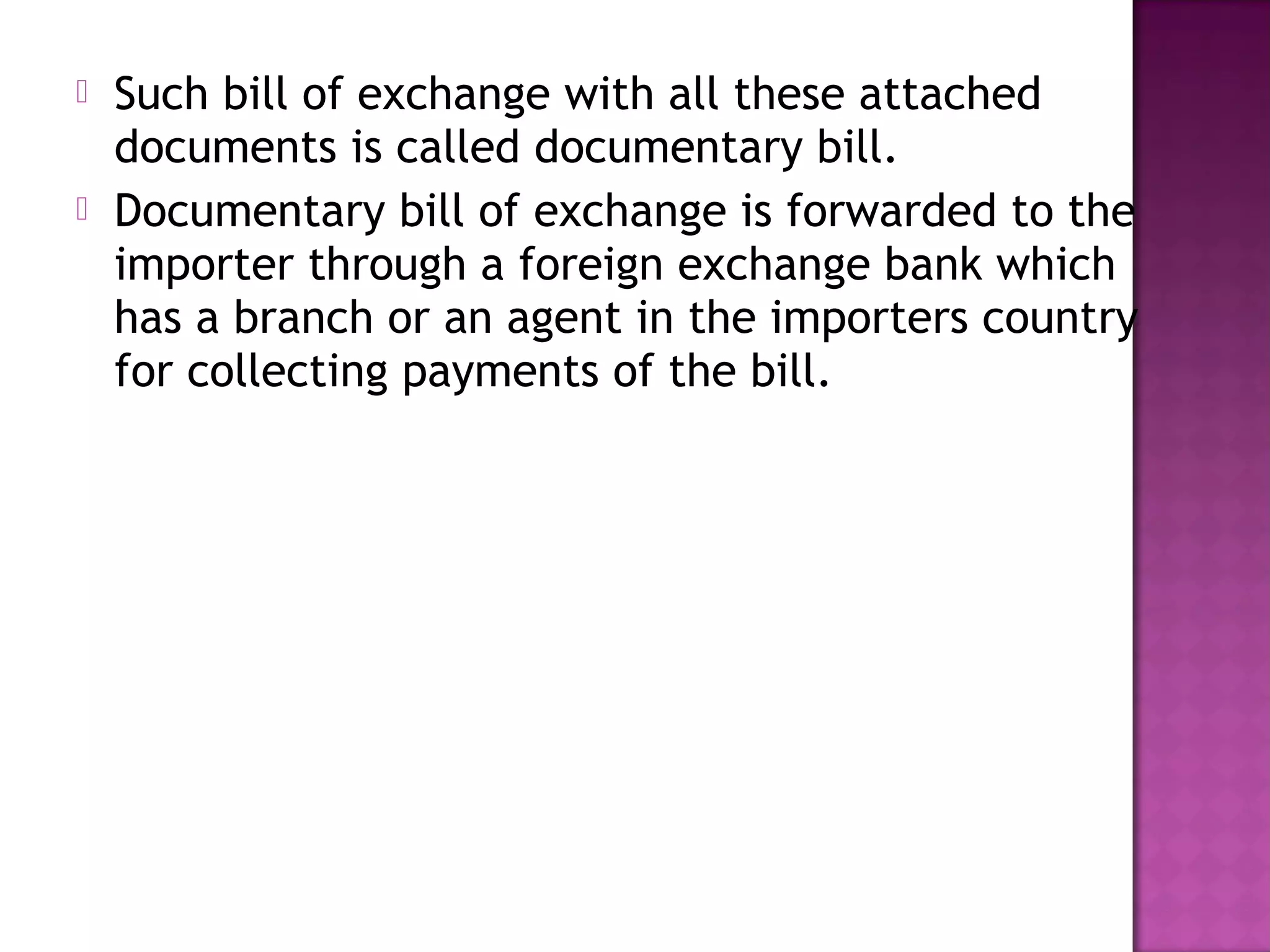

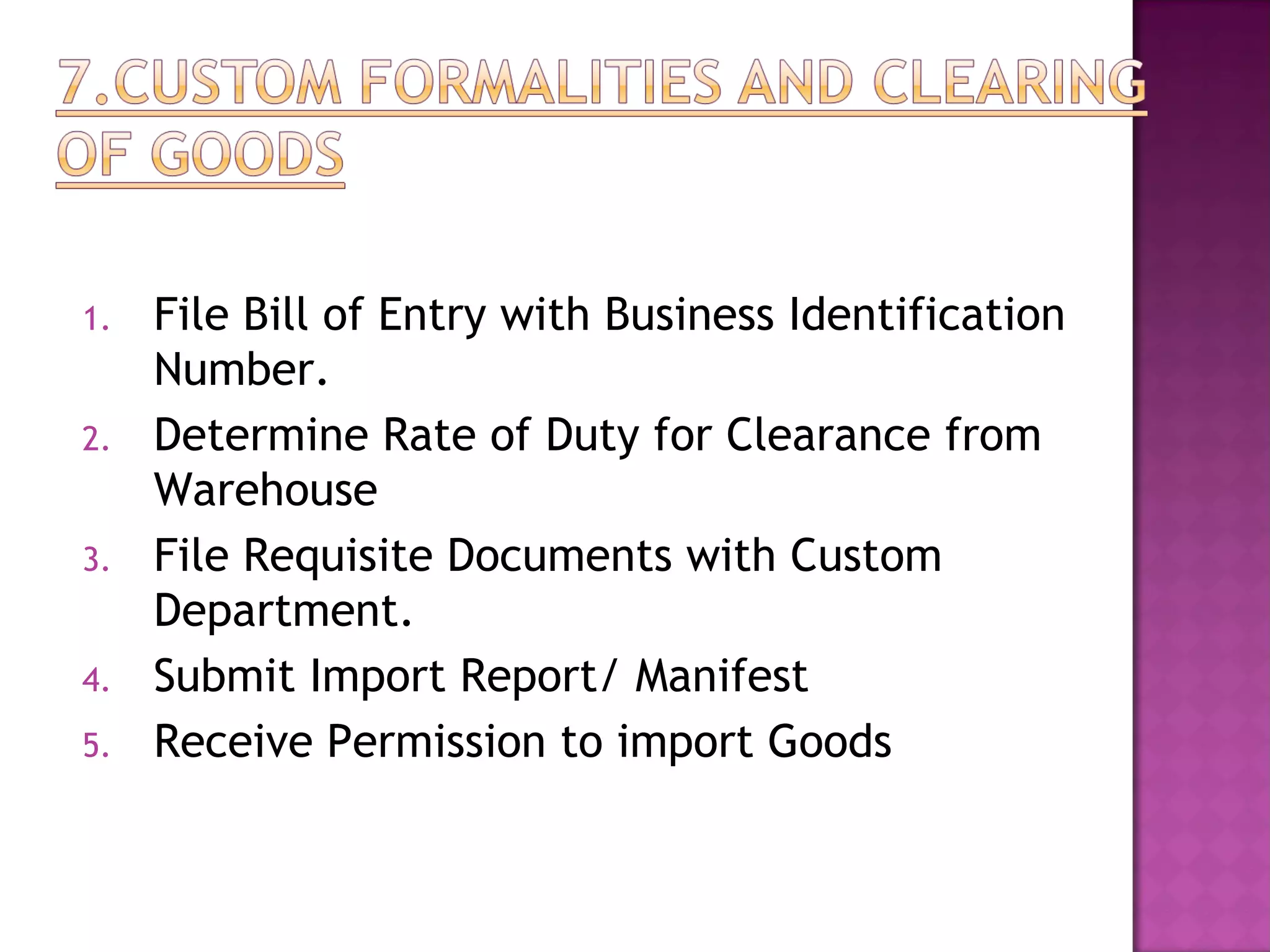

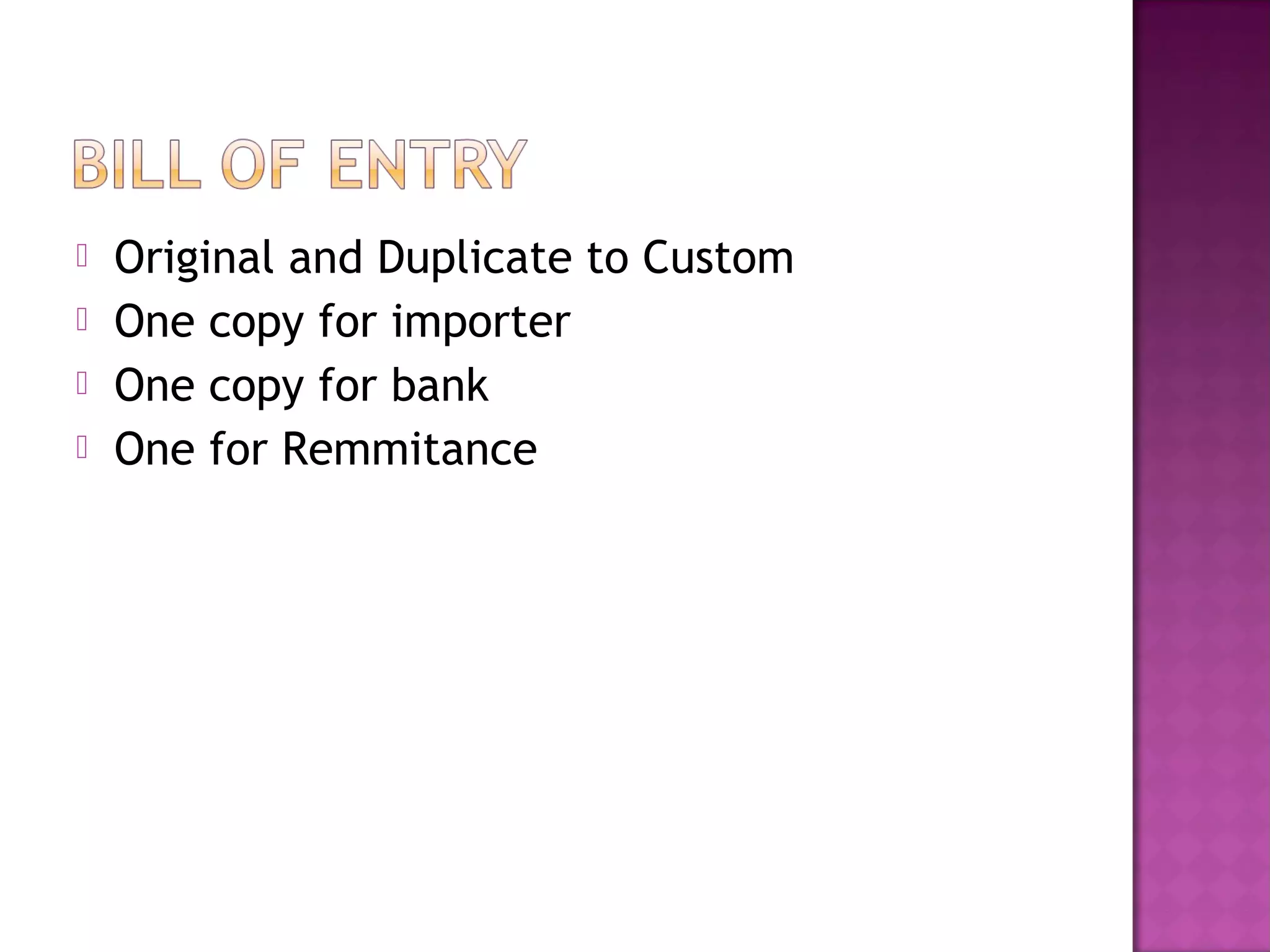

The document summarizes the key steps involved in the import trade process. It discusses that import procedures vary by country but generally involve trade enquiries, obtaining import licenses and foreign exchange, placing orders, obtaining necessary documents, customs clearance, and payment. Key import documentation and duties charged are also outlined. The overall process ensures government regulation of imports and facilitation of international trade transactions.