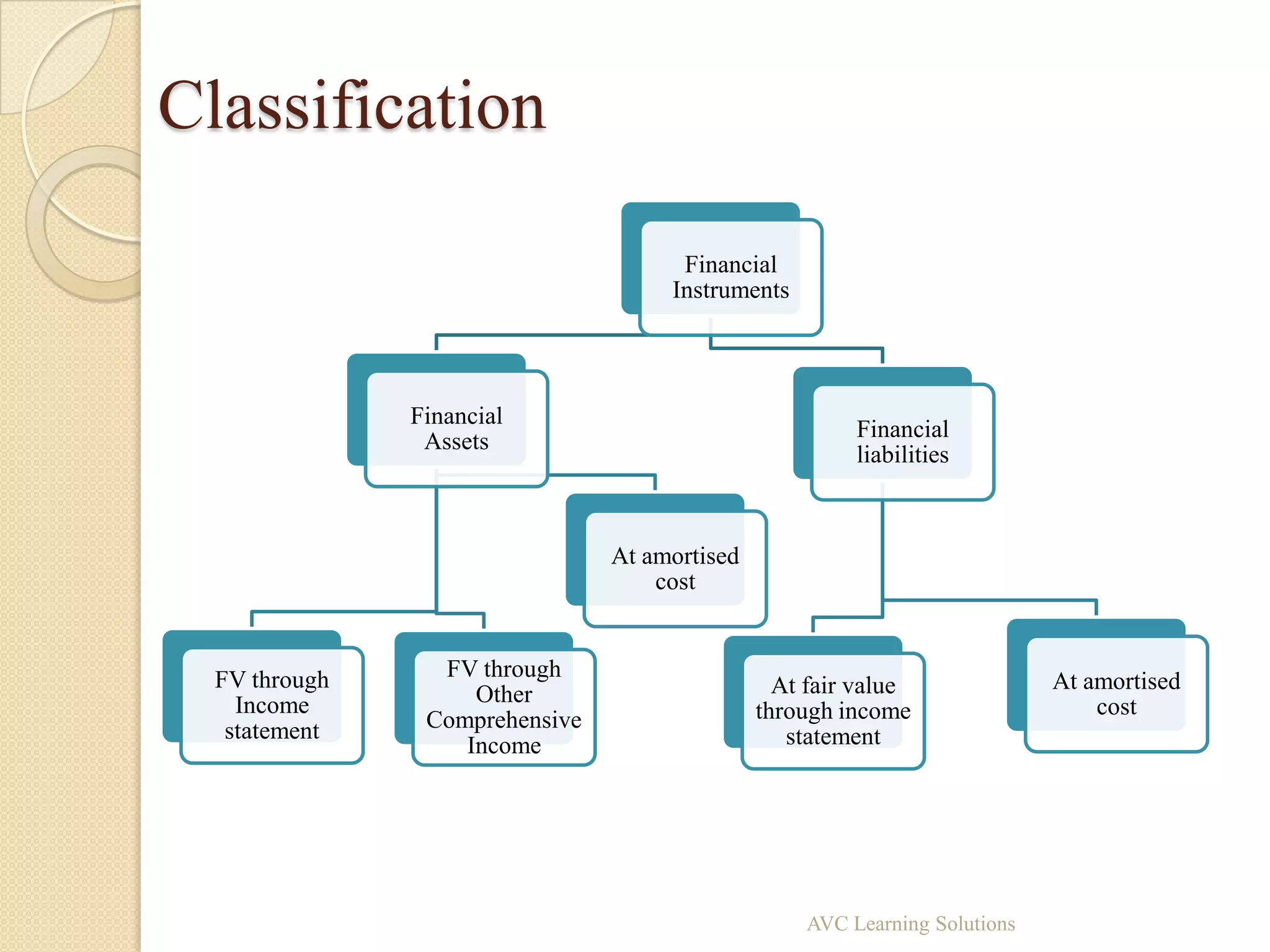

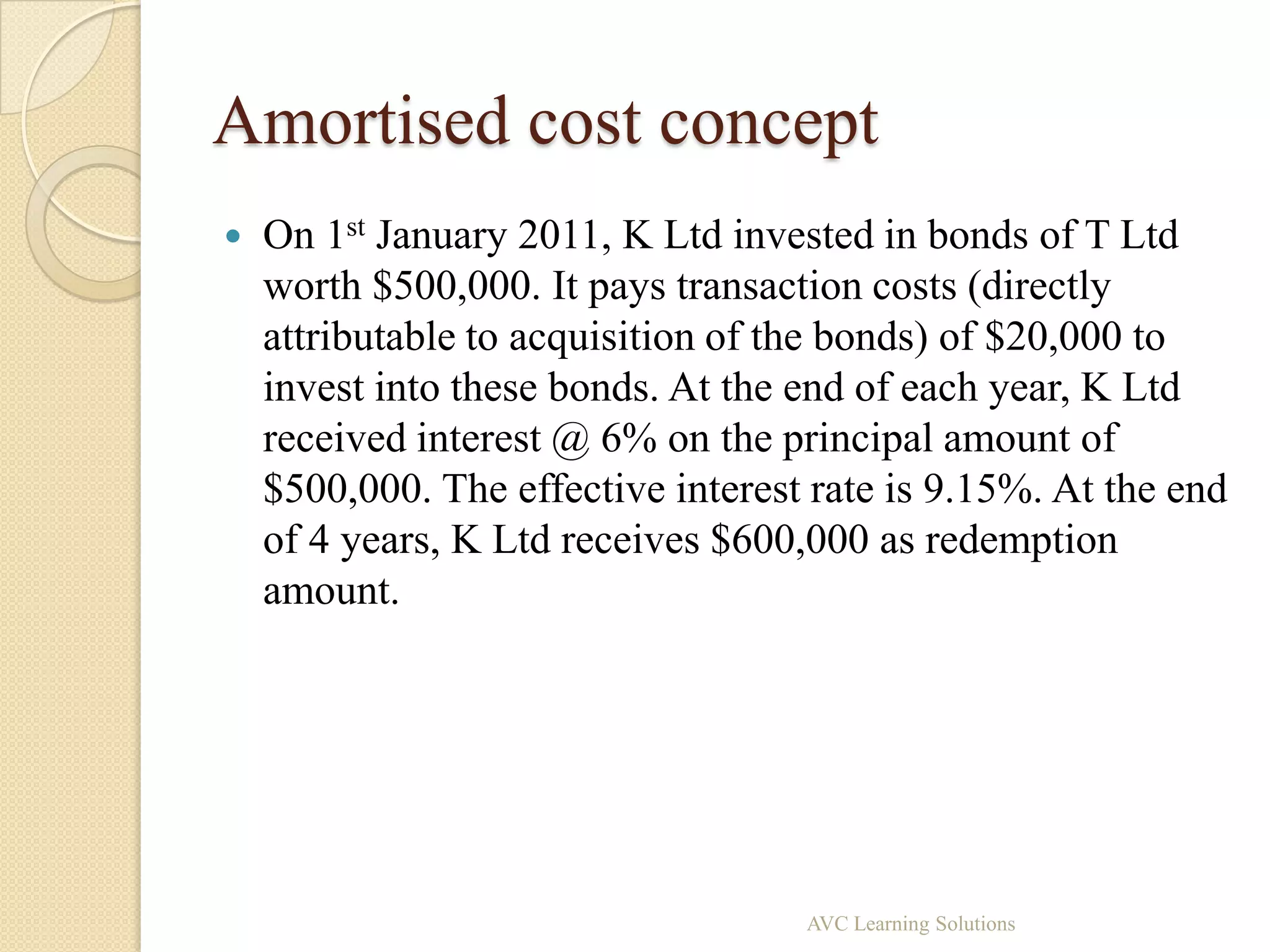

The document outlines the classification and measurement of financial assets and liabilities according to IFRS 9 and IAS 32/39, emphasizing distinctions between amortized cost and fair value. It provides examples of business models for financial assets, highlighting how entities like K Ltd approach cash flow collections and investment strategies. Additionally, the document discusses transaction costs related to financial instruments and initial measurement principles for financial assets and liabilities.