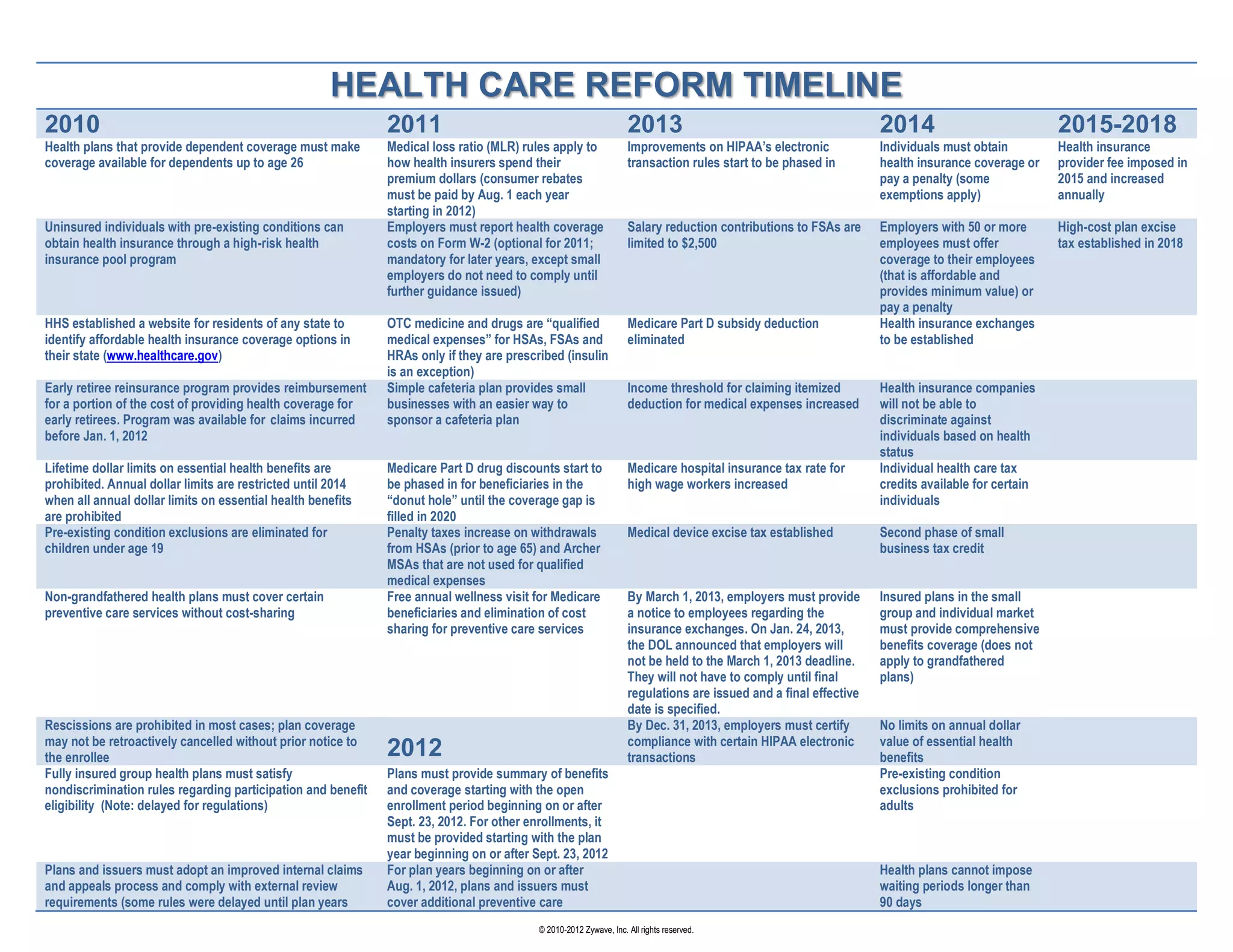

The timeline summarizes important dates in the implementation of the Affordable Care Act between 2010 and 2018. Key provisions include:

- 2010-2011: Dependent coverage must be offered until age 26 and pre-existing conditions can be covered through high-risk pools.

- 2011-2013: Medical loss ratio and electronic transactions rules apply, health care exchanges are established.

- 2014: Most individuals must have coverage or pay a penalty and health insurance market reforms take effect.

- 2015-2018: Additional taxes and fees are imposed on health plans, and remaining ACA provisions are implemented.

![Adp Affordable Care Act 112812 Final[1]](https://cdn.slidesharecdn.com/ss_thumbnails/adpaffordablecareact112812final1-13543760189508-phpapp02-121201093425-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![UBA Plan Related Reform Provisions04012010 Combined[1] 040210](https://cdn.slidesharecdn.com/ss_thumbnails/ubaplanrelatedreformprovisions04012010combined1040210-12705604099281-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)