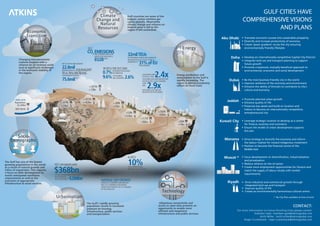

This document provides information on population growth, economic growth, energy production and consumption, and city planning visions for Gulf cities between 2000-2030. It notes that the Gulf region has experienced rapid population and economic growth, with average GDP growth of 5.7% compared to 1.6% for G7 economies. However, the region remains reliant on oil and has high per capita carbon emissions. The document outlines population projections and economic growth forecasts for each GCC country and lists the comprehensive visions and plans for their major cities, focusing on diversification, sustainability, and improving quality of life.