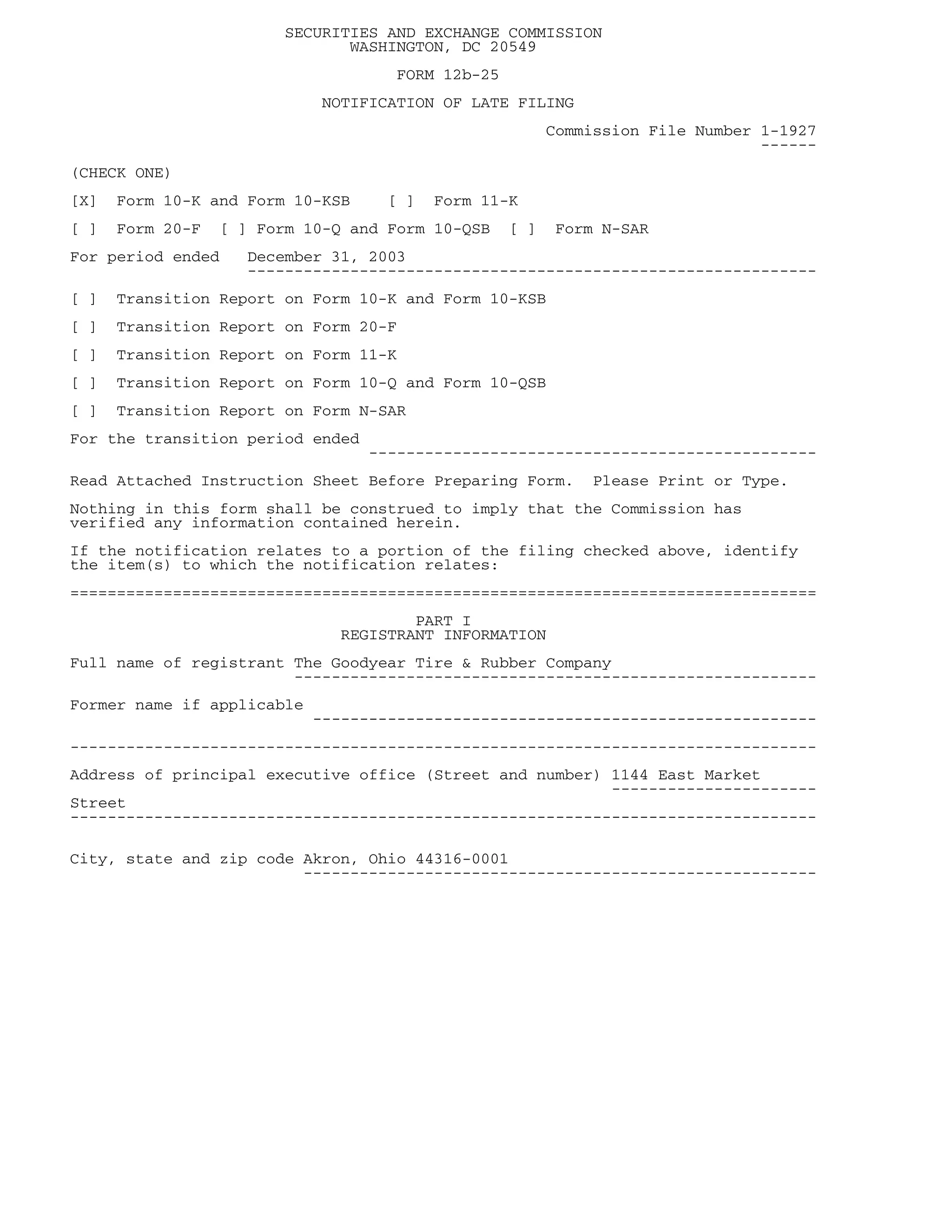

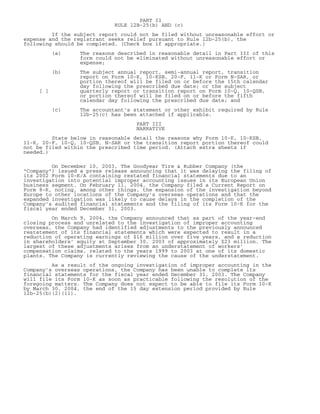

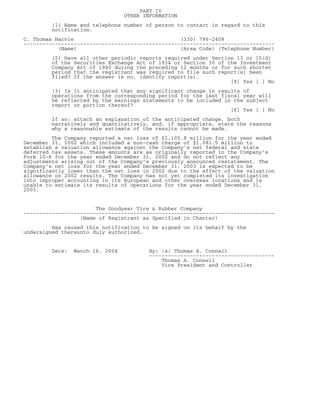

Download to read offline

The Goodyear Tire & Rubber Company filed a Form 12b-25 to notify that it would be unable to file its annual report (Form 10-K) for the fiscal year ending December 31, 2003 by the required deadline. The filing delay is due to an ongoing investigation into potential improper accounting in its European and other overseas operations. Goodyear also identified adjustments unrelated to the investigation that are expected to reduce previously reported earnings and equity. As a result of the ongoing investigation and adjustments, Goodyear has not completed its 2003 financial statements and cannot reasonably estimate its 2003 results of operations at this time.