Learning Objectives

• DefineStatement of Changes in Equity

• Identify the components

• Explain the purpose and importance

• Interpret a sample statement

3.

Definition

• The Statementof Changes in Equity shows the

movement in equity accounts during a period.

• Includes owner contributions, profits/losses,

withdrawals/dividends, and other changes.

4.

Purpose

• To providetransparency on equity movement

• Helps users understand how net income and

owner actions affect equity

5.

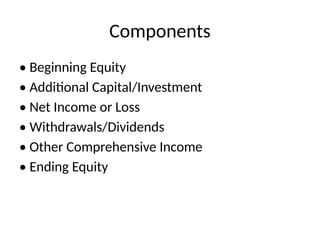

Components

• Beginning Equity

•Additional Capital/Investment

• Net Income or Loss

• Withdrawals/Dividends

• Other Comprehensive Income

• Ending Equity

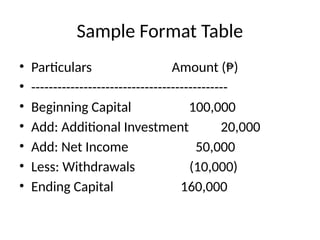

Sample Format Table

•Particulars Amount (₱)

• ---------------------------------------------

• Beginning Capital 100,000

• Add: Additional Investment 20,000

• Add: Net Income 50,000

• Less: Withdrawals (10,000)

• Ending Capital 160,000

10.

Example: Sole Proprietor

•• Juan started with ₱100,000

• • Invested another ₱20,000

• • Earned ₱50,000 net income

• • Withdrew ₱10,000 for personal use

• • Ending Equity: ₱160,000

11.

Example: Corporation

• •Includes Share Capital, Retained Earnings,

Reserves

• • More complex with dividends and Other

Comprehensive Income (OCI)

12.

Importance to Users

•For owners/investors: track returns

• For analysts: assess company stability

• For accountants: summarize changes in equity

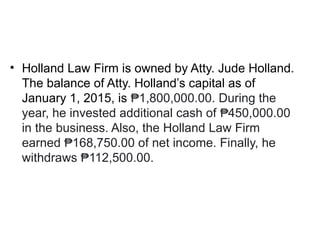

• Holland LawFirm is owned by Atty. Jude Holland.

The balance of Atty. Holland’s capital as of

January 1, 2015, is 1,800,000.00. During the

₱

year, he invested additional cash of 450,000.00

₱

in the business. Also, the Holland Law Firm

earned 168,750.00 of net income. Finally, he

₱

withdraws 112,500.00.

₱