Fundamental of partnership introduction of partnership

Here is the explanation of chapter fundamentals of partnership chapter 1.

Full chapter in less efforts.

In this ppt you will get all the headings and points of chapter.

ACCOUNTING FORPARTNERSHIPS FIRM

INTRODUCTION ABOUT TOPIC

1. Nature of partnership firms .

2. feature or Characteristics of partnership .

3. i. Rights of partner

3. ii. Limited Liability Partnership (LLP)

4. Partnership Deed. Articles of Partnership.

5. Rules of Applicable in the Absence of Partnership deed.

6. Format of Profit and loss Appropriation accounts .

7. Calculation of Interest on Capital .

8. Calculation of Internet on Drawing.

9. Capital Accounts of Partners i. Fixed Capital Account . ii. Fluctuating Capital Account.

3.

10. Manager'sCommission on Net Profits. i . On profit before changing

such Commission ii . On profit after changing such Commission

11. 1. Interest on Partners loan to the firm.

2. Interest on partner’s loan from the firm.

12. Rent haid to a Partner .

13. When Appropeciation are more than profit.

14. Adjustments In the closing Accounts.

15. Rectification of Interest on capitalless Charged or Cancellation of

excessive interest.

16. In the absence of Partnerships Deed.

17. Guarantee of profit to a Partner.

4.

INTRODUCTION

There arecertain limitations of a sole trader. In a sole trading

concern only one man invests capital, undertakes the risk

involved in the business and controls the whole affairs of the

business.

Therefore, some persons may combine and enter into an

agreement to form a partnership. Partnership is a relation of

mutual trust and faith. Partnership accounts should present a

true and fair picture of the partnership business.

5.

1. Nature ofPartnership Firm

a partnership firm is not a separate legal entity. In other

words, it has no existence separate from its partners.

It means that in case of bankruptcy of the partnership

firm, private estates of the partners would be liable to

meet the firm's debts.

6.

Definition of Partnership

Section 4 of the Indian partnership act, 1932

Partnership is the relation between persons

who have agreed to share the profits of a

business carried on by all or any of them acting

for all."

7.

2. Main Featuresor Essential Elements or Characteristics

of Partnership

1. Two or more persons :- There must be atleast two persons to form a

partnership.

Partnership Act does not specify the maximum number of persons.

Section 464 of Indian Companies Act, 2013, restricts the number of

partners to 50.

2. Agreement :- Partnership is the result of an agreement. It must come

into existence by an agreement and not by the operation of law.

Hindu undivided family comes into existence by the operation of law

and not by an agreement.

Such an agreement can be either oral or in writing.

8.

3. Existence ofBusiness and Profit Motive :- Partnership can be

formed for the purpose of carrying on some business with the

intention of earning profits .

such business must be legal.

A joint ownership of some property by itself cannot be called a

partnership

4. Sharing of Profits :- The agreement between the partners must be

aimed at sharing the profits of the business.

If some persons join hands to run some charitable activity, it will

not be called partnership.

9.

5. Relationship ofPrincipal and Agent : Each partner is an agent as

well as a principal of the firm.

An agent, because he can bind the other partners by his acts and

a principal, because he himself can be bound by the acts of the

other partners.

6. Business carried on by all or any of them acting for all :-- It

means that each partner can participate in the conduct of business.

each partner is bound by the acts of other partners in respect to

the business of the firm.

7. No Separate Existence :- A partnership firm has no separate

existence from its members.

It means that all agreements entered with the firm will be

enforceable against each partner separately and jointly.

10.

3. i. Rightsof a Partner

1. Every partner has the right to share profits or losses with other

partners in the agreed ratio.

2. Every partner has the right to take part in the conduct of the

business.

3. Every partner has the right to be consulted in the matters related

to partnership business.

4. Every partner has the right to inspect and have a copy of the

books of accounts.

5. Every partner has a right to disallow the admission of a new

partner.

6. Every partner is the joint owner of the partnership property.

11.

1. Law:- Applicable Indian Partnership

Act, 1932.

2. Registration :- Optional

3. Creation:- Created by an Agreement

4. Separate Legal Entity :- It is not a

separate legal entity.

5. Number of Partner :-Minimum 2 and

Maximum 50.

6. Ownership of assets :- Firm cannot

own any asset.The partners own the

assets of the firm.

7. Liability Unlimited

Limited Liability PartnershipAct,

2008

Compulsory with Registrar of

Companies

Created by Law

It is a separate legal entity.

Minimum 2 but no maximum limit.

The LLP as an independent entity

can own assets.

Limited to the extent of their

contribution towards LLP

Distinction between Partnership

Firm and LLP

PARTNERSHIP LLPs

12.

4. Meaning ofPARTNERSHIP DEED

As stated above a partnership is formed by an

agreement.

This agreement can be oral or written.

Though the law does not expressly require that

there should be an agreement in writing but the

absence of written agreement may be the

source of problem in managing the affairs of

the partnership firm

13.

Contents of Partnershipdeed

• 1. Name and address of the firm.

• 2. Name and addresses of all the partners.

• 3. Nature and place of the business.

• 4. Duration of partnership.

• 5. Date of commencement of partnership.

• 6. Amount of capital contributed by each partners.

• 7. Ratio in which profits and losses are to be shared.

14.

8. Intereston partner's capital and drawings.

9. Interest on loan by the partner to the firm.

10. Salary, Commission, etc. if any payable to a partner.

11. Method of computation and treatment of Goodwill on the

reconstitution of the firm.

12. Mode of settlement of accounts in case of retirement/death

of a partner.

13. Mode of settlement of accounts in case of dissolution of

the firm.

14. Accounting period of the firm.

15. Bank accounts operate by firm’s name or by Partner.

16. Settlement of disputes.

17. Method of recording of firm‘s accounts.

15.

5 . Rulesin the absence of the

Partnership Deed

Profit sharing ratio:- The partners will share the profits and losses in the

equal ratio.

Interest on loan:- Interest on loan will be given @ 6% p.a. to the partners.

Interest on Capital:- No interest is allowed to partners on the capital

invested by them.

Interest on Drawing:- No interest is to be charged on Drawing.

Salary to a Partner:- No Partner is entitled to any salary or Commission.

Admission of new Partner:- without agreed by all Partner no new Partner

admitted.

16.

Meaning of Profitand Loss Appropriation

Account:

Profit and Loss Appropriation Account is an extension of Profit

and Loss Account that is prepared to distribute the net profit

among the partners.

All adjustments relating to partners like interest on capital,

interest on drawings, commission to partners etc. are made in

this Account

17.

10. Manager'sCommission on Net Profits.

i . On profit before changing such Commission.

ii . On profit after changing such Commission

11. Interest on Partners loan to the firm.

12. Reserve account.

13. Rent haid to a Partner .

ALL POINTS IN FORMATS OF P/L APPROPRIATION

18.

Dr. Cr.

Particular amountParticular amount

To partner 's salary

*******

By Profit & loss a/c

Balancing figure ******

To partners commission (on net profit ) ******* Less :- Interest on Loan ***

To reserve a/c ******* Less:- Rent received by Partner **

To Interest on capital ******* Less:- Manager‘s commission *** ****

To Provisions for donation *******

By Interest on drawing

To profit transfer to: *******

X's capital Account *******

Y's capital Accoun *******

6. PROFIT & LOSS APPROPRIATION

ACCOUNT for the year ended 31st

March, 2021

19.

Enter for Intereston Capital

1 on allowing interest on Capital

a Interest on Capital A/c Dr.

To Partner's Capital A/c

(Interest on Capital at .....% p.a)

b on closer of interest on Capital A/c

Profit & Loss Appropriation A/c Dr.

To interest on Capital A/c

2 Entry for interest on Drawing

on allowing interest on Drawing

a Partner's Capital A/c Dr.

To Interest on Drawing A/c

(Interest on Capital at .....% p.a)

b on closer of interest on Drawing A/c

JOURNAL ENTRIES FOR P/L APP. ACCOUNT

20.

3 EntRY forsalary and Commission payable

a on allowing salary or Commission to Partner

Partner's Salary or Commission A/c Dr.

To Partner's Capital A/c

b on closer of salary or Commission A/c

Profit and Loss Appropriation A/c Dr.

To Partner's Salary /Commission A/c

4 Entry for transfer a part of profit to Reserve

Profit and Loss Appropriation A/c Dr.

To Reserve A/c

5 Entry for transfer of credit balance of P/L App.

Profit and Loss Appropriation A/c Dr.

To Partner's Capital or current A/c

21.

profit and lossappropriation A/c

In case of net Loss

1. If Partners will get any Rent for his property.

P/L AIC :- To Rent of Partner (Dr)

2. If partner grant Loan to the firm (interest on loan) 6% given.

P/ L A/c :- To Interest on Loan (Dr.)

Note :- Rent and interest on loan are charged against profit. It will be

allowed even in case of Loss.

In case of (Net profit)

i. Rent Received by partner

P/L A/c :- To Rent of partner

ii. Interest on Loan Received by partner

P/L A/L :- To Interest on Loan.

Note, when interest on capital , salary of Partner is more than given profit

then profit will be adjusted in the Ratio of Interest on loan and Salary.

22.

Loan given TOTHE FIRM by partner

PROFIT/LOSS ACCOUNT

PARTICULAR Dr. AMOUNT PARTICULAR AMOUNT

To Interest on partner’s loan a/c

PARTICULAR Dr. AMOUNT PARTICULAR AMOUNT

To Balance C/d

By Bank A/C

BY Interest on Loan A/C

Partner’s Loan A/C

23.

Loan taken bypartner FROM THE FIRM

Profit and Loss A/c

PARTICULAR Dr. AMOUNT PARTICULAR. Cr. AMOUNT

By Interest on partner’s loan a/c

PARTICULAR Dr. AMOUNT PARTICULAR AMOUNT

To Interest on partner’s Loan A/C

Partner’s capital A/c

24.

7. Provision relatingto Interest on Capital

Case Provision

case 1. when Agreement is silent No interest is allowed

about Interest on Capital

case 2. Interest on Capital is silent in

Interest will be allowed when there is a

profit

treating interest as charge a. In case of Loss No interest will be allowed

b. Profit is equal to or full interest will be allowed

more than the amount of interest

c. profit is less than the interest itself Interest will be restricted

to the amount of profit .

Hence, profit will be distributed

in the ratio of interest on Capital.

case 3. Interest is treated as charge

Full interest will be allowed whether

there is profit or Loss

25.

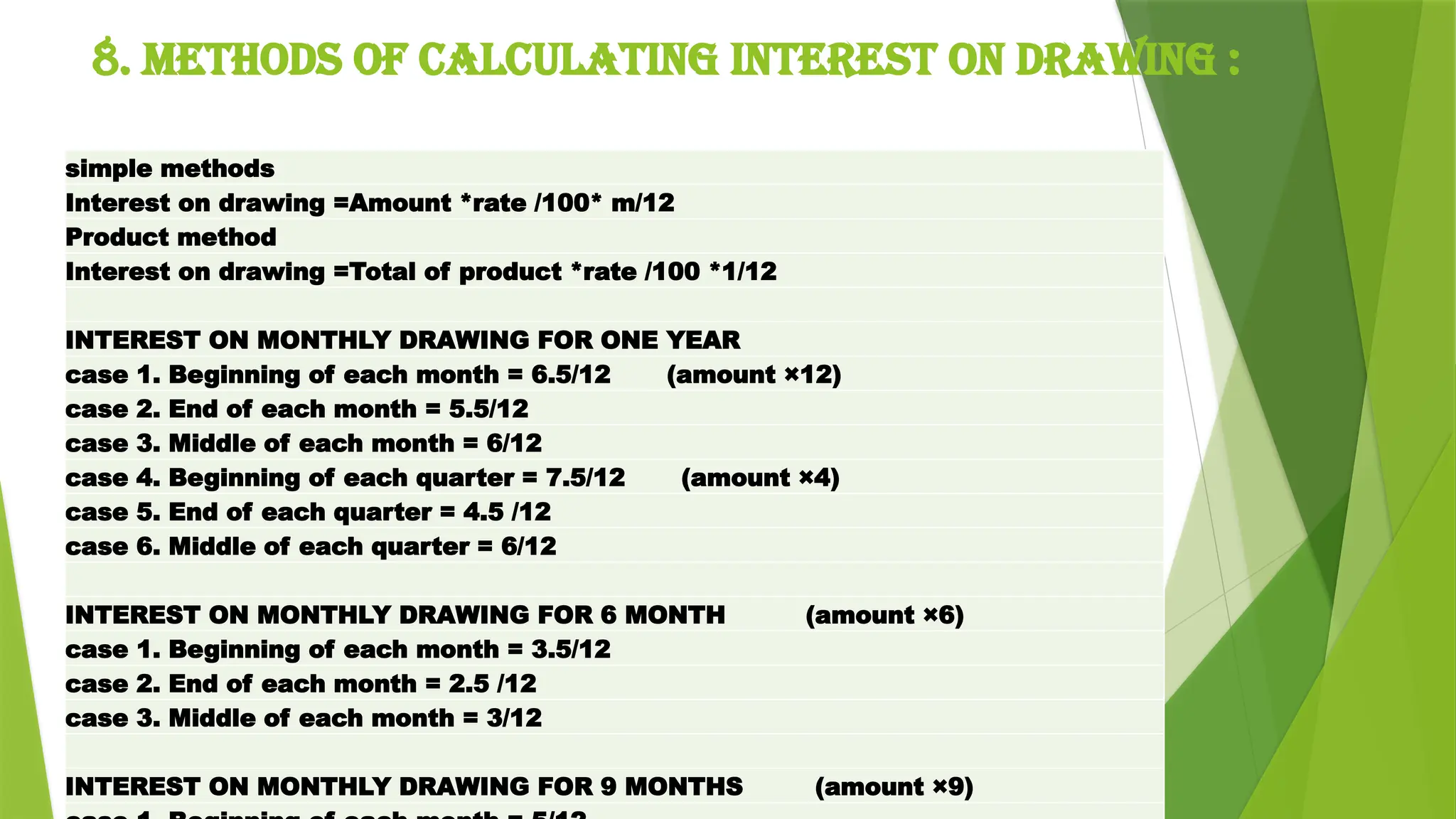

8. METHODS OFCALCULATING INTEREST ON DRAWING :

simple methods

Interest on drawing =Amount *rate /100* m/12

Product method

Interest on drawing =Total of product *rate /100 *1/12

INTEREST ON MONTHLY DRAWING FOR ONE YEAR

case 1. Beginning of each month = 6.5/12 (amount ×12)

case 2. End of each month = 5.5/12

case 3. Middle of each month = 6/12

case 4. Beginning of each quarter = 7.5/12 (amount ×4)

case 5. End of each quarter = 4.5 /12

case 6. Middle of each quarter = 6/12

INTEREST ON MONTHLY DRAWING FOR 6 MONTH (amount ×6)

case 1. Beginning of each month = 3.5/12

case 2. End of each month = 2.5 /12

case 3. Middle of each month = 3/12

INTEREST ON MONTHLY DRAWING FOR 9 MONTHS (amount ×9)

26.

9. CAPITAL ACCOUNTSOF PARTNERS

In case of partnership there is a separate

capital account for each partner.

The capital contributed by each partner will be

conducted to his capital account.

Capital account of partners may be maintained

in any one of the following two method.

1. FIXED CAPITAL ACCOUNTS

2. FLUCTUATING CAPITAL ACCOUNTS

27.

Capital ofpartners are not allowed to change

during the lifetime of business except in

extraordinary circumstances .

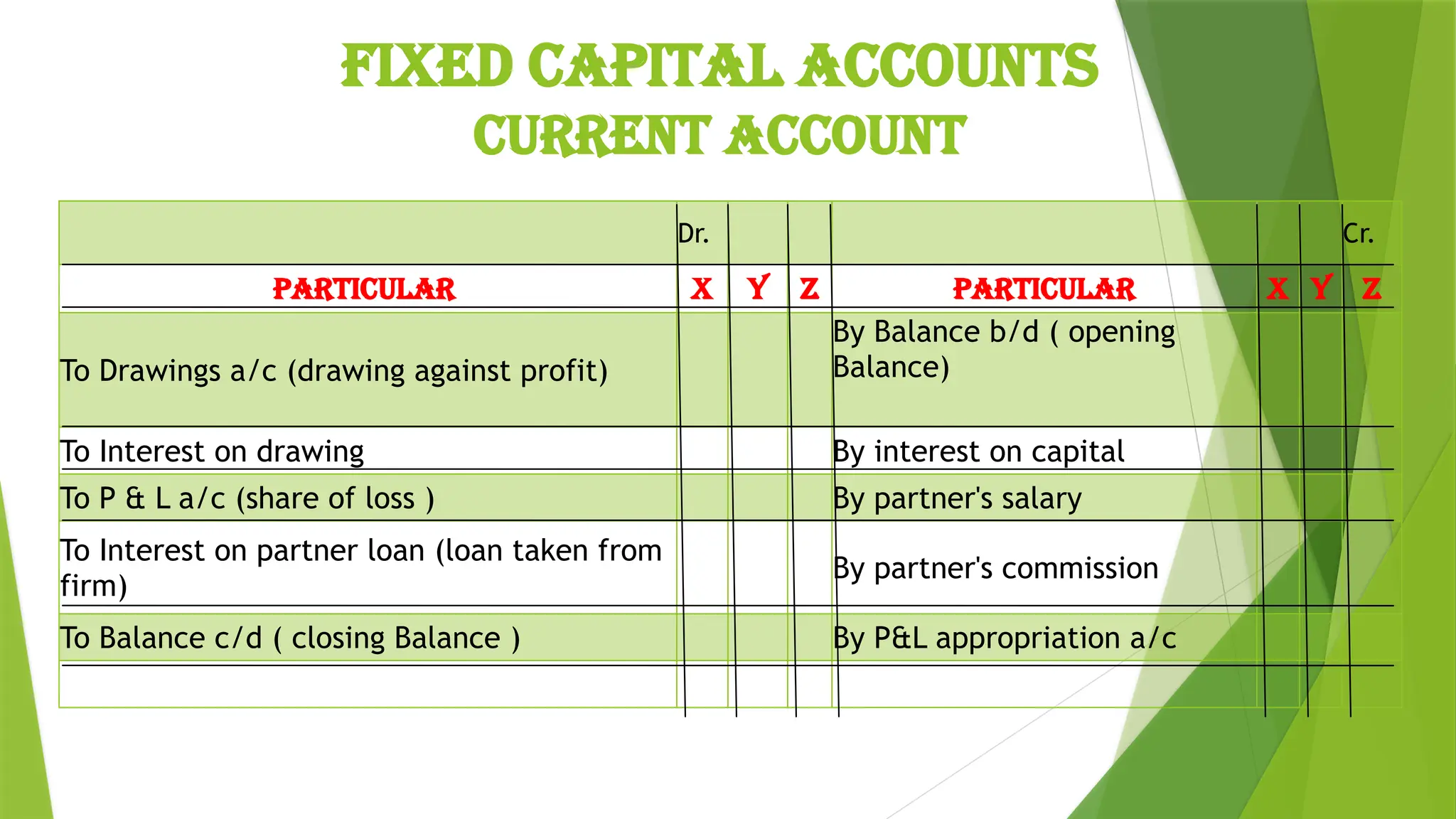

when fixed capital method is adopted, all

entries related to drawing, interest on capital,

interest on drawing, salary to partner, share of

profit or loss etc., are made in newly opened

account for each partner called current account

or drawing account .

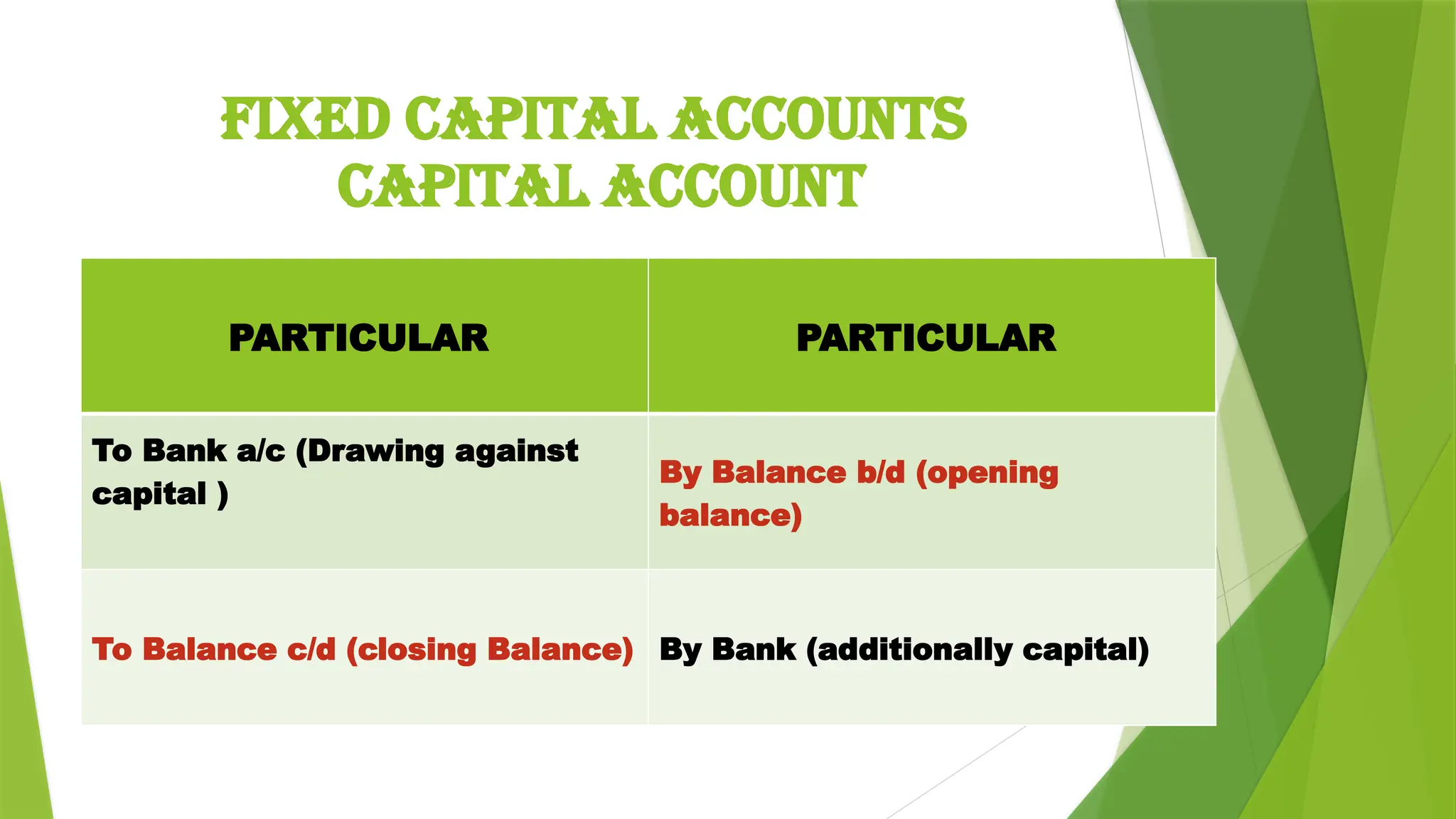

Fixed Capital Accounts

28.

PARTICULAR PARTICULAR

To Banka/c (Drawing against

capital )

By Balance b/d (opening

balance)

To Balance c/d (closing Balance) By Bank (additionally capital)

Fixed Capital Accounts

CAPITAL ACCOUNT

29.

Fixed Capital Accounts

CURRENTACCOUNT

Dr. Cr.

Particular X Y Z Particular X Y Z

To Drawings a/c (drawing against profit)

By Balance b/d ( opening

Balance)

To Interest on drawing By interest on capital

To P & L a/c (share of loss ) By partner's salary

To Interest on partner loan (loan taken from

firm)

By partner's commission

To Balance c/d ( closing Balance ) By P&L appropriation a/c

30.

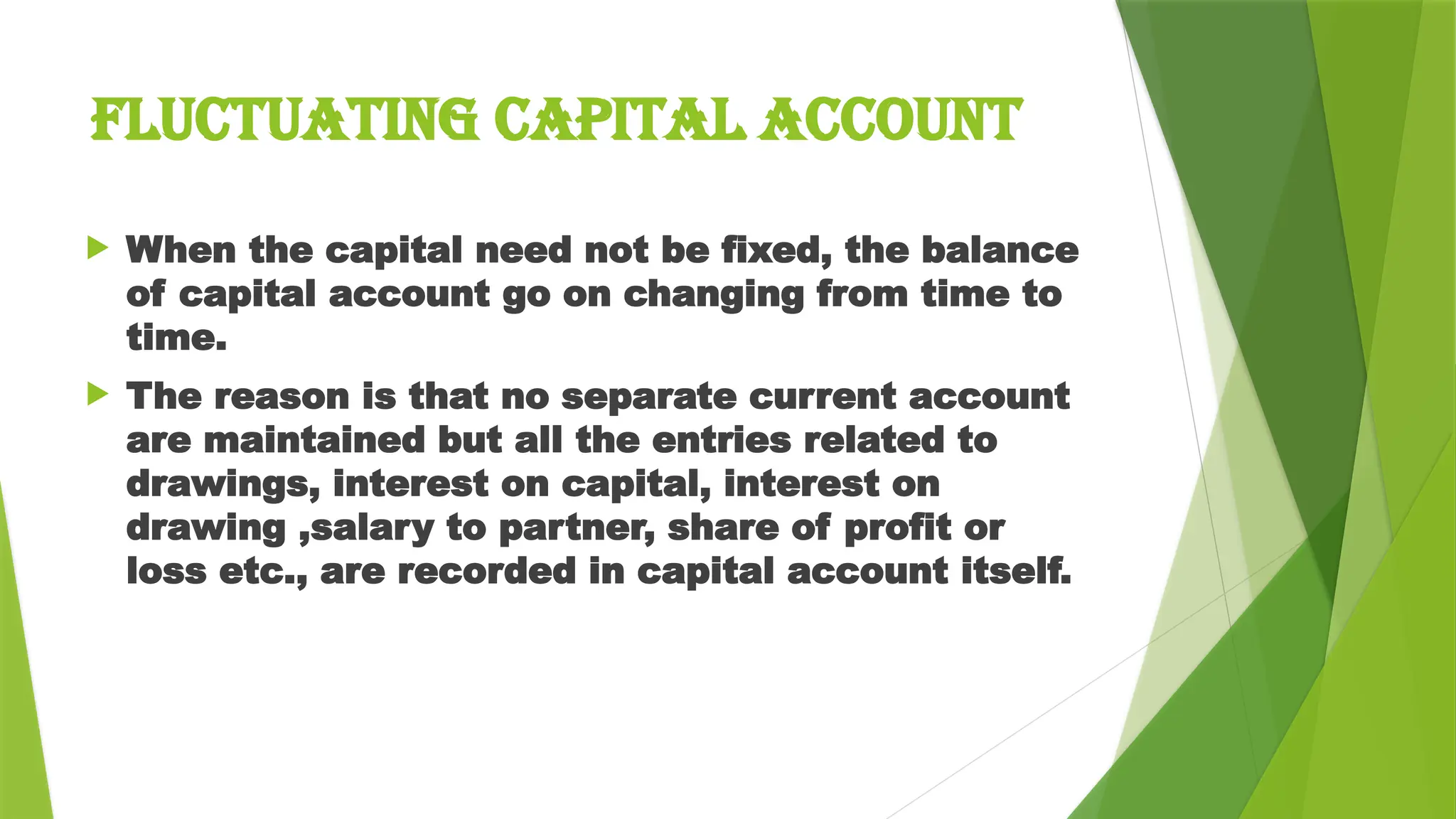

When thecapital need not be fixed, the balance

of capital account go on changing from time to

time.

The reason is that no separate current account

are maintained but all the entries related to

drawings, interest on capital, interest on

drawing ,salary to partner, share of profit or

loss etc., are recorded in capital account itself.

FLUCTUATING CAPITAL ACCOUNT

31.

FLUCTUATING CAPITAL ACCOUNT

PARTNERSCAPITAL A/C

Dr. Cr.

Particular X Y Z Particular X Y Z

To Bank a/c (Drawing against capital )

By Balance c/d ( opening

Balance)

To Drawings a/c (drawing against profit)

By Bank (additionally

capital)

To Interest on drawing By interest on capital

To P & L a/c (share of loss ) By partner's salary

To Interest on partner loan (loan taken

from firm)

By partner's commission

To Balance c/d ( closing Balance ) By P&L appropriation a/c

32.

Question 1

Partner APartner B

1 A and B commenced business with capital respectively. rs 6,00,000 rs 2,00,000

2 the profit during the year . rs 2,40,000

3 Interest on capital is to be allowed on capital . 6 % p.m 6 % p.m

4 partner are allowed to Salary of rupees . rs 700/Month rs 60,000 p.a

5 the drawing of the partner . rs 60,000 rs 40,000

6 the Interest on drawing rs 2,000

rs 1,000 or 5%

p.a

7 Partnership sharing profit and loss in the ratio of 2 : 1

8

Partner's Commission 8% of net profit before charging any commission

(profit * 8/100) (see question 9)

9

Partner's commission of 8% of net profit after charging any commission

(profit * 8/108)

10 manager is entitled to a commission of 10% of the profit

11 Interest on partner's loan a/c of rs 80,000 for the whole year .

12 1/10th of the distributable profit transferred to General Reserve.

13

partner is entitled to a Rent of rs 20,000 per month for the use of his

premises by the firm.

6 or 14

Interest on drawing (drawing for beginning,middle,end of each month or

quarter and for 6 months or 9 months .

3 or 15 Interest on Capital in the absence of partnership Deed. (follow the rules )

16 prepare the Profit and Loss appropriation account and

17 partners capital account as at 31st March 2021

33.

Dr. Cr.

Particular amountParticular amount

To partner 's salary By Profit & loss a/c (net profit)

Less:- Rent 13

To partners commission (on net

profit ) 8,9

Less:- Interest on partner's loan

11

To General reserve a/c 12 Less :- Manager's Commission 10

To Interest on capital 3 or 15 (10% of Net profit)

A's Capital A/c

B's Capital A/c

To Provisions for donation

To profit transfer to: By Interest on drawing (6 or 14)

A's capital Account Partner's Capital A/c

B's capital Accoun Partner's Capital A/c

PROFIT & LOSS APPROPRIATION ACCOUNT

for the year ended 31st March, 2017

34.

PRATNERS CAPITAL ACCOUNT

Dr.Cr.

Particular A B Particular A B

To Bank a/c

(Drawing against capital )

By Balance c/d

(opening Balance)

To Drawings a/c

(drawing against profit)

By Bank

(additionally capital)

To Interest on drawing By interest on capital

To P & L a/c (share of loss ) By partner's salary

To Balance c/d ( closing Balance ) By partner's commission

By P&L appropriation a/c

35.

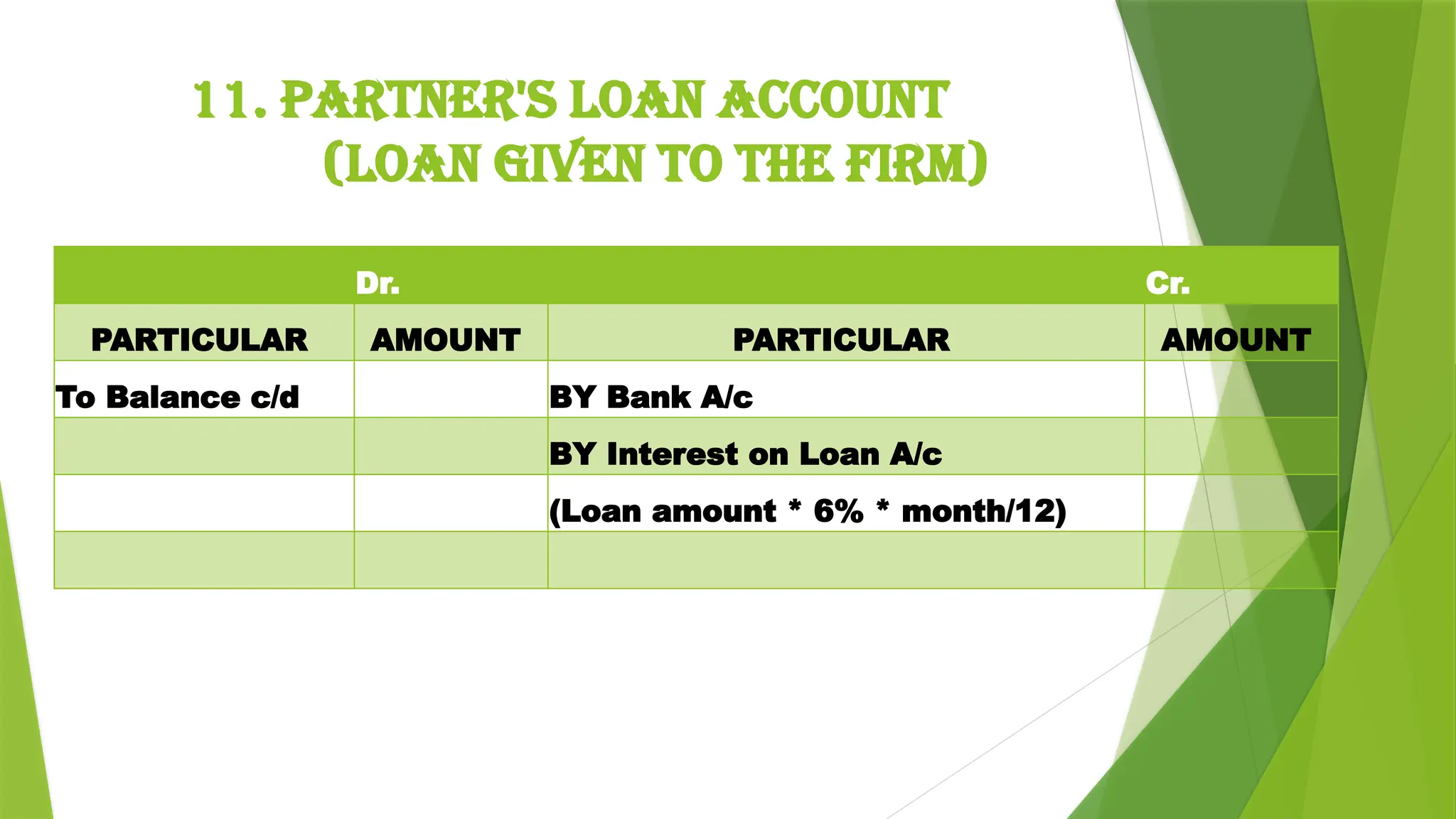

11. PARTNER'S LOANACCOUNT

(Loan given TO THE firm)

Dr. Cr.

PARTICULAR AMOUNT PARTICULAR AMOUNT

To Balance c/d BY Bank A/c

BY Interest on Loan A/c

(Loan amount * 6% * month/12)

36.

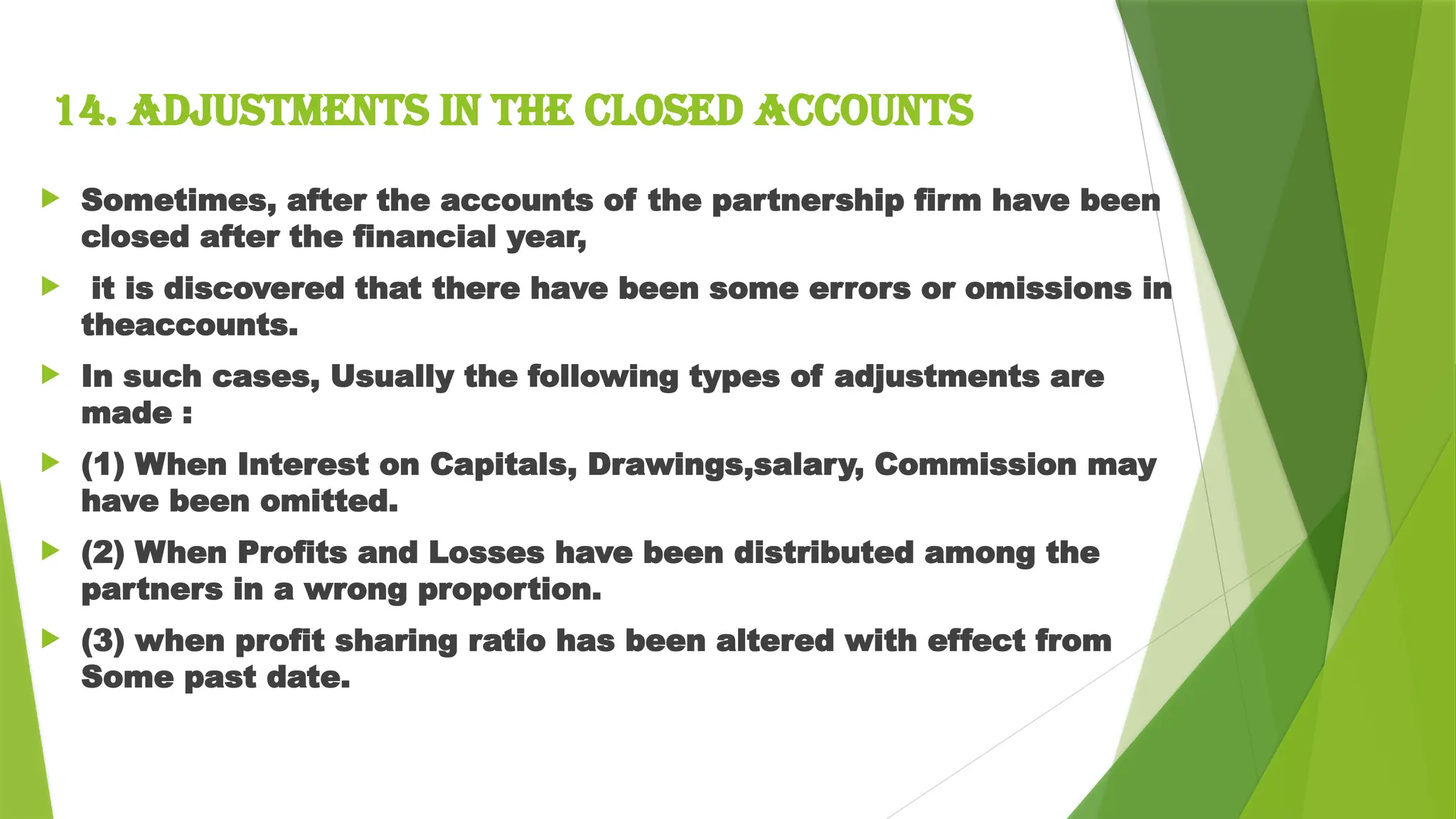

14. Adjustments inthe closed accounts

Sometimes, after the accounts of the partnership firm have been

closed after the financial year,

it is discovered that there have been some errors or omissions in

theaccounts.

In such cases, Usually the following types of adjustments are

made :

(1) When Interest on Capitals, Drawings,salary, Commission may

have been omitted.

(2) When Profits and Losses have been distributed among the

partners in a wrong proportion.

(3) when profit sharing ratio has been altered with effect from

Some past date.

37.

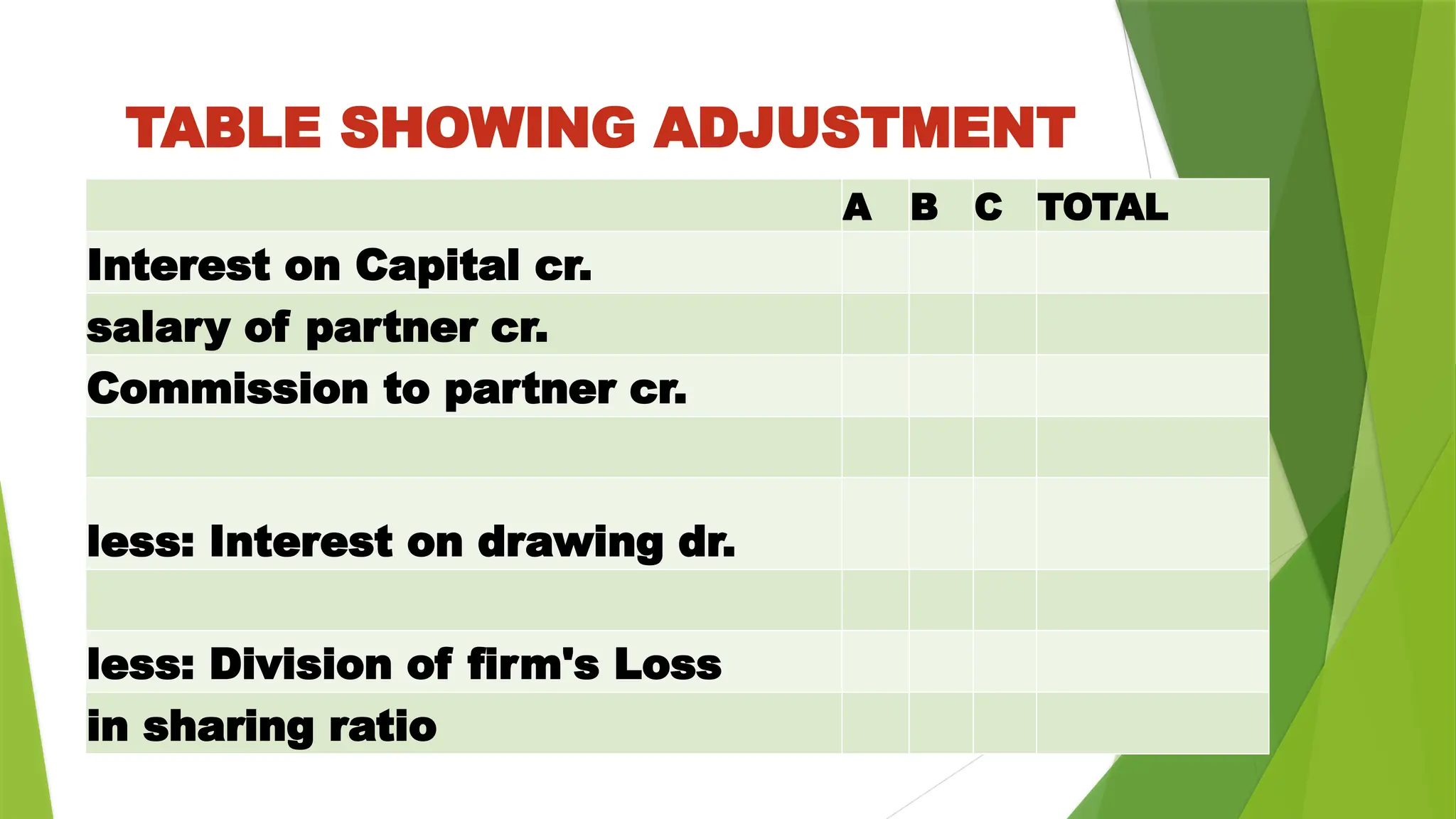

A B CTOTAL

Interest on Capital cr.

salary of partner cr.

Commission to partner cr.

less: Interest on drawing dr.

less: Division of firm's Loss

in sharing ratio

TABLE SHOWING ADJUSTMENT