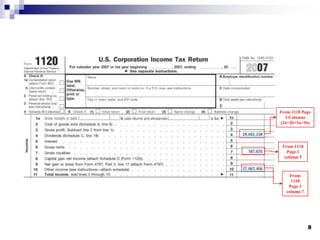

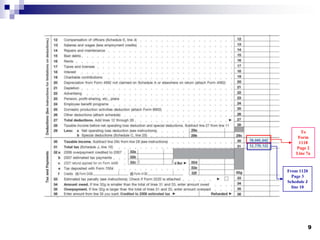

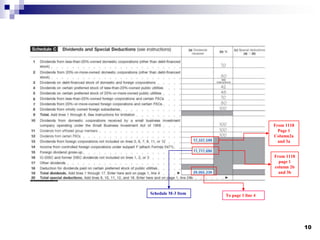

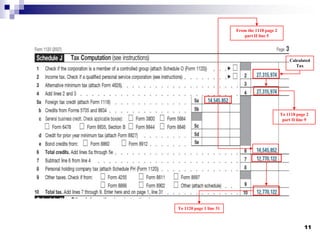

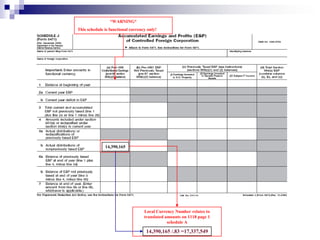

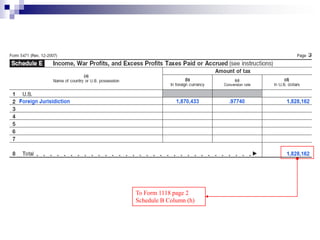

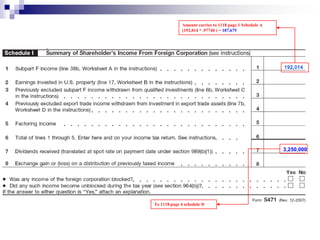

This document summarizes key compliance aspects of Forms 1118 and 5471. Form 1118 is used to claim foreign tax credits for income taxes paid abroad on income also taxed in the US. Taxpayers have 10 years to file this form. Form 5471 must be filed by US persons who are officers, directors or shareholders of certain foreign corporations to satisfy reporting requirements. It is due with the taxpayer's annual income tax return. The document reviews how various lines and amounts on the forms interconnect and need to reconcile between the forms and the taxpayer's US tax return. It stresses the importance of ensuring dividends, other income items and tax liability amounts reconcile between foreign and US reporting.