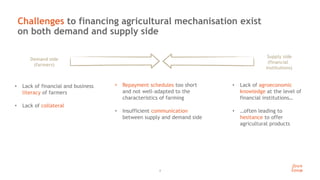

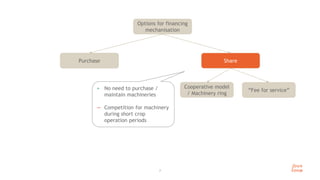

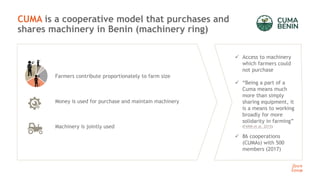

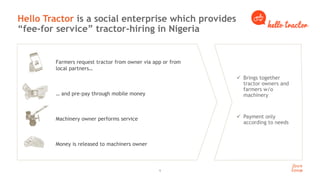

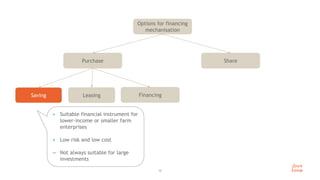

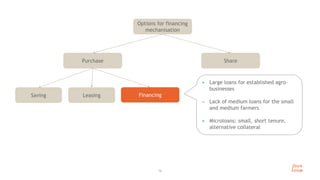

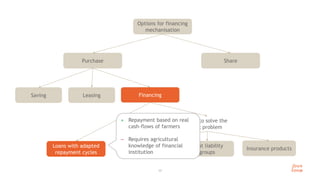

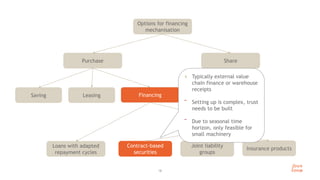

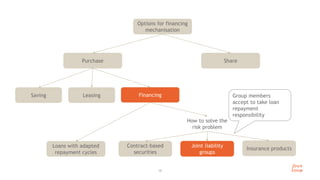

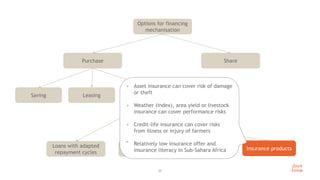

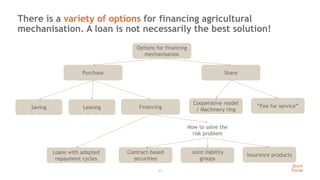

This document discusses options for financing agricultural mechanization in Sub-Saharan Africa. It notes that mechanization can be financed through various means, including purchasing equipment, leasing, saving programs, and fee-for-service models. It also discusses how to address challenges like lack of farmer financial literacy, short repayment periods, and risk through mechanisms like insurance programs, groups with shared liability, and loans with repayment schedules tailored to agricultural cycles. The document advocates combining perspectives from the agricultural and financial sectors to develop customized financing solutions.