Download to read offline

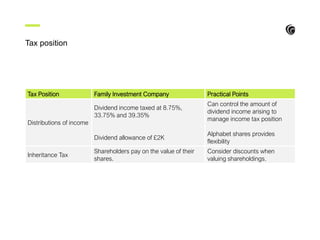

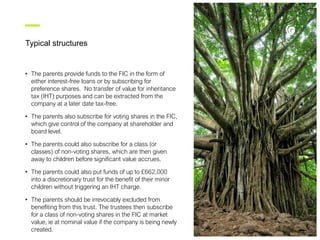

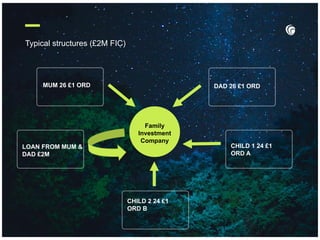

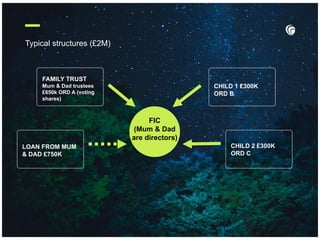

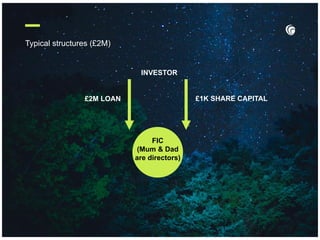

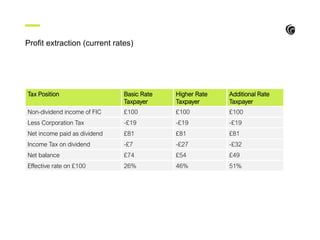

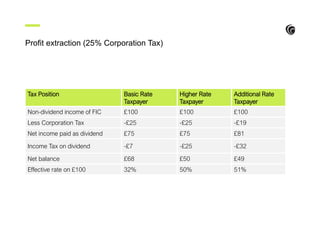

The document discusses Family Investment Companies (FICs), which are private companies used as an alternative to family trusts. Key features of FICs include shareholders being family members and enabling parents to retain control over assets in a tax efficient manner. Typical structures involve parents providing funds through interest-free loans or preference shares and retaining voting shares. FICs allow profits to accumulate and be distributed to family members in a tax efficient way. However, future changes to taxation of retained profits could impact the benefits of FICs. Planning is needed to ensure FICs continue to provide estate planning benefits for families.