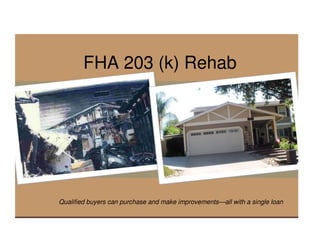

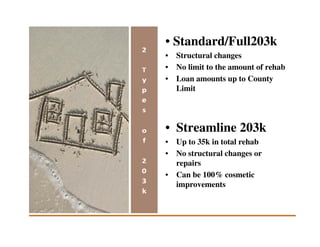

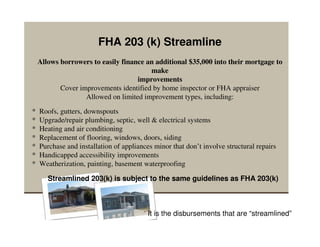

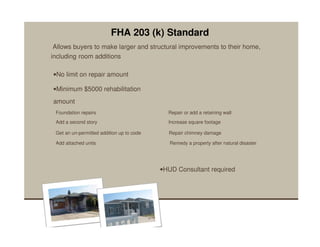

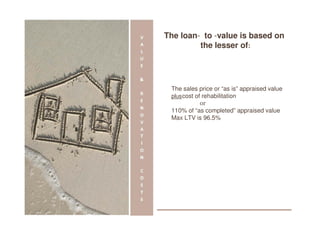

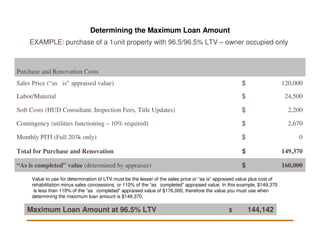

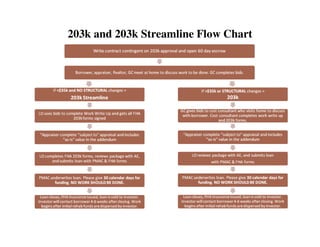

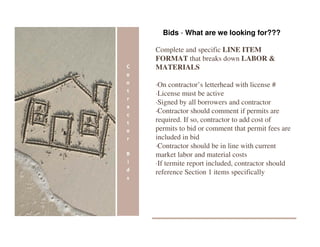

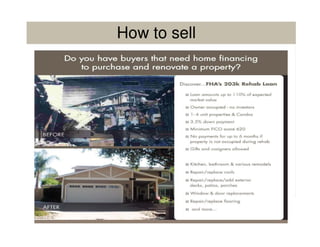

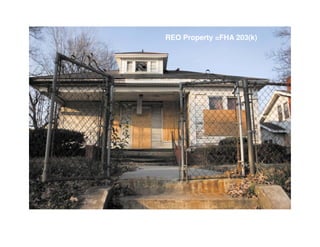

The document summarizes the FHA 203(k) mortgage program, which allows home buyers to finance both the purchase and renovation/repair costs of a home in a single loan. It describes how buyers can purchase distressed properties and make necessary improvements to expand homeownership opportunities. The program offers affordable financing options for buyers looking to purchase homes needing repairs or existing homeowners financing renovations. It provides guidelines on borrower eligibility, financing terms including loan-to-value ratios, rehabilitation amounts and costs that can be included, and the renovation process including contractor requirements and fund disbursements.

![FHA Streamline 203[k] Wholesale](https://cdn.slidesharecdn.com/ss_thumbnails/fhastreamline203k122711-120116101337-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![FHA Streamline 203[k] Residential](https://cdn.slidesharecdn.com/ss_thumbnails/resfhastreamline203k011112-120116101356-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![203k Realtor Guide[1]](https://cdn.slidesharecdn.com/ss_thumbnails/203krealtorguide1-12500914865136-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)