Economic Report Of The President Us Government Printing Office

Economic Report Of The President Us Government Printing Office

Economic Report Of The President Us Government Printing Office

Economic Report Of The President Us Government Printing Office

Economic Report Of The President Us Government Printing Office

1.

Economic Report OfThe President Us Government

Printing Office download

https://ebookbell.com/product/economic-report-of-the-president-

us-government-printing-office-2296152

Explore and download more ebooks at ebookbell.com

2.

Here are somerecommended products that we believe you will be

interested in. You can click the link to download.

Economic Report Of The President 2009 Economic Report Of The President

Transmitted To The Congress Executive Office Of The President

https://ebookbell.com/product/economic-report-of-the-

president-2009-economic-report-of-the-president-transmitted-to-the-

congress-executive-office-of-the-president-2187084

Transport And Economic Development Report Of The Hundred And

Nineteenth Round Table On Transport Economics Held In Paris On 29th

And 30rd March 2001 Oecd

https://ebookbell.com/product/transport-and-economic-development-

report-of-the-hundred-and-nineteenth-round-table-on-transport-

economics-held-in-paris-on-29th-and-30rd-march-2001-oecd-6779976

Role Of Direct And Indirect Taxes In The Federal Reserve System A

Conference Report Of The Nber And The Brookings Institution National

Bureau Of Economic Research John F Due

https://ebookbell.com/product/role-of-direct-and-indirect-taxes-in-

the-federal-reserve-system-a-conference-report-of-the-nber-and-the-

brookings-institution-national-bureau-of-economic-research-john-f-

due-51957078

Report Of The Hundred And Eighteenth Round Table On Transport

Economics Held In Paris On 30th November1st December 2000 On The

Following Topic Tolls On Interurban Road Infrastructure An Economic

Evaluation Oecd

https://ebookbell.com/product/report-of-the-hundred-and-eighteenth-

round-table-on-transport-economics-held-in-paris-on-30th-november1st-

december-2000-on-the-following-topic-tolls-on-interurban-road-

infrastructure-an-economic-evaluation-oecd-6778094

3.

The Financial CrisisInquiry Report Authorized Edition Final Report Of

The National Commission On The Causes Of The Financial And Economic

Crisis In The United States 1st Edition Financial Crisis Inquiry

Commission

https://ebookbell.com/product/the-financial-crisis-inquiry-report-

authorized-edition-final-report-of-the-national-commission-on-the-

causes-of-the-financial-and-economic-crisis-in-the-united-states-1st-

edition-financial-crisis-inquiry-commission-2621534

National Systems Of Transport Infrastructure Planning Report Of The

One Hundred And Twenty Eight Round Table On Transport Econmics Held In

Paris On 26th27th February 2004 Ecmt Round Tables European Conference

Of Ministers Of Tran

https://ebookbell.com/product/national-systems-of-transport-

infrastructure-planning-report-of-the-one-hundred-and-twenty-eight-

round-table-on-transport-econmics-held-in-paris-on-26th27th-

february-2004-ecmt-round-tables-european-conference-of-ministers-of-

tran-1989116

The State Of Economic Inclusion Report 2021 The Potential To Scale 1st

Edition World Bank Colin Andrews Ins Arvalo Snchez Sarang Chaudhary

Timothy Clay Puja Vasudeva Dutta Janet Heisey Sadna Samaranayake Aude

De Montesquiou

https://ebookbell.com/product/the-state-of-economic-inclusion-

report-2021-the-potential-to-scale-1st-edition-world-bank-colin-

andrews-ins-arvalo-snchez-sarang-chaudhary-timothy-clay-puja-vasudeva-

dutta-janet-heisey-sadna-samaranayake-aude-de-montesquiou-51883058

Report On The State Of The European Union Volume 3 Crisis In The Eu

Economic Governance Jeanpaul Fitoussi

https://ebookbell.com/product/report-on-the-state-of-the-european-

union-volume-3-crisis-in-the-eu-economic-governance-jeanpaul-

fitoussi-5361956

Report On The State Of The European Union Volume 3 Crisis In The Eu

Economic Governance Jeanpaul Fitoussi

https://ebookbell.com/product/report-on-the-state-of-the-european-

union-volume-3-crisis-in-the-eu-economic-governance-jeanpaul-

fitoussi-1814682

For sale bythe Superintendent of Documents, U.S. Government Printing Office

Internet: bookstore.gpo.gov Phone: toll free (866) 512-1800; DC area (202) 512-1800

Fax: (202) 512-2104 Mail: Stop IDCC, Washington, DC 20402-0001

ISBN 978-0-16-084824-7

transmitted to the congress

february 2010

together with

the annual report

of the

council of economic advisers

united states government printing office

washington : 2010

e c o n o m i c

rep ort

of the

president

8.

iii

C O NT E N T S

ECONOMIC REPORT OF THE PRESIDENT ........................................... 1

ANNUAL REPORT OF THE COUNCIL OF ECONOMIC ADVISERS* 11

CHAPTER 1. TO RESCUE, REBALANCE, AND REBUILD .............. 25

CHAPTER 2. RESCUING THE ECONOMY FROM THE GREAT

RECESSION ........................................................................ 39

CHAPTER 3 CRISIS AND RECOVERY IN THE WORLD

ECONOMY ........................................................................ 81

CHAPTER 4. SAVING AND INVESTMENT ....................................... 113

CHAPTER 5. ADDRESSING THE LONG-RUN FISCAL

CHALLENGE ..................................................................... 137

CHAPTER 6. BUILDING A SAFER FINANCIAL SYSTEM .............. 159

CHAPTER 7. REFORMING HEALTH CARE ...................................... 181

CHAPTER 8. STRENGTHENING THE AMERICAN LABOR

FORCE ................................................................................. 213

CHAPTER 9. TRANSFORMING THE ENERGY SECTOR AND

ADDRESSING CLIMATE CHANGE ............................ 235

CHAPTER 10. FOSTERING PRODUCTIVITY GROWTH

THROUGH INNOVATION AND TRADE ................. 259

REFERENCES ............................................................................................... 285

APPENDIX A. REPORT TO THE PRESIDENT ON THE

ACTIVITIES OF THE COUNCIL OF

ECONOMIC ADVISERS DURING 2009 ...................... 305

APPENDIX B. STATISTICAL TABLES RELATING TO INCOME,

EMPLOYMENT, AND PRODUCTION ....................... 319

____________

*For a detailed table of contents of the Council’s Report, see page 15.

Page

Economic Report ofthe President | 3

economic report of the president

To the Congress of the United States:

As we begin a new year, the American people are still experiencing

the effects of a recession as deep and painful as any we have known in

generations. Traveling across this country, I have met countless men and

women who have lost jobs these past two years. I have met small business

owners struggling to pay for health care for their workers; seniors unable

to afford prescriptions; parents worried about paying the bills and saving

for their children’s future and their own retirement. And the effects of this

recession come in the aftermath of a decade of declining economic security

for the middle class and those who aspire to it.

At the same time, over the past two years, we have also seen reason

for hope: the resilience of the American people who have held fast—

even in the face of hardship—to an unrelenting faith in the promise of

our country.

It is that determination that has helped the American people

overcome difficult periods in our Nation’s history. And it is this persever-

ance that remains our great strength today. After all, our workers are as

productive as ever. American businesses are still leaders in innovation.

Our potential is still unrivaled. Our task as a Nation—and our mission

as an Administration—is to harness that innovative spirit, that productive

energy, and that potential in order to create jobs, raise incomes, and foster

economic growth that is sustained and broadly shared. It’s not enough

to move the economy from recession to recovery. We must rebuild the

economy on a new and stronger foundation.

I can report that over the past year, this work has begun. In the

coming year, this work continues. But to understand where we must go

in the next year and beyond, it is important to remember where we began

one year ago.

11.

4 | EconomicReport of the President

Last January, years of irresponsible risk-taking and debt-fueled

speculation—unchecked by sound oversight—led to the near-collapse

of our financial system. We were losing an average of 700,000 jobs each

month. Over the course of one year, $13 trillion of Americans’ household

wealth had evaporated as stocks, pensions, and home values plummeted.

Our gross domestic product was falling at the fastest rate in a quarter

century. The flow of credit, vital to the functioning of businesses large and

small, had ground to a halt. The fear among economists, from across the

political spectrum, was that we could sink into a second Great Depression.

Immediately, we took a series of difficult steps to prevent that

catastrophe for American families and businesses. We acted to get lending

flowing again so ordinary Americans could get financing to buy homes

and cars, to go to college, and to start businesses of their own; and so

businesses, large and small, could access loans to make payroll, buy equip-

ment, hire workers, and expand. We enacted measures to stem the tide of

foreclosures in our housing market, helping responsible homeowners stay

in their homes and helping to stop the broader decline in home values.

To achieve this, and to prevent an economic collapse, we were forced

to use authority enacted under the previous Administration to extend

assistance to some of the very banks and financial institutions whose

actions had helped precipitate the turmoil. We also took steps to prevent

the collapse of the American auto industry, which faced a crisis partly

of its own making, to prevent another round of widespread job losses in

an already fragile time. These decisions were not popular, but they were

necessary. Indeed, the decision to stabilize the financial system helped to

avert a larger catastrophe, and thanks to the efficient management of the

rescue—with added transparency and accountability—we have recovered

most of the money provided to banks.

In addition, even as we worked to address the crises in our banking

sector, in our housing market, and in our auto industry, we also began

attacking our economic crisis on a broader front. Less than one month

after taking office, we enacted the most sweeping economic recovery

package in history: the American Recovery and Reinvestment Act of

2009. The Recovery Act not only provided tax cuts to small businesses and

95 percent of working families and provided emergency relief to those out

of work or without health insurance; it also began to lay a new foundation

for long-term growth. With investments in health care, education, infra-

structure, and clean energy, the Recovery Act has saved or created roughly

two million jobs so far, and it has begun the hard work of transforming our

economy to thrive in the modern, global era.

12.

Economic Report ofthe President | 5

Because of these and other steps, we can safely say that we’ve avoided

the depression many feared. Our economy is growing again, and the

growth over the last three months was the strongest in six years. But while

economic growth is important, it means nothing to somebody who has

lost a job and can’t find another. For Americans looking for work, a good

job is the only good news that matters. And that’s why our work is far

from complete.

It is true that the steps we have taken have slowed the flood of job

losses from 691,000 per month in the first quarter of 2009 to 69,000 in the

last quarter. But stemming the tide of job loss isn’t enough. More than

7 million jobs have been lost since the recession began two years ago. This

represents not only a terrible human tragedy, but also a very deep hole

from which we’ll have to climb out. Until jobs are being created to replace

those we’ve lost—until America is back at work—my Administration will

not rest and this recovery will not be finished.

That’s why I am continuing to call on the Congress to pass a jobs bill.

I’ve proposed a package that includes tax relief for small businesses to spur

hiring, that accelerates construction on roads, bridges, and waterways,

and that creates incentives for homeowners to invest in energy efficiency,

because this will create jobs, save families money, and reduce pollution

that harms our environment.

It is also essential that as we promote private sector hiring, we

continue to take steps to prevent layoffs of critical public servants like

teachers, firefighters, and police officers, whose jobs are threatened by

State and local budget shortfalls. To do otherwise would not only worsen

unemployment and hamper our recovery; it would also undermine our

communities. And we cannot forget the millions of people who have lost

their jobs. The Recovery Act provided support for these families hardest-

hit by this recession, and that support must continue.

At the same time, long before this crisis hit, middle-class families

were under growing strain. For decades, Washington failed to address

fundamental weaknesses in the economy: rising health care costs, growing

dependence on foreign oil, an education system unable to prepare all of

our children for the jobs of the future. In recent years, spending bills and

tax cuts for the very wealthiest were approved without paying for any of

it, leaving behind a mountain of debt. And while Wall Street gambled

without regard for the consequences, Washington looked the other way.

As a result, the economy may have been working for some at the

very top, but it was not working for all American families. Year after year,

folks were forced to work longer hours, spend more time away from their

13.

6 | EconomicReport of the President

loved ones, all while their incomes flat-lined and their sense of economic

security evaporated. Growth in our country was neither sustained nor

broadly shared. Instead of a prosperity powered by smart ideas and sound

investments, growth was fueled in large part by a rapid rise in consumer

borrowing and consumer spending.

Beneath the statistics are the stories of hardship I’ve heard all

across America—hardships that began long before this recession hit two

years ago. For too many, there has long been a sense that the American

dream—a chance to make your own way, to work hard and support your

family, save for college and retirement, own a home—was slipping away.

And this sense of anxiety has been combined with a deep frustration that

Washington either didn’t notice, or didn’t care enough to act.

These weaknesses have not only made our economy more

susceptible to the kind of crisis we have been through. They have also

meant that even in good times the economy did not produce nearly enough

gains for middle-class families. Typical American families saw their stan-

dards of living stagnate, rather than rise as they had for generations. That

is why, in the aftermath of this crisis, and after years of inaction, what is

clear is that we cannot go back to business as usual.

That is why, as we strive to meet the crisis of the moment, we are

continuing to lay a new foundation for prosperity: a foundation on which

the middle class can prosper and grow, where if you are willing to work

hard, you can find a good job, afford a home, send your children to world-

class schools, afford high-quality health care, and enjoy retirement security

in your later years. This is the heart of the American Dream, and it is at

the core of our efforts to not only rebuild this economy—but to rebuild it

stronger than before. And this work has already begun.

Already, we have made historic strides to reform and improve our

education system. We have launched a Race to the Top in which schools

are competing to create the most innovative programs, especially in math

and science. We have already made college more affordable, even as we

seek to increase student aid by ending a wasteful subsidy that serves only

to line the pockets of lenders with tens of billions of taxpayer dollars. And

I’ve proposed a new American Graduation Initiative and set this goal: by

2020, America will once again have the highest proportion of college grad-

uates in the world. For we know that in this new century, growth will be

powered not by what consumers can borrow and spend, but what talented,

skilled workers can create and export.

Already, we have made historic strides to improve our health care

system, essential to our economic prosperity. The burdens this system

14.

Economic Report ofthe President | 7

places on workers, businesses, and governments is simply unsustainable.

And beyond the economic cost—which is vast—there is also a terrible

human toll. That’s why we’ve extended health insurance to millions more

children; invested in health information technology through the Recovery

Act to improve care and reduce costly errors; and provided the largest

boost to medical research in our history. And I continue to fight to pass

real, meaningful health insurance reforms that will get costs under control

for families, businesses, and governments, protect people from the worst

practices of insurance companies, and make coverage more affordable and

secure for people with insurance, as well as those without it.

Already, we have begun to build a new clean energy economy. The

Recovery Act included the largest investment in clean energy in history,

investments that are today creating jobs across America in the industries

that will power our future: developing wind energy, solar technology, and

clean energy vehicles. But this work has only just begun. Other countries

around the world understand that the nation that leads the clean energy

economy will be the nation that leads the global economy. I want America

to be that nation. That is why we are working toward legislation that will

create new incentives to finally make renewable energy the profitable

kind of energy in America. It’s not only essential for our planet and our

security, it’s essential for our economy.

But this is not all we must do. For growth to be truly sustainable—

for our prosperity to be truly shared and our living standards to actually

rise—we need to move beyond an economy that is fueled by budget deficits

and consumer demand. In other words, in order to create jobs and raise

incomes for the middle class over the long run, we need to export more

and borrow less from around the world, and we need to save more money

and take on less debt here at home. As we rebuild, we must also rebalance.

In order to achieve this, we’ll need to grow this economy by growing our

capacity to innovate in burgeoning industries, while putting a stop to irre-

sponsible budget policies and financial dealings that have led us into such

a deep fiscal and economic hole.

That begins with policies that will promote innovation throughout

our economy. To spur the discoveries that will power new jobs, new busi-

nesses—and perhaps new industries—I have challenged both the public

sector and the private sector to devote more resources to research and

development. And to achieve this, my budget puts us on a path to double

investment in key research agencies and makes the research and experi-

mentation tax credit permanent. We are also pursuing policies that will

help us export more of our goods around the world, especially by small

15.

8 | EconomicReport of the President

businesses and farmers. And by harnessing the growth potential of inter-

national trade—while ensuring that other countries play by the rules and

that all Americans share in the benefits—we will support millions of good,

high-paying jobs.

But hand in hand with increasing our reliance on the Nation’s

ingenuity is decreasing our reliance on the Nation’s credit card, as well as

reining in the excess and abuse in our financial sector that led large firms

to take on extraordinary risks and extraordinary liabilities.

When my Administration took office, the surpluses our Nation

had enjoyed at the start of the last decade had disappeared as a result of

the failure to pay for two large tax cuts, two wars, and a new entitlement

program. And decades of neglect of rising health care costs had put our

budget on an unsustainable path.

In the long term, we cannot have sustainable and durable economic

growth without getting our fiscal house in order. That is why even as we

increased our short-term deficit to rescue the economy, we have refused

to go along with business as usual, taking responsibility for every dollar we

spend. Last year, we combed the budget, cutting waste and excess wher-

ever we could, a process that will continue in the coming years. We are

pursuing health insurance reforms that are essential to reining in deficits.

I’ve called for a fee to be paid by the largest financial firms so that the

American people are fully repaid for bailing out the financial sector. And

I’ve proposed a freeze on nonsecurity discretionary spending for three

years, a bipartisan commission to address the long-term structural imbal-

ance between expenditures and revenues, and the enactment of “pay-go”

rules so that Congress has to account for every dollar it spends.

In addition, I’ve proposed a set of common sense reforms to prevent

future financial crises. For while the financial system is far stronger today

than it was one year ago, it is still operating under the same rules that led

to its near-collapse. These are rules that allowed firms to act contrary to

the interests of customers; to hide their exposure to debt through complex

financial dealings that few understood; to benefit from taxpayer-insured

deposits while making speculative investments to increase their own

profits; and to take on risks so vast that they posed a threat to the entire

economy and the jobs of tens of millions of Americans.

That is why we are seeking reforms to empower consumers with

the benefit of a new consumer watchdog charged with making sure that

financial information is clear and transparent; to close loopholes that

allowed big financial firms to trade risky financial products like credit

defaults swaps and other derivatives without any oversight; to identify

16.

Economic Report ofthe President | 9

system-wide risks that could cause a financial meltdown; to strengthen

capital and liquidity requirements to make the system more stable; and to

ensure that the failure of any large firm does not take the economy down

with it. Never again will the American taxpayer be held hostage by a bank

that is “too big to fail.”

Through these reforms, we seek not to undermine our markets but

to make them stronger: to promote a vibrant, fair, and transparent finan-

cial system that is far more resistant to the reckless, irresponsible activities

that might lead to another meltdown. And these kinds of reforms are in

the shared interest of firms on Wall Street and families on Main Street.

These have been a very tough two years. American families and

businesses have paid a heavy price for failures of responsibility from Wall

Street to Washington. Our task now is to move beyond these failures, to

take responsibility for our future once more. That is how we will create

new jobs in new industries, harnessing the incredible generative and

creative capacity of our people. That is how we’ll achieve greater economic

security and opportunity for middle-class families in this country. That

is how in this new century we will rebuild our economy stronger than

ever before.

the white house

february 2010

13

letter of transmittal

Councilof Economic Advisers

Washington, D.C., February 11, 2010

Mr. President:

The Council of Economic Advisers herewith submits its 2010

Annual Report in accordance of the Employment Act of 1946 as amended

by the Full Employment and Balanced Growth Act of 1978.

Sincerely,

Christina D. Romer

Chair

Austan Goolsbee

Member

Cecilia Elena Rouse

Member

19.

15

C O NT E N T S

CHAPTER 1. TO RESCUE, REBALANCE, AND REBUILD ......... 25

Rescuing an Economy in Freefall ............................................ 26

Rescuing the Economy from the Great Recession ........................ 28

Crisis and Recovery in the World Economy ................................ 29

Rebalancing the Economy on the Path to Full

Employment ...................................................................................... 29

Saving and Investment .................................................................. 29

Addressing the Long-Run Fiscal Challenge ................................. 31

Building a Safer Financial System ............................................... 32

Rebuilding a Stronger Economy .............................................. 33

Reforming Health Care ................................................................. 33

Strengthening the American Labor Force .................................... 35

Transforming the Energy Sector and Addressing Climate

Change ............................................................................................ 36

Fostering Productivity Growth Through Innovation and

Trade .............................................................................................. 37

Conclusion ........................................................................................ 38

CHAPTER 2. RESCUING THE ECONOMY FROM THE

GREAT RECESSION ................................................................................ 39

An Economy in Freefall ............................................................... 39

The Run-Up to the Recession ........................................................ 40

The Downturn ............................................................................... 41

Wall Street and Main Street ......................................................... 44

The Unprecedented Policy Response ...................................... 46

Monetary Policy ............................................................................. 47

Financial Rescue ............................................................................ 49

Fiscal Stimulus ............................................................................... 51

Housing Policy ............................................................................... 55

The Effects of the Policies ........................................................ 56

Page

20.

16 | AnnualReport of the Council of Economic Advisers

The Financial Sector ...................................................................... 57

Housing ........................................................................................... 60

Overall Economic Activity ............................................................. 63

The Labor Market .......................................................................... 68

The Challenges Ahead .................................................................. 72

Deteriorating Forecasts .................................................................. 72

The Administration Forecast ......................................................... 75

Responsible Policies to Spur Job Creation ..................................... 78

Conclusion ......................................................................................... 79

CHAPTER 3. CRISIS AND RECOVERY IN THE WORLD

ECONOMY ................................................................................................. 81

International Dimensions of the Crisis ................................ 82

Spread of the Financial Shock ....................................................... 82

The Collapse of World Trade ........................................................ 87

The Collapse in Financial Flows ................................................... 89

The Decline in Output Around the Globe .................................... 90

Policy Responses Around the Globe ........................................ 93

Monetary Policy in the Crisis ........................................................ 93

Central Bank Liquidity Swaps ....................................................... 96

Fiscal Policy in the Crisis ............................................................... 98

Trade Policy in the Crisis ............................................................... 100

The Role of International Institutions ................................ 100

The G-20 ......................................................................................... 100

The International Monetary Fund ................................................ 101

The Beginning of Recovery Around the Globe ................... 102

The Impact of Fiscal Policy ............................................................ 104

The World Economy in the Near Term ........................................ 106

Global Imbalances in the Crisis ..................................................... 108

Conclusion ......................................................................................... 111

CHAPTER 4. SAVING AND INVESTMENT ..................................... 113

The Path of Consumption Spending ...................................... 114

The Determinants of Saving .......................................................... 115

Implications for Recent and Future Saving Behavior .................. 117

The Future of the Housing Market and

Construction .................................................................................... 120

The Housing Market ...................................................................... 121

21.

Contents | 17

CommercialReal Estate ................................................................. 123

Business Investment ....................................................................... 126

Investment in the Recovery ............................................................ 126

Investment in the Long Run .......................................................... 127

The Current Account ................................................................... 129

Determinants of the Current Account .......................................... 129

The Current Account in the Recovery and in the Long Run ....... 132

Steps to Encourage Exports ............................................................ 133

Conclusion ......................................................................................... 135

CHAPTER 5. ADDRESSING THE LONG-RUN FISCAL

CHALLENGE .............................................................................................. 137

The Long-Run Fiscal Challenge ............................................... 137

Sources of the Long-Run Fiscal Challenge .................................... 139

The Role of the Recovery Act and Other Rescue Operations ....... 143

An Anchor for Fiscal Policy ...................................................... 144

The Effects of Budget Deficits ........................................................ 145

Feasible Long-Run Fiscal Policies .................................................. 146

The Choice of a Fiscal Anchor ....................................................... 148

Reaching the Fiscal Target ........................................................ 149

General Principles .......................................................................... 149

Comprehensive Health Care Reform ............................................ 150

Restoring Balance to the Tax Code ............................................... 151

Eliminating Wasteful Spending ..................................................... 155

Conclusion: The Distance Still to Go ................................... 156

CHAPTER 6. BUILDING A SAFER FINANCIAL SYSTEM ........... 159

What Is Financial Intermediation? ......................................... 160

The Economics of Financial Intermediation ................................ 160

Types of Financial Intermediaries ................................................. 163

The Regulation of Financial Intermediation in the

United States .................................................................................... 166

Financial Crises: The Collapse of Financial

Intermediation ................................................................................. 170

Confidence Contagion .................................................................... 170

Counterparty Contagion ................................................................ 172

Coordination Contagion ................................................................ 173

Preventing Future Crises: Regulatory Reform ................. 174

22.

18 | AnnualReport of the Council of Economic Advisers

Promote Robust Supervision and Regulation of Financial

Firms ............................................................................................... 175

Establish Comprehensive Regulation of Financial Markets ........ 176

Provide the Government with the Tools It Needs to Manage

Financial Crises .............................................................................. 178

Raise International Regulatory Standards and Improve

International Cooperation ............................................................. 179

Protect Consumers and Investors from Financial Abuse ............ 179

Conclusion ......................................................................................... 180

CHAPTER 7. REFORMING HEALTH CARE .................................... 181

The Current State of the U.S. Health Care Sector ......... 182

Rising Health Spending in the United States ................................ 182

Market Failures in the Current U.S. Health Care System:

Theoretical Background ................................................................. 185

System-Wide Evidence of Inefficient Spending ............................ 188

Declining Coverage and Strains on Particular Groups and

Sectors .............................................................................................. 191

Health Policies Enacted in 2009 ............................................... 196

Expansion of the CHIP Program ................................................... 197

Subsidized COBRA Coverage ........................................................ 197

Temporary Federal Medical Assistance Percentage (FMAP)

Increase ........................................................................................... 199

Recovery Act Measures to Improve the Quality and Efficiency

of Health Care ................................................................................ 201

2009 Health Reform Legislation ............................................... 202

Insurance Market Reforms: Strengthening and Securing

Coverage .......................................................................................... 202

Expansions in Health Insurance Coverage Through the

Exchange ......................................................................................... 205

Economic and Health Benefits of Expanding Health

Insurance Coverage ........................................................................ 206

Reducing the Growth Rate of Health Care Costs in the Public

and Private Sectors ......................................................................... 207

The Economic Benefits of Slowing the Growth Rate of Health

Care Costs ....................................................................................... 210

Conclusion ......................................................................................... 211

23.

Contents | 19

CHAPTER8. STRENGTHENING THE AMERICAN

LABOR FORCE .......................................................................................... 213

Challenges Facing American Workers .................................. 214

Unemployment ............................................................................... 214

Sectoral Change .............................................................................. 216

Stagnating Incomes for Middle-Class Families ............................ 217

Policies to Support Workers ...................................................... 219

Education and Training: The Groundwork for

Long-Term Prosperity ................................................................... 221

Benefits of Education ..................................................................... 221

Trends in U.S. Educational Attainment ....................................... 222

U.S. Student Achievement ............................................................. 226

A Path Toward Improved Educational Performance ...... 227

Postsecondary Education ............................................................... 228

Training and Adult Education ...................................................... 229

Elementary and Secondary Education .......................................... 231

Early Childhood Education ........................................................... 233

Conclusion ......................................................................................... 234

CHAPTER 9. TRANSFORMING THE ENERGY SECTOR

AND ADDRESSING CLIMATE CHANGE .......................................... 235

Greenhouse Gas Emissions, Climate, and Economic

Well-Being ......................................................................................... 236

Greenhouse Gases ........................................................................... 237

Temperature Change ...................................................................... 238

Impact on Economic Well-Being ................................................... 239

Jump-Starting the Transition to Clean Energy ................. 243

Recovery Act Investments in Clean Energy .................................. 243

Short-Run Macroeconomic Effects of the Clean Energy

Investments ..................................................................................... 246

Other Domestic Actions to Mitigate Climate

Change ................................................................................................. 247

Market-Based Approaches to Advance the Clean

Energy Transformation and Address Climate Change ... 248

Cap-and-Trade Program Basics .................................................... 248

Ways to Contain Costs in an Effective Cap-and-Trade

System .............................................................................................. 250

24.

20 | AnnualReport of the Council of Economic Advisers

Coverage of Gases and Industries .................................................. 253

The American Clean Energy and Security Act ............................. 254

International Action on Climate Change Is Needed ....... 255

Partnerships with Major Developed and Emerging

Economies ....................................................................................... 256

Phasing Out Fossil Fuel Subsidies ................................................. 257

Conclusion ......................................................................................... 257

CHAPTER 10. FOSTERING PRODUCTIVITY GROWTH

THROUGH INNOVATION AND TRADE ......................................... 259

The Role of Productivity Growth in Driving Living

Standards ........................................................................................... 261

Recent Trends in Productivity in the United States ..................... 262

Sources of Productivity Growth ..................................................... 264

Fostering Productivity Growth Through Innovation ... 266

The Importance of Basic Research ................................................ 267

Private Research and Experimentation ........................................ 269

Protection of Intellectual Property Rights ..................................... 270

Spurring Progress in National Priority Areas .............................. 272

Increasing Openness and Transparency ....................................... 272

Trade as an Engine of Productivity Growth and

Higher Living Standards ............................................................. 274

The United States and International Trade ................................. 275

Sources of Productivity Growth from International Trade ......... 276

Encouraging Trade and Enforcing Trade Agreements ................ 280

Ensuring the Gains from Productivity Growth

Are Widely Shared ......................................................................... 282

Conclusion ......................................................................................... 284

REFERENCES ............................................................................................. 285

appendixes

A. Report to the President on the Activities of the Council of

Economic Advisers During 2009 .................................................. 305

B. Statistical Tables Relating to Income, Employment, and

Production ...................................................................................... 319

25.

Contents | 21

listof figures

1-1. House Prices Adjusted for Inflation ............................................. 27

1-2. Monthly Change in Payroll Employment .................................... 28

1-3. Personal Consumption Expenditures as a Share of GDP .......... 30

1-4. Actual and Projected Budget Surpluses in January 2009

under Previous Policy ..................................................................... 31

1-5. Real Median Family Income .......................................................... 33

1-6. Total Compensation Including and Excluding Health

Insurance ........................................................................................... 34

1-7. Mean Years of Schooling by Birth Cohort ................................... 36

1-8. R&D Spending as a Percent of GDP ............................................. 37

2-1. House Prices Adjusted for Inflation ............................................. 40

2-2. Income and Consumption Around the 2008 Tax Rebate ......... 42

2-3. TED Spread and Moody’s BAA-AAA Spread Through

December 2008 ................................................................................. 43

2-4. Assets on the Federal Reserve’s Balance Sheet ............................ 48

2-5. TED Spread and Moody’s BAA-AAA Spread Through

December 2009 ................................................................................. 57

2-6. S&P 500 Stock Price Index ............................................................. 58

2-7. Monthly Gross SBA 7(a) and 504 Loan Approvals .................... 60

2-8. 30-Year Fixed Rate Mortgage Rate ............................................... 61

2-9. FHFA and LoanPerformance National House Price Indexes ... 63

2-10. Real GDP Growth ............................................................................ 64

2-11. Real GDP: Actual and Statistical Baseline Projection ............... 65

2-12. Contributions to Real GDP Growth ............................................. 66

2-13. Average Monthly Change in Employment .................................. 68

2-14. Estimated Effect of the Recovery Act on Employment .............. 69

2-15. Contributions to the Change in Employment ............................. 71

2-16. Okun’s Law, 2000-2009 ................................................................... 74

3-1. Interbank Market Rates .................................................................. 83

3-2. Nominal Trade-Weighted Dollar Index ....................................... 85

3-3. OECD Exports-to-GDP Ratio ....................................................... 87

3-4. Vertical Specialization and the Collapse in Trade ...................... 88

3-5. Cross-Border Gross Purchases and Sales of Long-Term

Assets ................................................................................................. 90

3-6. Industrial Production in Advanced Economies .......................... 91

3-7. Industrial Production in Emerging Economies .......................... 92

3-8. Headline Inflation, 12-Month Change ......................................... 93

3-9. Policy Rates in Economies with Major Central Banks ............... 94

26.

22 | AnnualReport of the Council of Economic Advisers

3-10. Change in Central Bank Assets ..................................................... 95

3-11. Central Bank Liquidity Swaps of the Federal Reserve ................ 97

3-12. Tax Share and Discretionary Stimulus ......................................... 99

3-13. Outperforming Expectations and Stimulus ................................. 105

3-14. OECD Countries: GDP and Unemployment ............................. 108

3-15. Current Account Deficits or Surpluses ........................................ 110

4-1. Personal Consumption Expenditures as a Share of GDP .......... 114

4-2. Personal Saving Rate Versus Wealth Ratio .................................. 115

4-3. Personal Saving Rate: Actual Versus Model ............................... 118

4-4. Actual Personal Saving Versus Counterfactual Personal

Saving ................................................................................................. 119

4-5. Single-Family Housing Starts ......................................................... 121

4-6. Homeownership Rate ...................................................................... 122

4-7. Fixed Investment in Structures by Type ...................................... 124

4-8. Commercial Real Estate Prices and Loan Delinquencies .......... 125

4-9. Nonstructures Investment as a Share of Nominal GDP ............ 128

4-10. Saving, Investment, and the Current Account as a Percent

of GDP ............................................................................................... 132

4-11. Growth of U.S. Exports and Rest-of-World Income:

1960-2008 .......................................................................................... 134

5-1. Actual and Projected Budget Surpluses in January 2009

under Previous Policy ..................................................................... 138

5-2. Actual and Projected Government Debt Held by the Public

under Previous Policy ..................................................................... 139

5-3. Budgetary Cost of Previous Administration Policy ................... 141

5-4. Causes of Rising Spending on Medicare, Medicaid, and

Social Security .................................................................................. 142

5-5. Budget Comparison: January 2001 and January 2009 .............. 143

5-6. Effect of the Recovery Act on the Deficit ..................................... 144

5-7. Top Statutory Tax Rates ................................................................. 153

5-8. Evolution of Average Tax Rates .................................................... 154

6-1. Financial Intermediation: Saving into Investment .................... 161

6-2. Financial Sector Assets .................................................................... 163

6-3. Share of Financial Sector Assets by Type ..................................... 164

6-4. Confidence Contagion .................................................................... 171

6-5. Counterparty Contagion ................................................................ 173

6-6. Coordination Contagion ................................................................ 174

7-1. National Health Expenditures as a Share of GDP ...................... 183

7-2. Total Compensation Including and Excluding Health

Insurance ........................................................................................... 184

27.

Contents | 23

7-3.Child and Infant Mortality Across G-7 Countries ..................... 190

7-4. Insurance Rates of Non-Elderly Adults ........................................ 192

7-5. Percent of Americans Uninsured by Age ..................................... 193

7-6. Share of Non-Elderly Individuals Uninsured by Poverty

Status .................................................................................................. 194

7-7. Medicare Part D Out-of-Pocket Costs by Total Prescription

Drug Spending ................................................................................. 195

7-8. Share Uninsured among Adults Aged 18 and Over ................... 198

7-9. Monthly Medicaid Enrollment Across the States ....................... 200

8-1. Unemployment and Underemployment Rates ........................... 214

8-2. Unemployment Rates by Race ....................................................... 215

8-3. Real Median Family Income and Median Individual

Earnings ............................................................................................ 218

8-4. Share of Pre-Tax Income Going to the Top 10 Percent of

Families ............................................................................................. 219

8-5. Total Wage and Salary Income by Educational Group ............. 222

8-6. Mean Years of Schooling by Birth Cohort ................................... 224

8-7. Educational Attainment by Birth Cohort, 2007 .......................... 225

8-8. Long-Term Trend Math Performance ......................................... 227

9-1. Projected Global Carbon Dioxide Concentrations with No

Additional Action ............................................................................ 238

9-2. Recovery Act Clean Energy Appropriations by Category ......... 246

9-3. United States, China, and World Carbon Dioxide

Emissions .......................................................................................... 255

10-1. Non-Farm Labor Productivity and Per Capita Income ............. 261

10-2. Labor Productivity Growth since 1947 ........................................ 262

10-3. R&D Spending as a Percent of GDP ............................................. 270

10-4. Exports as a Share of GDP ............................................................. 275

10-5. Intra-Industry Trade, U.S. Manufacturing .................................. 278

list of tables

2-1. Cyclically Sensitive Elements of Labor Market Adjustment ..... 70

2-2. Forecast and Actual Macroeconomic Outcomes ........................ 73

2-3. Administration Economic Forecast .............................................. 75

3-1. 2009 Fiscal Stimulus as Share of GDP, G-20 Members ............. 98

3-2. Stimulus and Growth in Advanced G-20 Countries .................. 104

5-1. Government Debt-to-GDP Ratio in Selected OECD

Countries (percent) ......................................................................... 147

28.

24 | AnnualReport of the Council of Economic Advisers

list of boxes

2-1. Potential Real GDP Growth ........................................................... 76

4-1. Unemployment and the Current Account ................................... 130

7-1. The Impact of Health Reform on State and Local

Governments .................................................................................... 208

8-1. The Recession’s Impact on the Education System ...................... 224

8-2. Community Colleges: A Crucial Component of Our

Higher Education System ............................................................... 230

9-1. Climate Change in the United States and Potential Impacts .... 240

9-2. Expected Consumption Loss Associated with Temperature

Increase .............................................................................................. 241

9-3. The European Union’s Experience with Emissions Trading .... 252

10-1. Overview of the Administration’s Innovation Agenda .............. 266

29.

25

C H AP T E R 1

TO RESCUE, REBALANCE,

AND REBUILD

President Obama took office at a time of economic crisis. The recession

that began in December 2007 had accelerated following the financial

crisis in September 2008. By January 2009, 11.9 million people were unem-

ployed and real gross domestic product (GDP) was falling at a breakneck

pace. The possibility of a second Great Depression was frighteningly real.

In the first months of the Administration, the President and Congress

took unprecedented actions to restore demand, stabilize financial markets,

and put people back to work. Just 28 days after his inauguration, the

President signed the American Recovery and Reinvestment Act of 2009, the

boldest countercyclical fiscal stimulus in American history. The Financial

Stability Plan, announced in February, included wide-ranging measures to

strengthen the banking system, increase consumer and business lending,

and stem foreclosures and support the housing market. These and a host of

other actions stabilized the financial system, supported those most directly

affected by the recession, and walked the economy back from the brink.

But the Administration always knew that stabilizing the economy

would not be enough. The problems that led to the crisis were years in the

making. Continued action will be necessary to return the economy to full

employment. In the process, an important rebalancing will need to occur.

For too many years, America’s growth and prosperity were fed by a boom in

consumer spending stemming from rising asset prices and easy credit. The

Federal Government had likewise been living beyond its means, resulting in

large and growing budget deficits. And our regulatory system had failed to

keep up with financial innovation, allowing risky practices to endanger the

system and the economy. For this reason, the Administration has sought to

help restore the economy to health on a foundation of greater investment,

fiscal responsibility, and a well-functioning and secure financial system.

30.

26 | Chapter1

Even this important rebalancing would not be sufficient. In addition

to the problems that had set the stage for the crisis, long-term challenges had

been ignored and the U.S. economy was failing at some of its central tasks.

Our health care system was beset by steadily rising costs, and millions of

Americans either had no health insurance at all or were unsure whether their

coverage would be there when they needed it. Middle-class families had seen

their real incomes stagnate during the previous eight years, while those at

the top of the income distribution had seen their incomes soar. A failure to

slow the consumption of fossil fuels had contributed to global warming and

continued dependence on foreign oil. And a country built on its record of

innovation was failing to invest enough in research and development.

The President has dedicated his Administration to dealing with these

long-run problems as well. As the new decade opens, Congress has come

closer than ever before to passing landmark legislation reforming the health

insurance system. This legislation would make health insurance more secure

for those who have it and affordable for those who do not, and it would slow

the growth rate of health care costs. Over the past year, the Administration

has also worked with Congress to make important new investments to

sustain and improve K-12 education and community colleges, jump-start the

transition to a clean energy economy, and spur innovation through increased

research and development. These and numerous other initiatives will help

to rebuild the American economy stronger than before and put us on the

path to sustained growth and prosperity. Enacting these policies will help

to ensure that our children and grandchildren inherit a country as full of

promise and as economically secure as ever in our history.

Rescuing an Economy in Freefall

In December 2007, the American economy entered what at first

seemed likely to be a mild recession. As Figure 1-1 shows, real house prices

(that is, house prices adjusted for inflation) had risen to unprecedented levels,

almost doubling between 1997 and 2006. The rapid run-up in prices was

accompanied by a residential construction boom and the proliferation of

complex mortgages and mortgage-related financial assets. The fall of national

house prices starting in early 2007, and the associated declines in the values

of mortgage-backed and other related assets, led to a slowdown in the growth

of consumer spending, increases in mortgage defaults and home foreclosures,

significant strains on financial institutions, and reduced credit availability.

31.

To Rescue, Rebalance,and Rebuild | 27

By early 2008, the economy was contracting. Employment fell by

an average of 137,000 jobs per month over the first eight months of 2008.

Real GDP rose only anemically from the third quarter of 2007 to the second

quarter of 2008.

Then in September 2008, the character of the downturn worsened

dramatically. The collapse of Lehman Brothers and the near-collapse of

American International Group (AIG) led to a seizing up of financial markets

and plummeting consumer and business confidence. Parts of the financial

system froze, and assets once assumed to be completely safe, such as money-

market mutual funds, became unstable and subject to runs. Credit spreads,

a common indicator of credit market stress, spiked to unprecedented levels

in the fall of 2008. The value of the stock market plunged 24 percent in

September and October, and another 15 percent by the end of January. As

Figure 1-2 shows, over the final four months of 2008 and the first month of

2009, the economy lost, on average, a staggering 544,000 jobs per month, the

highest level of job loss since the demobilization at the end of World War

II. Real GDP fell at an increasingly rapid pace: an annual rate of 2.7 percent

in the third quarter of 2008, 5.4 percent in the fourth quarter of 2008, and

6.4 percent in the first quarter of 2009.

50

75

100

125

150

175

200

1909 1919 1929 1939 1949 1959 1969 1979 1989 1999 2009

Figure 1-1

House Prices Adjusted for Inflation

Index (1900=100)

Sources: Shiller (2005); recent data from http://www.econ.yale.edu/~shiller/data/Fig2-1.xls.

32.

28 | Chapter1

Rescuing the Economy from the Great Recession

Thus, the first imperative of the new Administration upon taking

office had to be to turn around an economy in freefall. Chapter 2 describes

the unprecedented policy actions the Administration has taken, together

with Congress and the Federal Reserve, to address the immediate crisis. The

large fiscal stimulus in the American Recovery and Reinvestment Act, the

programs to stabilize financial markets and restart lending, and the policies

to assist small businesses and distressed homeowners have all played a role

in generating one of the sharpest economic turnarounds in post–World War

II history. Real GDP is growing again, job loss has moderated greatly, house

prices appear to have stabilized, and credit spreads have almost returned

to normal levels. A wide range of evidence indicates that in the absence of

the aggressive policy actions, the recession and the attendant suffering of

ordinary Americans would have been far more severe and could have led

to catastrophe.

Yet, because the economy’s downward momentum was so great and

the barriers to robust growth from the weakened financial conditions of

households and financial institutions are so strong, the economy remains

distressed and many families continue to struggle. A change from freefall to

growing GDP and moderating job losses is a dramatic improvement, but it

is not nearly enough. Chapter 2 therefore also examines the challenges that

-800

-600

-400

-200

0

200

400

Figure 1-2

Monthly Change in Payroll Employment

Thousands, seasonally adjusted

Dec-2007

Sep-2008

Jan-2009

2005 2006 2007 2008 2009

Source: Department of Labor (Bureau of Labor Statistics), Current Employment Statistics

survey Series CES0000000001.

33.

To Rescue, Rebalance,and Rebuild | 29

remain in achieving a full recovery. It discusses some possible additional

measures to spur private sector job creation.

Crisis and Recovery in the World Economy

In the early fall of 2008, there was hope that the impact of the crisis

on the rest of the world would be limited. Those hopes were dashed during

the months that followed. In the fourth quarter of 2008 and the first quarter

of 2009, real GDP fell sharply—often at double-digit rates—in the United

Kingdom, Germany, Japan, Taiwan, and elsewhere. The surprisingly rapid

spread of the downturn to the rest of the world reduced the demand for U.S.

exports sharply, and so magnified our economic contraction.

The worldwide crisis required a worldwide response. Chapter 3

describes both the actions taken by individual countries and those taken

through international institutions and cooperation. As described in the

leaders’ statement from the September summit of the Group of Twenty

(G-20) nations, the result was “the largest and most coordinated fiscal and

monetary stimulus ever undertaken” (Group of Twenty 2009). Just as the

actions in the United States have begun to turn the domestic economy

around, these international actions appear to have put the worst of the global

crisis behind us. But the firmness of the budding recovery varies consider-

ably across countries, and significant challenges still remain.

Rebalancing the Economy on the

Path to Full Employment

The path from budding recovery to full employment will surely be

a difficult one. The problems that sowed the seeds of the financial crisis

need to be dealt with so that the economy emerges from the recession with

a stronger, more durable prosperity. There needs to be a rebalancing of

the economy away from low personal saving and large government budget

deficits and toward investment. Our financial system must be strengthened

both to provide the lending needed to support the recovery and to reduce

the risk of future crises.

Saving and Investment

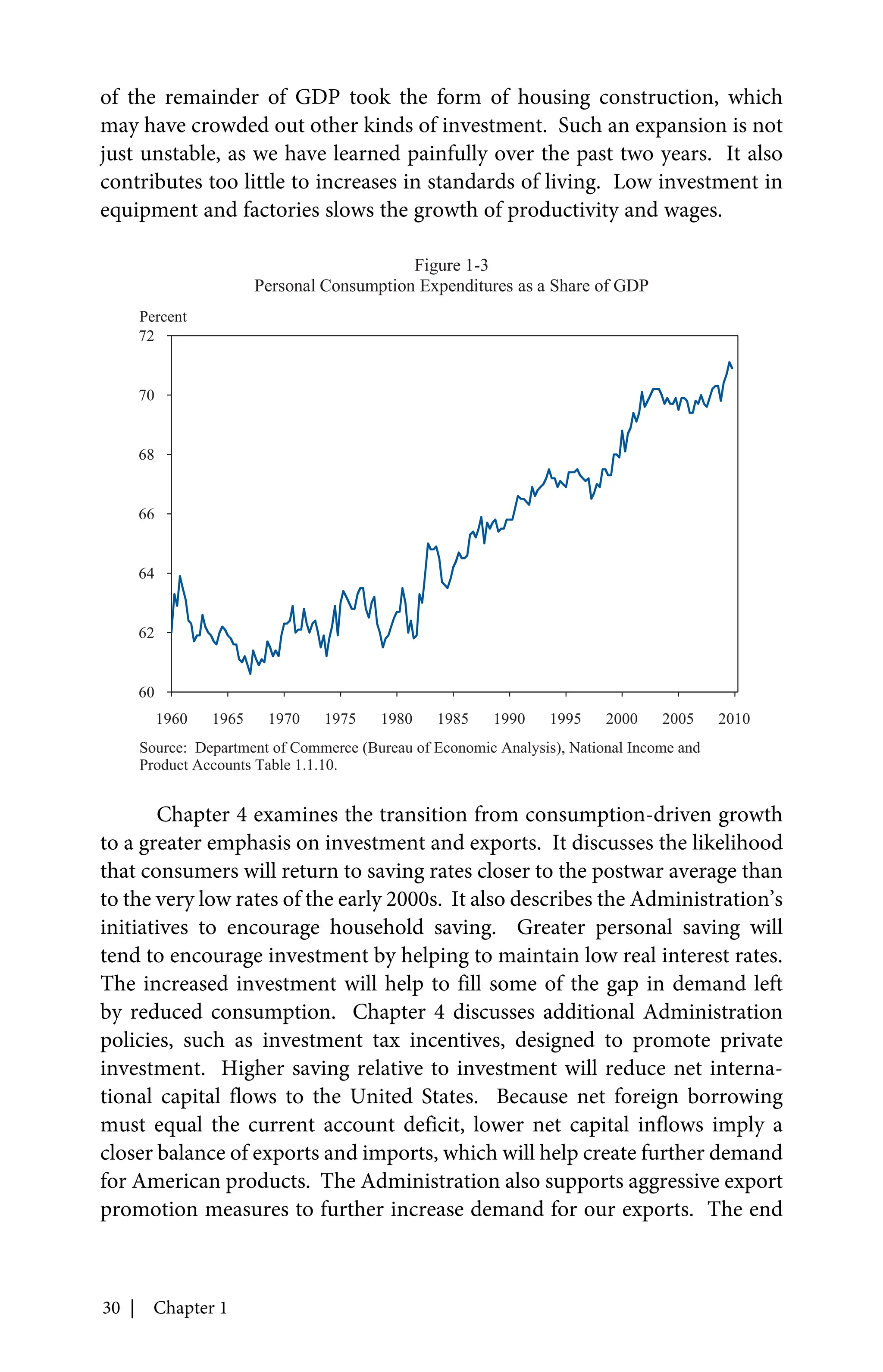

The expansion of the 2000s was fueled in part by high consumption.

As Figure 1-3 shows, the share of GDP that takes the form of consumption

has been on a generally upward trend for decades and reached unprec-

edented heights in the 2000s. The personal saving rate fell to exceptionally

low levels, and trade deficits were large and persistent. A substantial amount

34.

30 | Chapter1

of the remainder of GDP took the form of housing construction, which

may have crowded out other kinds of investment. Such an expansion is not

just unstable, as we have learned painfully over the past two years. It also

contributes too little to increases in standards of living. Low investment in

equipment and factories slows the growth of productivity and wages.

Chapter 4 examines the transition from consumption-driven growth

to a greater emphasis on investment and exports. It discusses the likelihood

that consumers will return to saving rates closer to the postwar average than

to the very low rates of the early 2000s. It also describes the Administration’s

initiatives to encourage household saving. Greater personal saving will

tend to encourage investment by helping to maintain low real interest rates.

The increased investment will help to fill some of the gap in demand left

by reduced consumption. Chapter 4 discusses additional Administration

policies, such as investment tax incentives, designed to promote private

investment. Higher saving relative to investment will reduce net interna-

tional capital flows to the United States. Because net foreign borrowing

must equal the current account deficit, lower net capital inflows imply a

closer balance of exports and imports, which will help create further demand

for American products. The Administration also supports aggressive export

promotion measures to further increase demand for our exports. The end

60

62

64

66

68

70

72

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

Figure 1-3

Personal Consumption Expenditures as a Share of GDP

Percent

Source: Department of Commerce (Bureau of Economic Analysis), National Income and

Product Accounts Table 1.1.10.

35.

To Rescue, Rebalance,and Rebuild | 31

result of this rebalancing will be an economy that is more stable, more

investment-oriented, and more export-oriented, and thus better for our

future standards of living.

Addressing the Long-Run Fiscal Challenge

A key part of the rebalancing that must occur as the economy returns

to full employment and beyond involves taming the Federal budget deficit.

Figure 1-4 shows the actual and projected path of the budget surplus based

on estimates released by the Congressional Budget Office (CBO) in January

2009, just before President Obama took office. As the figure makes clear,

the budget surpluses of the late 1990s turned to substantial deficits in the

2000s, and the deficits were projected to grow even more sharply over the

next three decades. As discussed in Chapter 5, the change to deficits in the

2000s largely reflects policy actions that were not paid for, such as the 2001

and 2003 tax cuts and the introduction of the Medicare prescription drug

benefit. The projection of steadily increasing future deficits is largely due to

the continuation of the decades-long trend of rising health care costs.

-20

-15

-10

-5

0

5

1990 2000 2010 2020 2030 2040

Figure 1-4

Actual and Projected Budget Surpluses in January 2009 under Previous Policy

Percent of GDP

Projected

Actual

Note: CBO baseline surplus projection adjusted for CBO’s estimates of costs of continued

war spending, continuation of the 2001 and 2003 tax cuts, preventing scheduled cuts in

Medicare’s physician payment rates, and holding other discretionary outlays constant as a

share of GDP.

Sources: Congressional Budget Office (2009a, 2009b).

36.

32 | Chapter1

Chapter 5 describes the likely consequences of these projected deficits

over time and the importance of restoring fiscal discipline. It also discusses

the President’s plan for facing this challenge. A period of severe economic

weakness is no time for a large fiscal contraction. Instead, the Nation must

tackle the long-run deficit problem through actions that address the under-

lying sources of the problem over time. The single most important step that

can be taken to reduce future deficits is to adopt health care reform that slows

the growth rate of costs without compromising the quality of care. In addi-

tion, the President’s fiscal 2011 budget includes other significant measures,

such as allowing President Bush’s tax cuts for the highest-income earners

to expire, reforming international tax rules to discourage tax avoidance and

encourage investment in the United States, and imposing a three-year freeze

in nonsecurity discretionary spending; alongside a proposal for a bipartisan

commission process to address the long-run gap between revenues and

expenditures.

Building a Safer Financial System

Risky credit practices both encouraged some of the imprudent rise in

consumption and homebuilding in the previous decade and set the stage for

the financial crisis. Chapter 6 analyzes the role that financial intermediaries

play in the economy and diagnoses what went wrong during the meltdown

of financial markets. The crisis showed that the Nation’s financial regula-

tory structure, much of which had not been fundamentally changed since

the 1930s, failed to keep up with the evolution of financial markets. The

current system provided too little protection for the economy from actions

that could threaten financial stability and too little protection for ordinary

Americans in their dealings with sophisticated and powerful financial insti-

tutions and other providers of credit. Strengthening our financial system is

thus a key element of the rebalancing needed to assure stable, robust growth.

Chapter 6 discusses financial regulatory modernization. What is

needed is a system where capital requirements and sensible rules are set

in a way to control excessive risk-taking; where regulators can consider

risks to the system as a whole and not just to individual institutions; where

institutions cannot choose their regulators; where regulators no longer face

the unacceptable choice between the disorganized, catastrophic failure of a

financial institution and a taxpayer-funded bailout; and where a dedicated

agency has consumer protection as its central mandate. For this reason, the

President put forward a comprehensive plan for financial regulatory reform

last June and is working with Congress to ensure passage of these critical

reforms this year.

37.

To Rescue, Rebalance,and Rebuild | 33

Rebuilding a Stronger Economy

Even before the crisis, the economy faced significant long-term

challenges. As a result, it was doing poorly at providing rising standards of

living for the vast majority of Americans. Figure 1-5 shows the evolution of

before-tax real median family income since 1960. Beginning around 1970,

slower productivity growth and rising income inequality caused incomes

for most families to grow only slowly. After a half-decade of higher growth

in the 1990s, the real income of the typical American family actually fell

between 2000 and 2006.

A central focus of Administration policy both over the past year

and for the years to come is to build a firmer foundation for the economy.

The President is committed to policies that will raise living standards for

all Americans.

Reforming Health Care

Health care is a key challenge that long predates the current economic

crisis. The existing system has left many Americans who have health insur-

ance inadequately covered, poorly protected against insurance industry

30,000

40,000

50,000

60,000

70,000

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

Figure 1-5

Real Median Family Income

2008 dollars

Notes: Income measure is total money income excluding capital gains and before taxes.

Annual income deflated using CPI-U-RS.

Source: Department of Commerce (Census Bureau), Current Population Survey, Annual

Social and Economic Supplement, Historical Income Table F-12.

38.

34 | Chapter1

abuses, and fearful of losing the insurance they have. And it has left tens of

millions of Americans with no insurance coverage at all. The system also

delivers too little benefit at too high a cost. Comparisons across countries

and, especially, across regions of the United States reveal large differences

in health care spending that are not associated with differences in health

outcomes and that cannot be fully explained by factors such as differences

in demographics, health status, income, or medical care prices. These large

differences in spending suggest that up to nearly 30 percent of health care

spending could be saved without adverse health consequences. The unnec-

essary growth of health care costs is eroding the growth of take-home pay

and is central to our long-run fiscal challenges. These adverse effects will

only become more severe if cost growth is not slowed.

To illustrate what could happen to workers’ earnings in the absence

of reform, Figure 1-6 shows the historical and projected paths of real total

compensation per worker (which includes nonwage benefits such as health

insurance) and total compensation net of health insurance premiums. As

health insurance premiums absorb a growing fraction of workers’ compen-

sation, the remaining portion of compensation levels off and then starts

to decline.

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

110,000

120,000

1999 2003 2007 2011 2015 2019 2023 2027 2031 2035 2039

Estimated annual total compensation

Estimated annual total compensation

net of health insurance premiums

Projected

Figure 1-6

Total Compensation Including and Excluding Health Insurance

2008 dollars per person

Actual

Note: Health insurance premiums include the employee- and employer-paid portions.

Sources: Actual data from Department of Labor (Bureau of Labor Statistics); Kaiser Family

Foundation and Health Research and Educational Trust (2009); Department of Health and

Human Services (Agency for Healthcare Research and Quality, Center for Financing, Access,

and Cost Trends), 2008 Medical Expenditure Panel Survey-Insurance Component. Projections

based on CEA calculations.

39.

To Rescue, Rebalance,and Rebuild | 35

Chapter 7 describes the actions the Administration and Congress

took in 2009 to begin the process of improvement, including an expansion

of the Children’s Health Insurance Program to provide access to health care

for millions of children and important investments in the modernization

of the health care system through the Recovery Act. It also describes the

key elements of successful health insurance reform and discusses the prog-

ress that has been made on reform legislation. Successful reform involves

making insurance more secure for those who have it and expanding coverage

to those who lack it. It must include delivery system reforms, reductions

in waste and improper payments in the Medicare system, and changes in

consumer and firm incentives that will slow the growth rate of costs substan-

tially, while maintaining and even improving quality. Slowing the growth

rate of health care costs will have benefits throughout the economy: it will

raise standards of living for families, help reduce the Federal budget deficit

relative to what it otherwise would be, benefit state and local governments,

and encourage job growth and improved macroeconomic performance.

Strengthening the American Labor Force

American workers have suffered greatly in the current recession.

As described in Chapter 8, long-term unemployment is at record levels.

The unemployment rate, which was 10 percent for the country as a