Downloaded 33 times

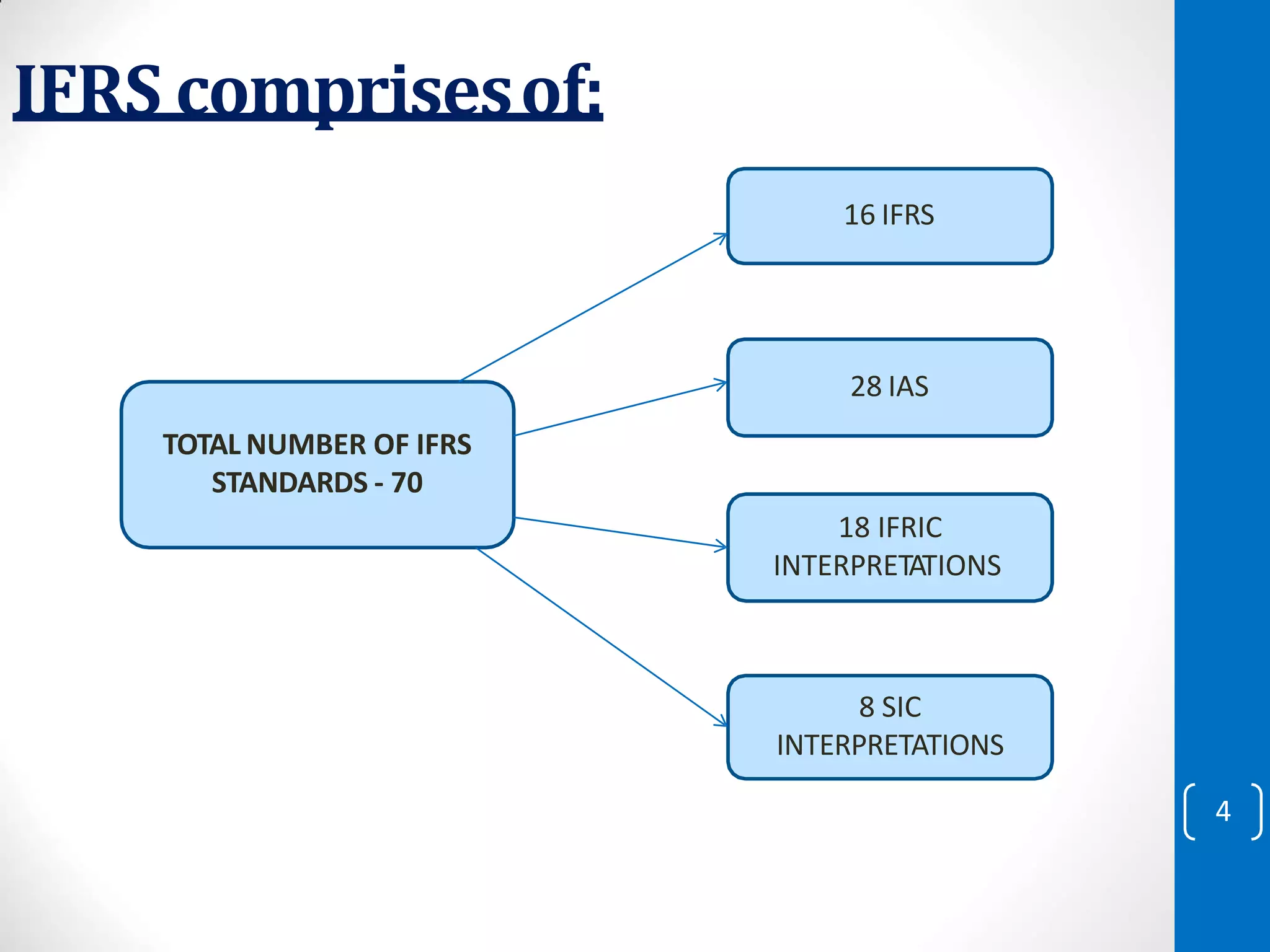

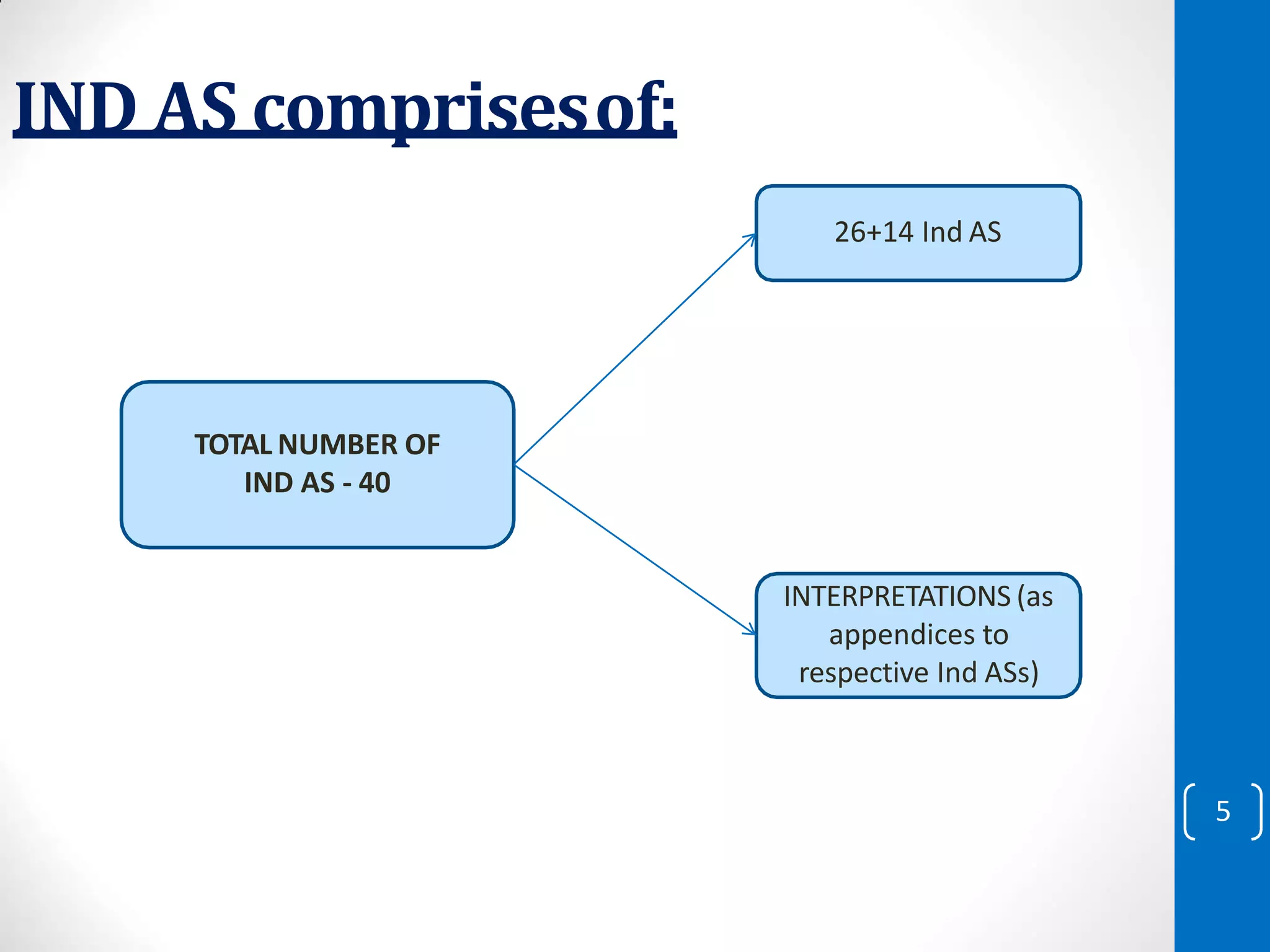

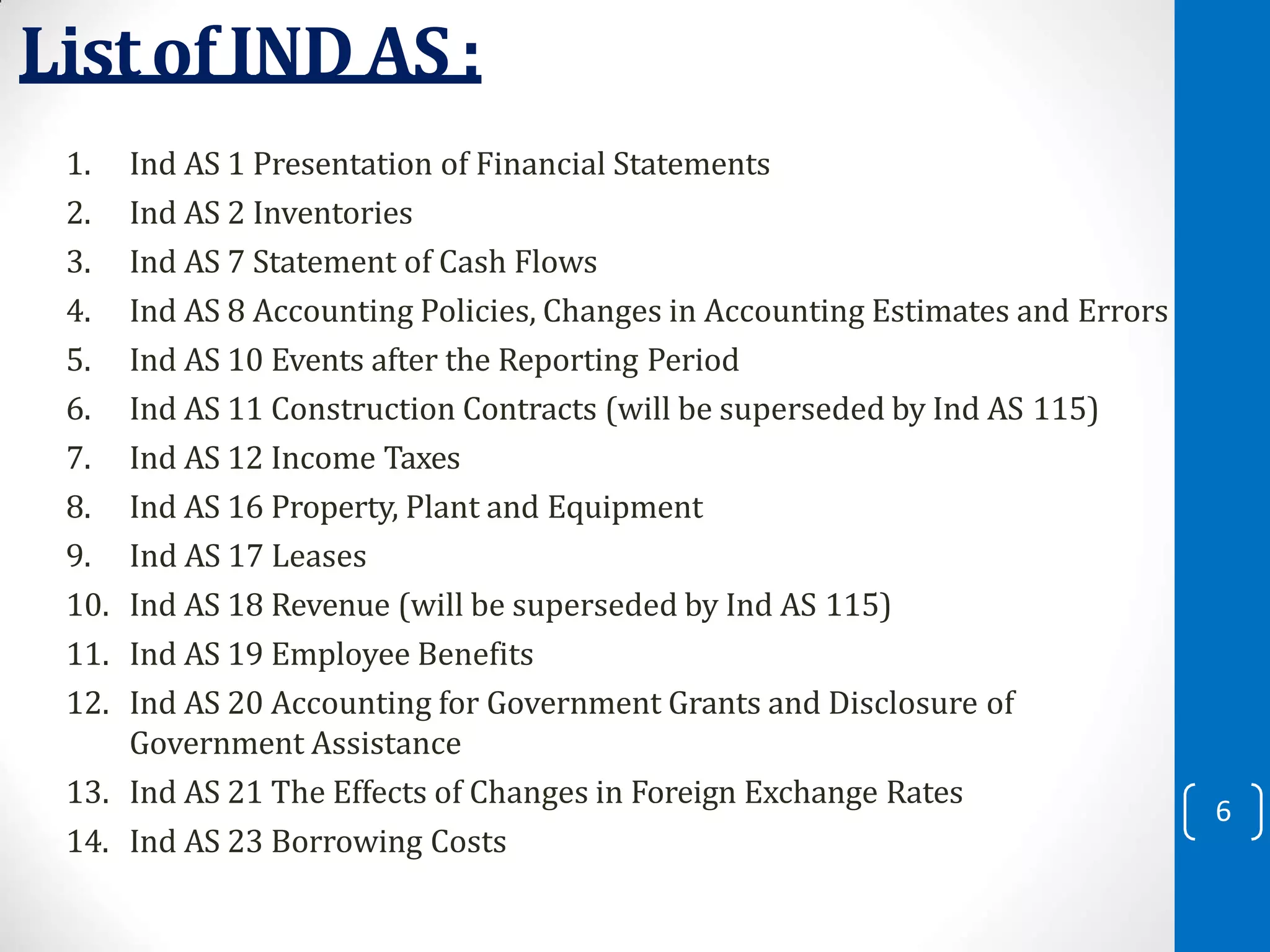

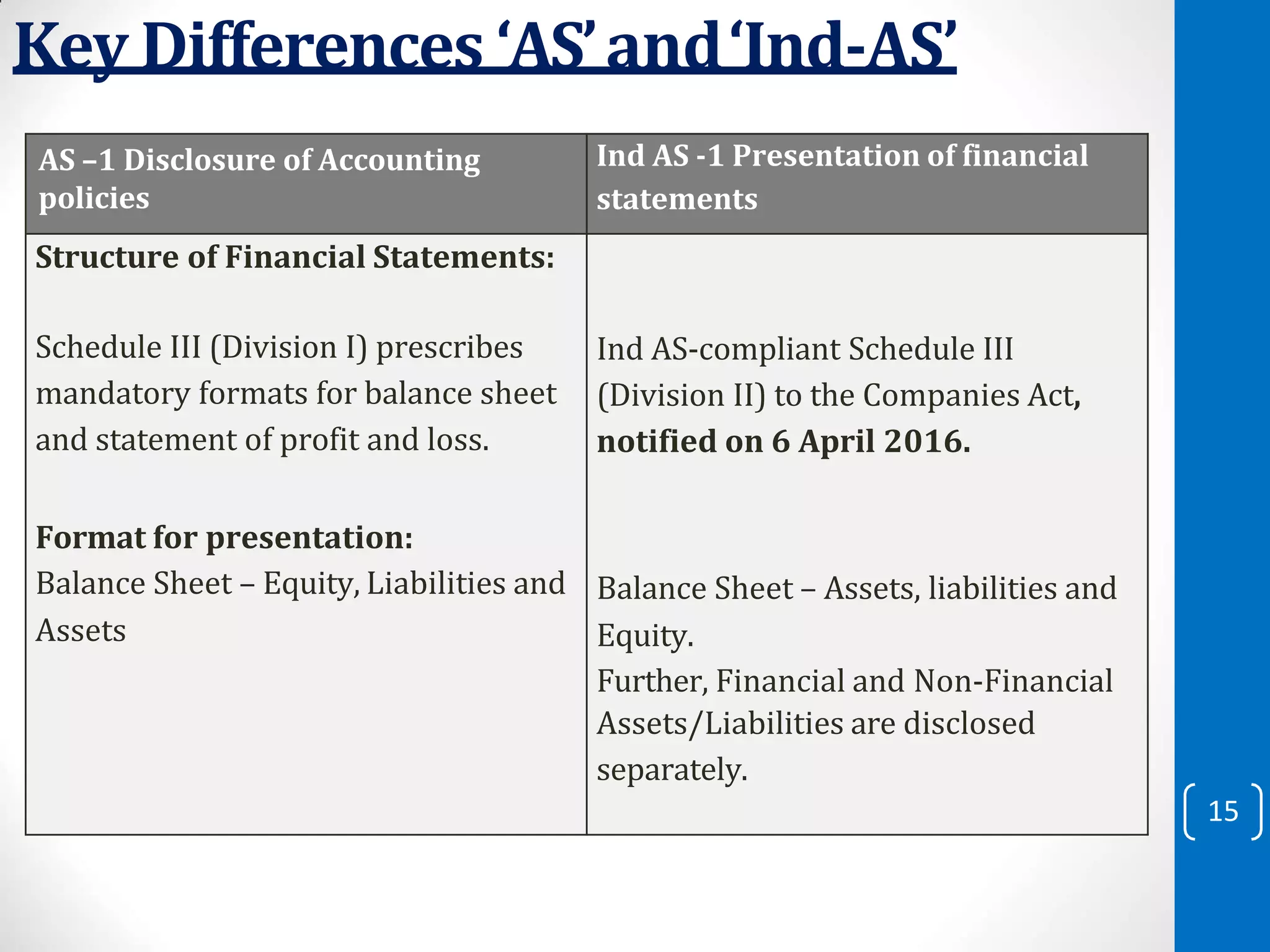

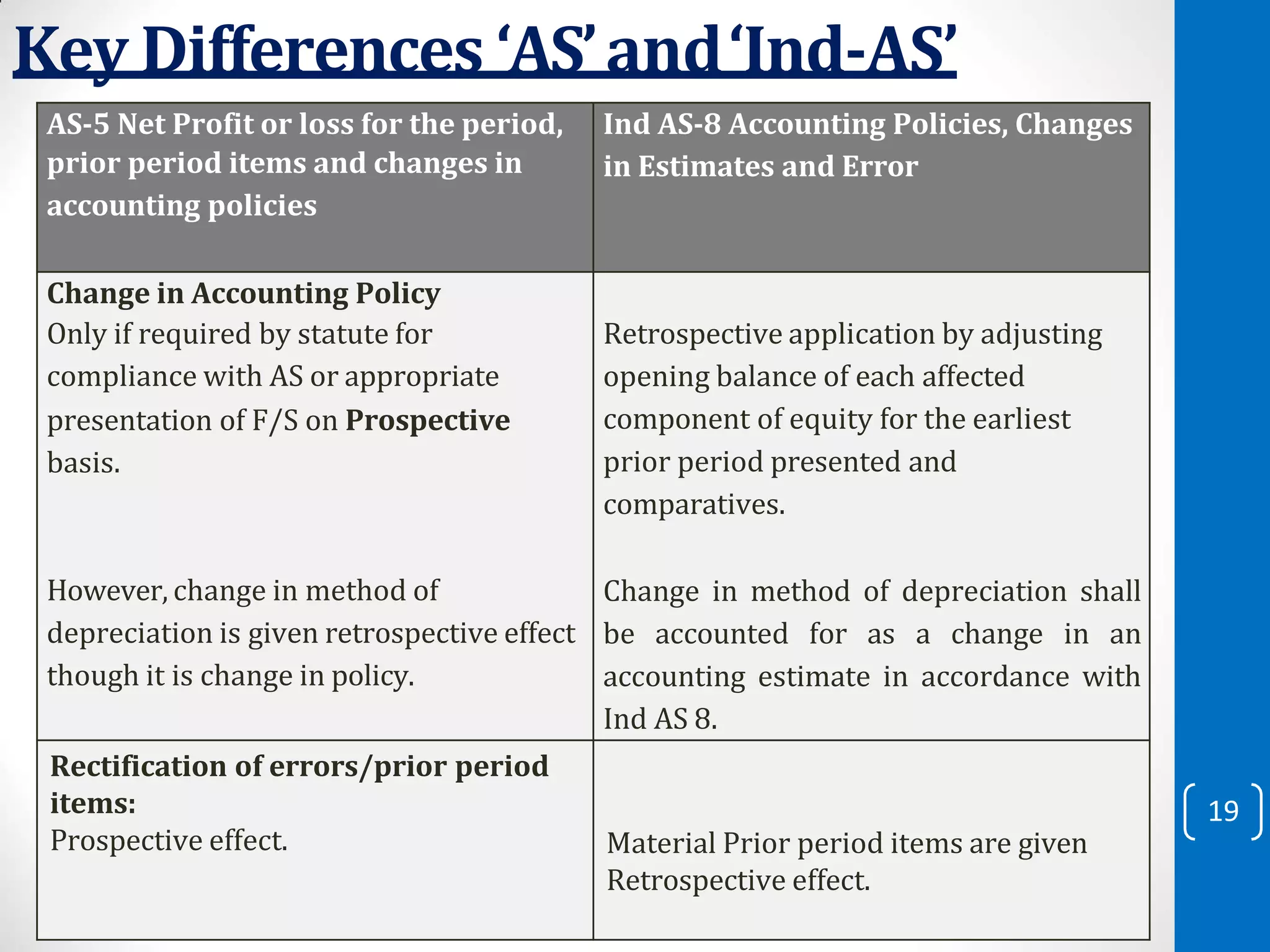

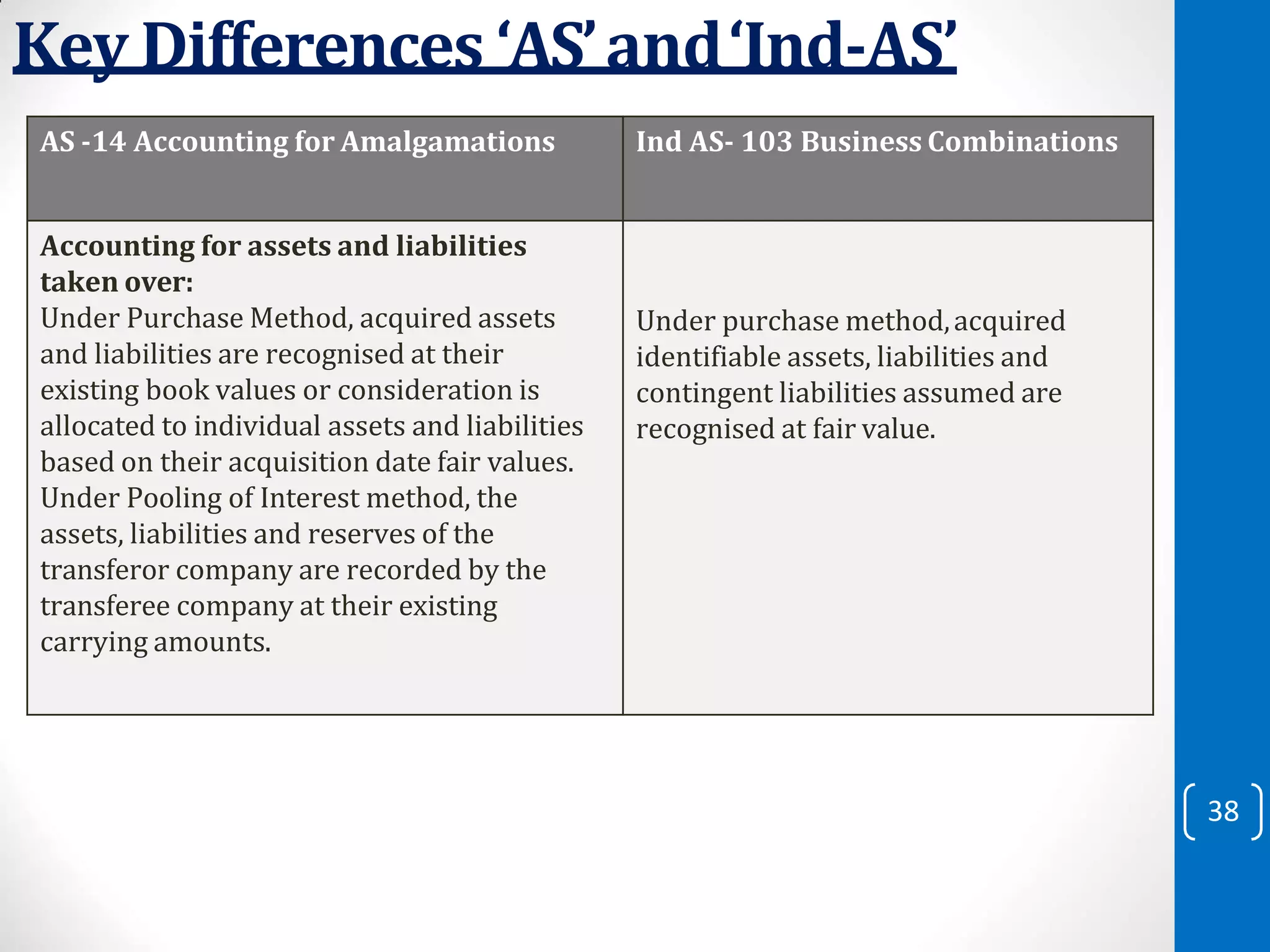

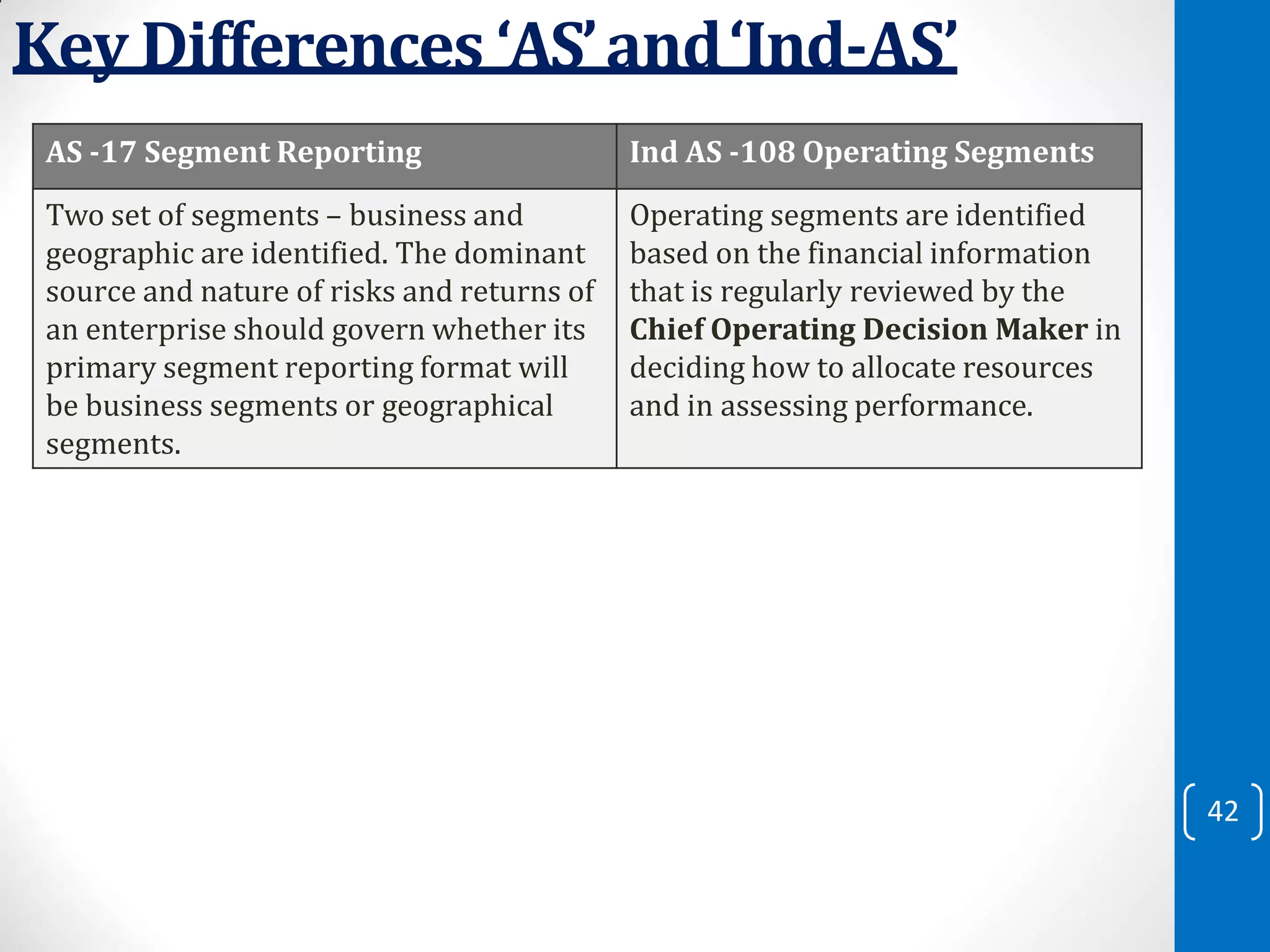

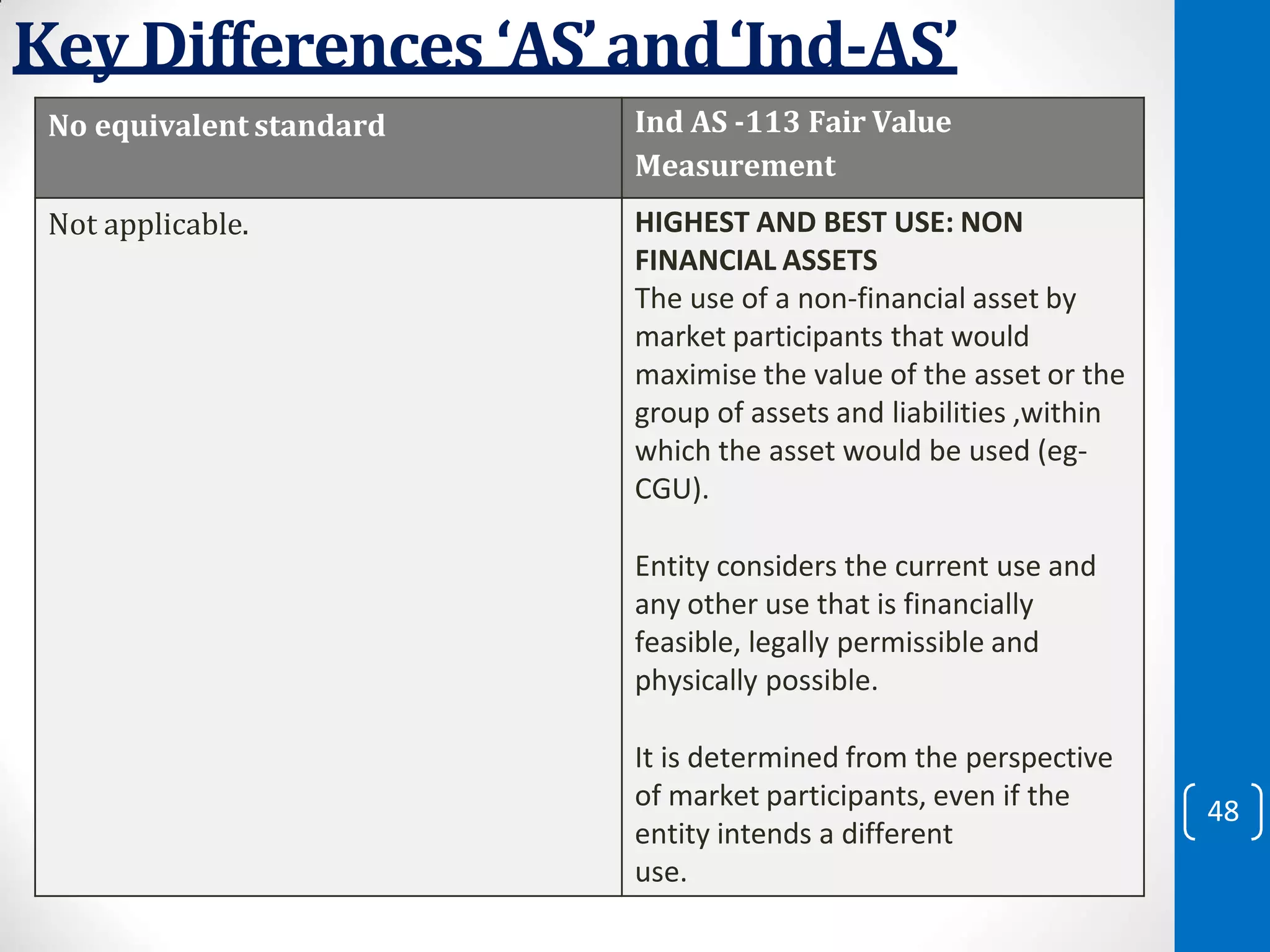

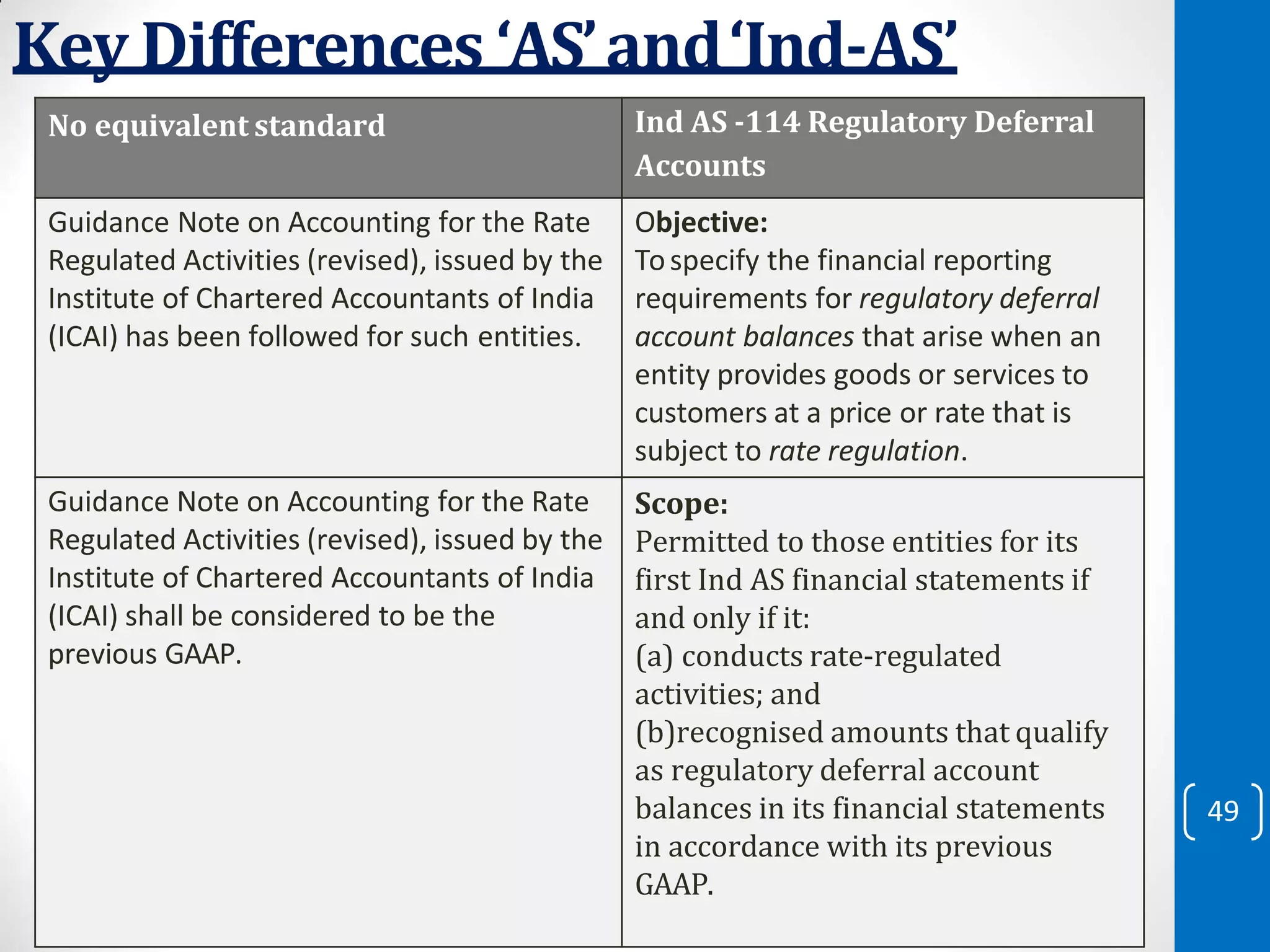

The document discusses the convergence of Indian Accounting Standards (Ind AS) with International Financial Reporting Standards (IFRS). It provides an overview of the need for IFRS, lists the various Ind AS and IFRS standards, and compares key differences between Indian Accounting Standards (AS) and Ind AS. The convergence roadmap for mandatory adoption of Ind AS by Indian companies of different sizes and industries at different time periods is also outlined. Some of the major differences highlighted between AS and Ind AS include the components of financial statements, treatment of extraordinary items and prior period errors, and accounting for proposed dividends and financial liability classification.

![Ind AS [ Indian Accounting Standards] - Applicablity](https://cdn.slidesharecdn.com/ss_thumbnails/indas-150610180302-lva1-app6892-thumbnail.jpg?width=640&height=640&fit=bounds)