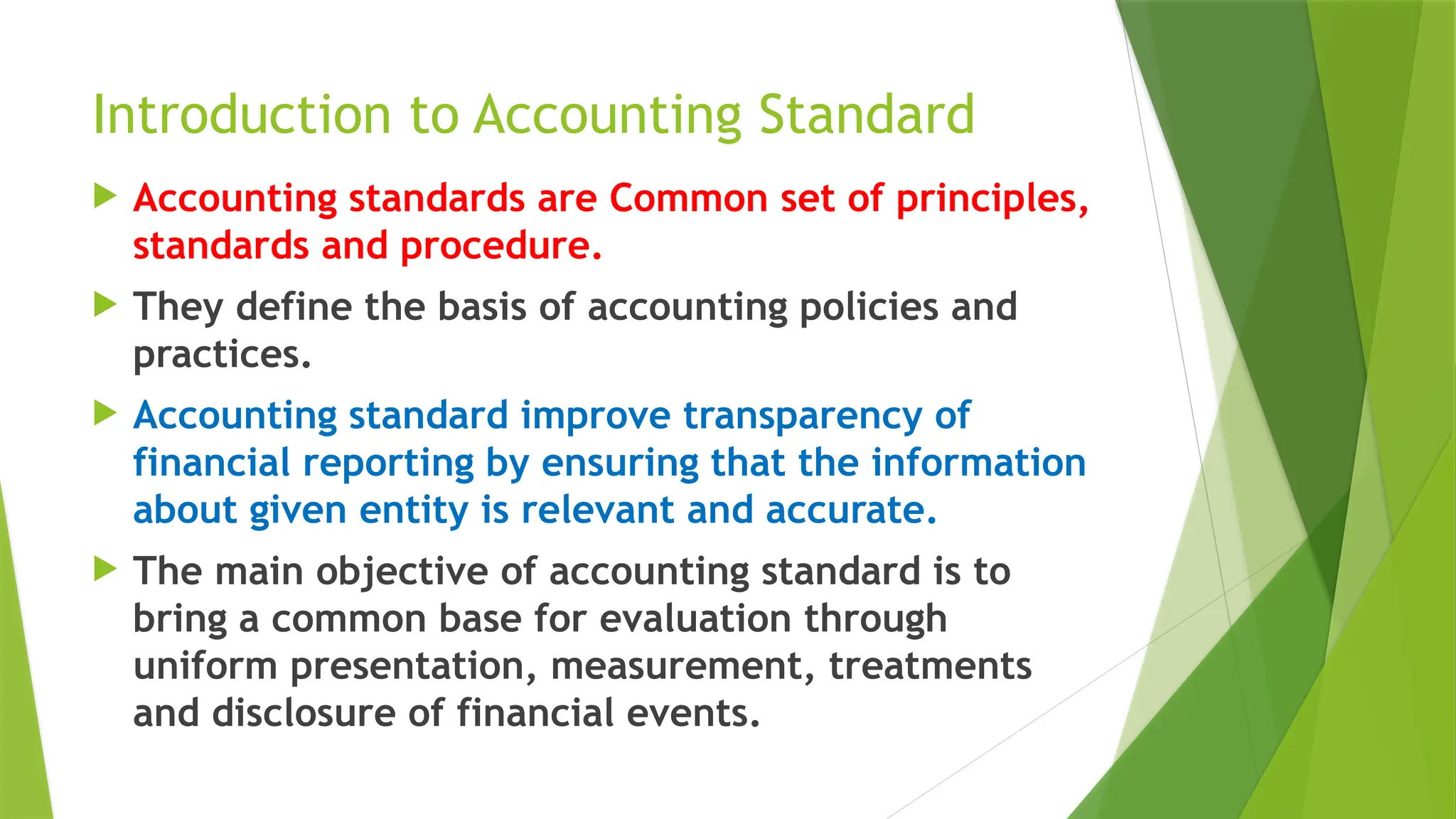

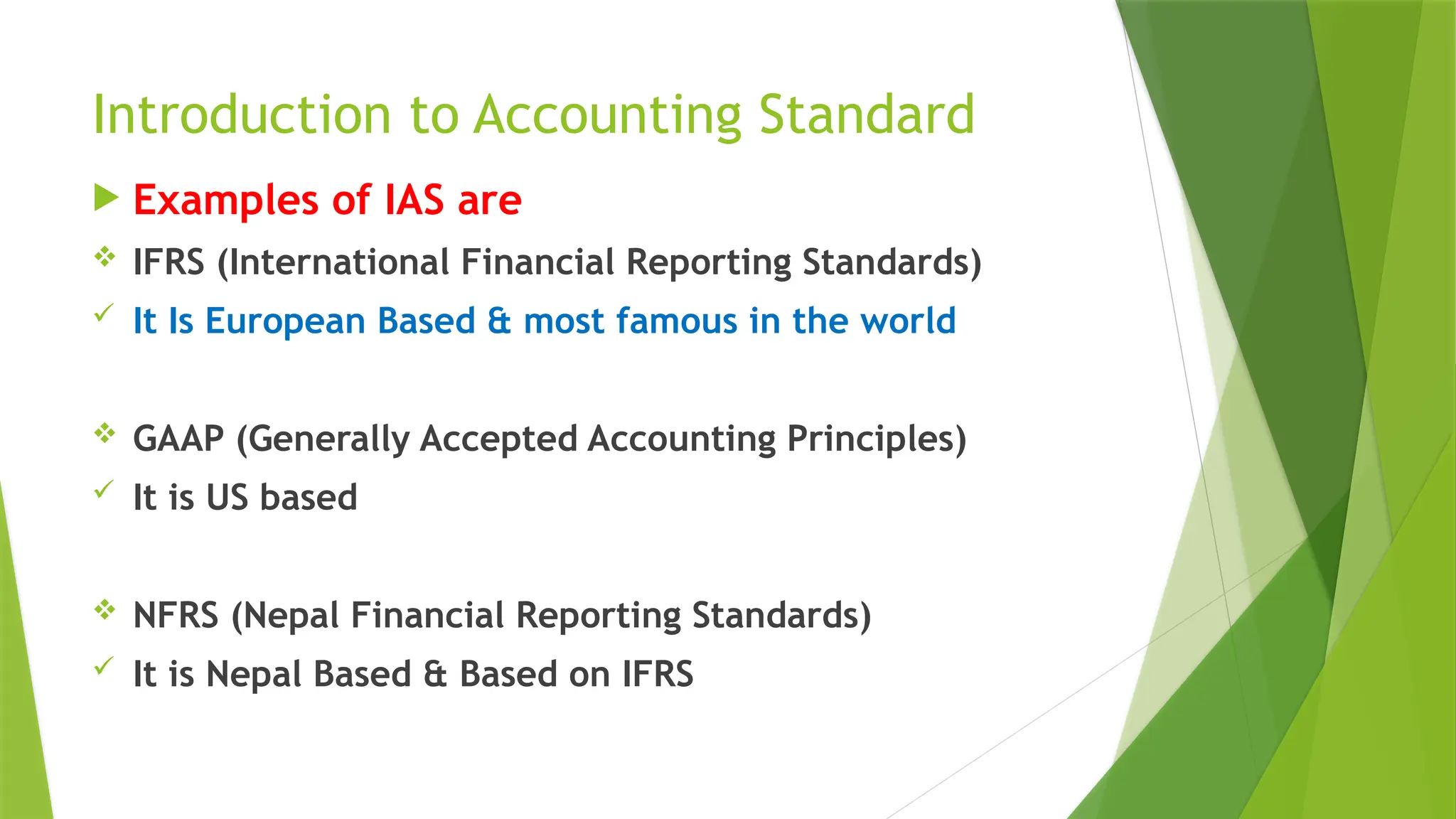

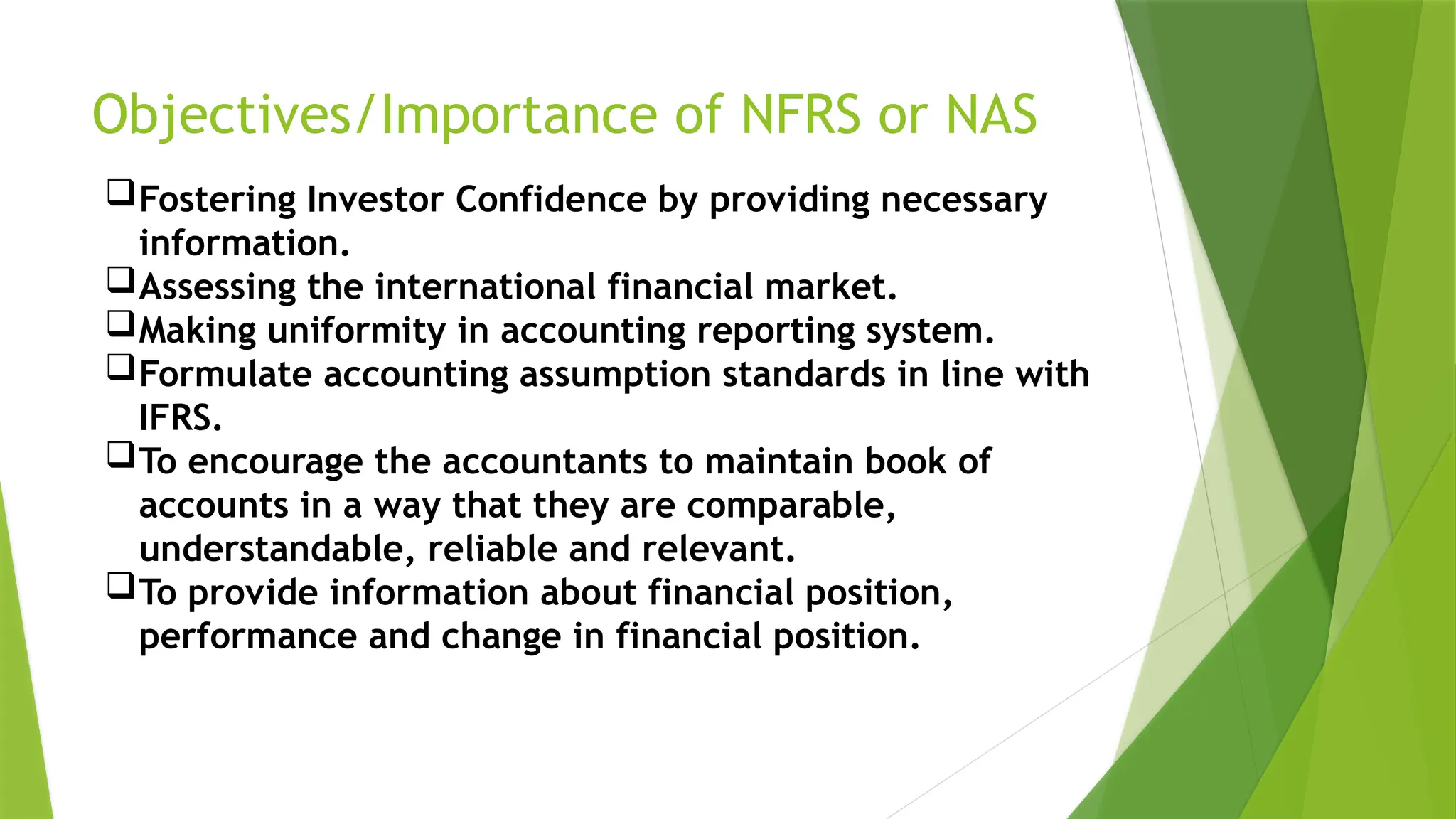

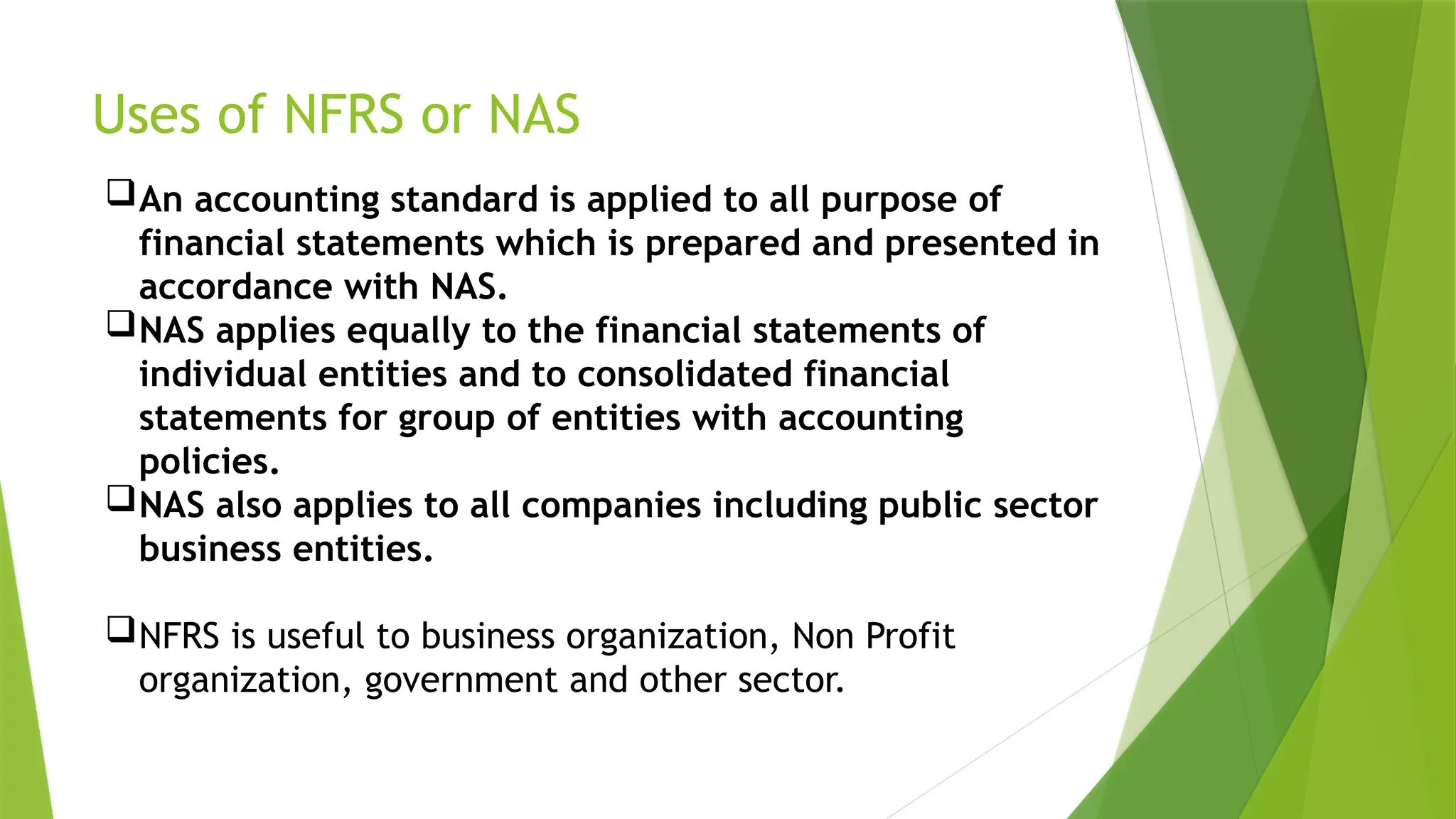

Accounting standards are sets of principles that enhance the transparency and accuracy of financial reporting. The Nepal Financial Reporting Standards (NFRS) were established by the Accounting Standard Board in 2003 to provide a uniform basis for financial reporting in Nepal, aligning with international standards like IFRS and GAAP. NFRS aims to foster investor confidence, ensure consistent accounting practices, and provide reliable financial information across all entities.

![Trial Balance [Autosaved].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/trialbalanceautosaved-230206035002-7c4f78dd-thumbnail.jpg?width=640&height=640&fit=bounds)