Unit Two: Auditingprofession and GAAS

2.1: Auditing profession

2.2: Generally Accepted Auditing Standards

2.2: Types of Audit reports

2.3: Parts of audit reports

2.4: Conditions for issuing different audit reports

2.5: Materiality and Auditors decisions

2.

Emergence of needfor Audit Reports

The prevalence of great business opportunities created

by growth in technology, improved communication &

transportation and expanding global markets proved owner

manager source of capital to be no more capable of

supporting the speed of entry to new markets internationally

nor the wealth-creating potential of the enterprises.

This lead to the need to pool resources through

savings of the community as a whole and hence

formation of large companies.

The result has been the growth of sophisticated securities

markets and credit-granting institutions serving the

financial needs of these large national, and increasingly

international, corporations.

3.

The flowof investor funds to the corporations and

the whole process of allocation of financial

resources through the securities markets have

become dependent to a very large extent on

financial reports made by company management.

One of the most important characteristics of these

corporations is the fact that their ownership is almost

totally separated from their management

Management has control over the accounting systems.

They are not only responsible for the financial reports to

investors, but they also have the authority to determine

the way in which the information is presented.

Emergence of need for Audit Reports

4.

Investors andcreditors may have different objectives

than management (e.g., management prefers higher

salaries and benefits (expenses), whereas investors

wish higher profits and dividends).

Investors and creditors must depend on fair

reporting of the financial statements.

To give them confidence in the financial

statements, an auditor provides an

independent and expert opinion on the

fairness of the reports, called an audit opinion.

Emergence of need for Audit Reports

5.

User Demand forReliable Information

Today’s information

More complex

Demanded by remote users

Demanded in a more timely manner

Has far reaching consequences

Information risk

The risk that the information disseminated by a

company will be materially false or misleading.

Users demand an independent third party

assessment of the information

Business risk

The risk that an entity will fail to meet its stated

business objectives

1-5

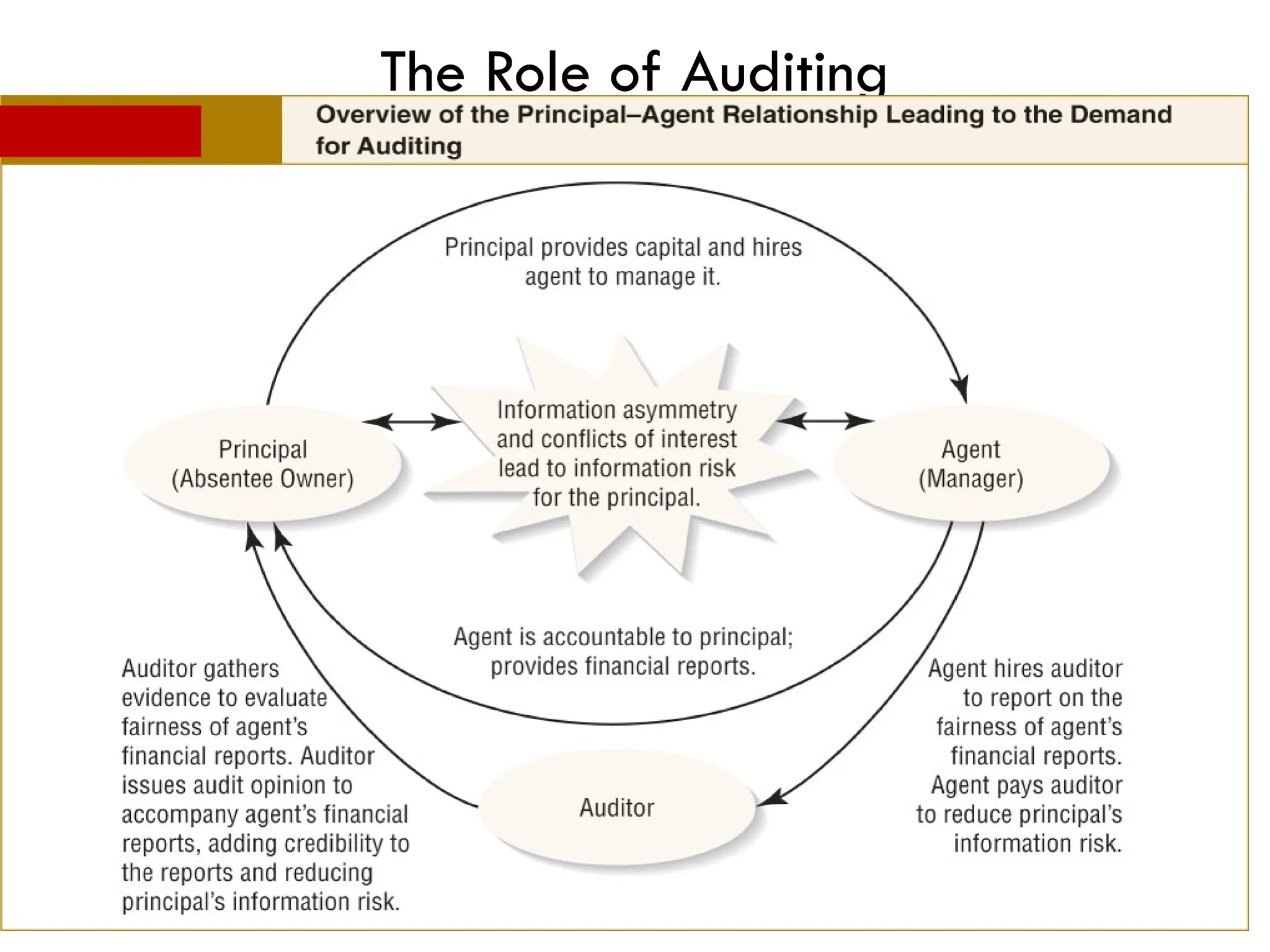

6.

Why Audit ?

Legal and Contractual Requirements

Restrictive Covenants in Debt Agreements

Modern Corporation Setup –

Absentee Stockholders and professional Managers

Principal –Agent Relationships

Lack on information symmetry

Conflicts of Interest

Cost Effective Monitoring Device

7.

The Auditor, Corporationsand Financial

Information

i. Audits Required

• In most countries, audits are now legally required for some

types of companies (statutory audits)

– E.g., listed companies, companies receiving government

money, certain industries

• Major stock exchange centers/ Bourses (including NYSE,

NASDAQ, London Stock Exchange, Tokyo NIKKEI, and

Frankfurt DAX) have listing rules that require all companies

to have an audited annual report.

8.

It canbe said that the function of auditing is to lend

credibility to the financial statements.

The financial statements are the responsibility of

management and the auditor’s responsibility is to lend

them credibility.

By the audit process, the auditor enhances the

usefulness and the value of the financial statements,

but also increases the credibility of other non-audited

information released by management.

The Auditor, Corporations and Financial

Information

ii. The Importance of Auditing

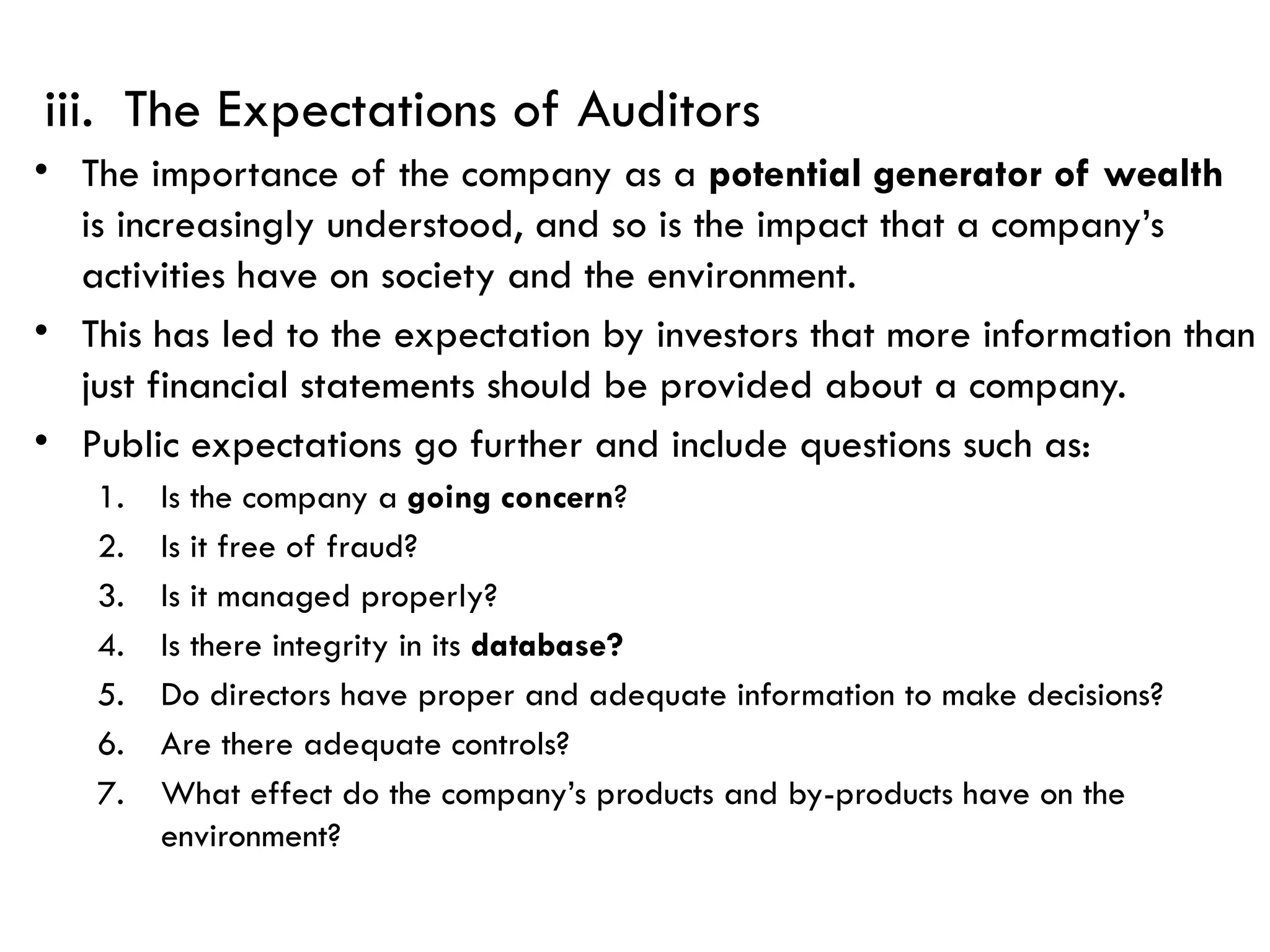

iii. The Expectationsof Auditors

• The importance of the company as a potential generator of wealth

is increasingly understood, and so is the impact that a company’s

activities have on society and the environment.

• This has led to the expectation by investors that more information than

just financial statements should be provided about a company.

• Public expectations go further and include questions such as:

1. Is the company a going concern?

2. Is it free of fraud?

3. Is it managed properly?

4. Is there integrity in its database?

5. Do directors have proper and adequate information to make decisions?

6. Are there adequate controls?

7. What effect do the company’s products and by-products have on the

environment?

11.

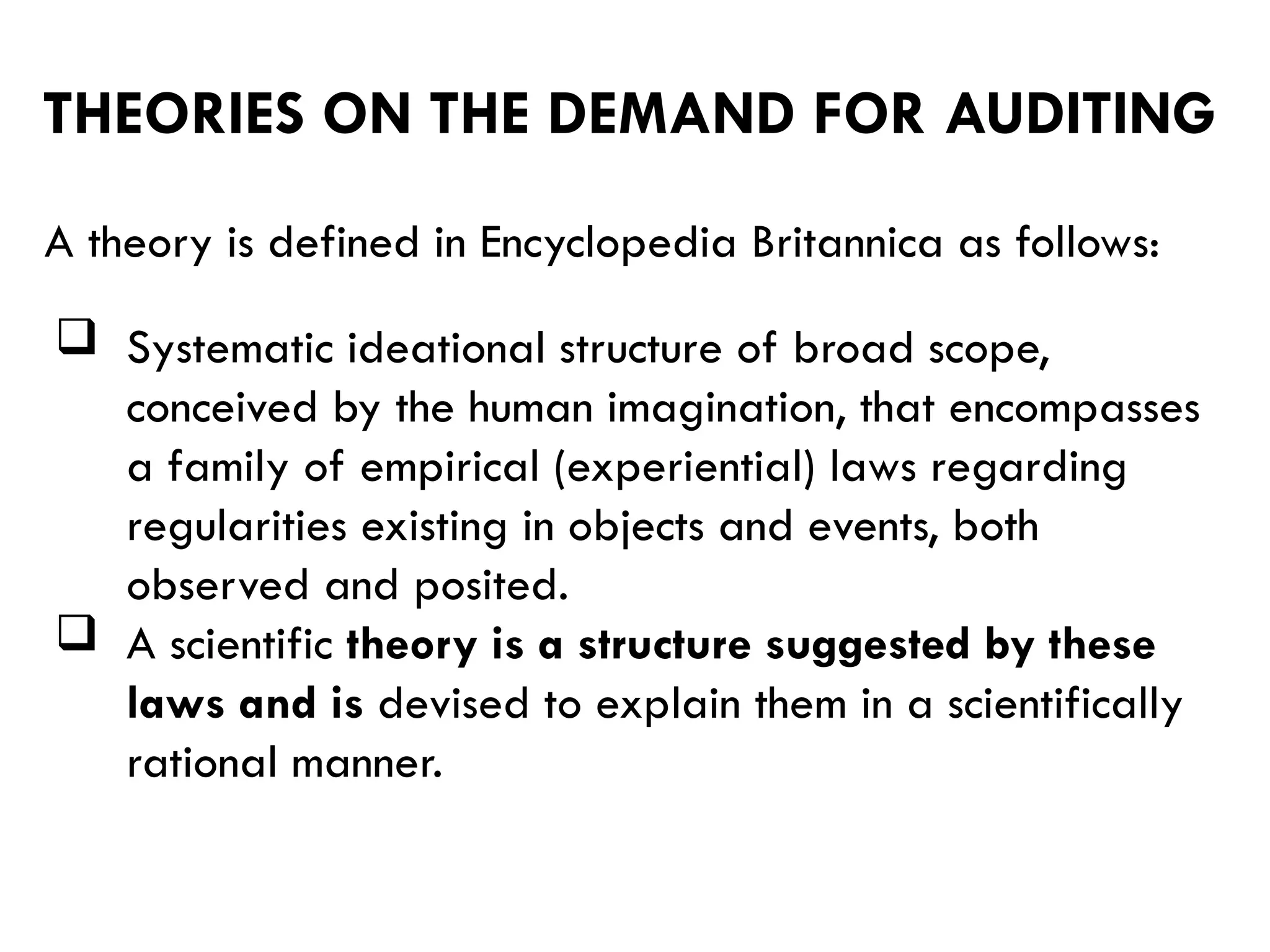

THEORIES ON THEDEMAND FOR AUDITING

A theory is defined in Encyclopedia Britannica as follows:

Systematic ideational structure of broad scope,

conceived by the human imagination, that encompasses

a family of empirical (experiential) laws regarding

regularities existing in objects and events, both

observed and posited.

A scientific theory is a structure suggested by these

laws and is devised to explain them in a scientifically

rational manner.

12.

Mautz andSharaf (1961) define the purpose of theory

in the following way: “One reason, then, for a serious

and substantial investigation into the possibility and

nature of auditing theory is the hope that it will provide

us with solutions or, at least, clues to solutions, of

problems which we now find difficult”.

Theories on the demand for auditing provide a general

framework for auditing, or at least for understanding it.

THEORIES ON THE DEMAND FOR

AUDITING

13.

Auditing theory

helps explain why auditing is needed in the first

place

helps explain why some of the postulates and key

concepts of auditing are so important

uncovers some of the laws that govern the audit

process and its activities.

provides us with a framework for understanding

the relationships and interrelationships between

different parties of a firm.

THEORIES ON THE DEMAND FOR AUDITING

14.

There areseveral different theories that may explain

the demand for audit Services.

There are four important audit theories that explain the

demand for audit services:

1. The policeman theory

2. The lending credibility theory

3. The theory of inspired confidence

4. Agency Theory

15.

1. The policemantheory

The policeman theory claims that the auditor is

responsible for searching, discovering and preventing

fraud.

In the early 20th century this was certainly the case.

However, more recently the main focus of auditors has

been to provide reasonable assurance and verify the

truth and fairness of the financial statements.

The detection of fraud is, however, still a hot topic in

the debate on the auditor's responsibilities, and typically

after events where financial statement frauds have been

revealed, the pressure increases on increasing the

responsibilities of auditors in detecting fraud.

16.

The lendingcredibility theory suggests that the primary

function of the audit is to add credibility to the financial

statements.

In this view the service that the auditors are selling to the

clients is credibility.

Audited financial statements are seen to have elements

that increase the financial statement users’ confidence in

the figures presented by management.

Under this it is believed that the quality of investment

decisions will improve when they are based on reliable

and credible information.

2. The lending credibility theory

17.

Addresses boththe demand and the supply for audit

services

States that the demand for audit services is the direct

consequence of the participation of third parties or

outside stakeholders in the company.

These parties demand accountability from the

management, in return for their investments in the

company.

Accountability is realized through the issuance of periodic

financial reports.

3.The theory of inspired confidence or Theory of

rational expectations

18.

Though, informationprovided by the management could

be biased due to conflict of interest, and outside parties

do not have direct means of monitoring, an audit is

required to assure the reliability of this information.

With regard to the supply of audit assurance, Limperg

(1932) suggests that the auditor should always strive to

meet the public expectations.

Theory of rational expectations

19.

Agency theory(Watts and Zimmerman 1978, 1986a,

1986b) suggests that the auditor is appointed in the

interests of both the third parties as well as the

management.

A company is viewed as a web of contracts.

Several groups (suppliers, bankers, customers, employees

etc.) make some kind of contribution to the company for a

given price.

4. Agency theory

20.

The taskof the management is to coordinate these

groups and contracts and try to optimize them by way

of:

low price for purchased supplies,

high price for sold goods,

low interest rates for loans,

high share prices and

low wages for employees.

In these relationships, management is the agent,

which tries to gain contributions from principals

(bankers, shareholders, employees etc).

4. Agency theory

21.

The role ofthe audit

Related, and to some extent overlapping, with the four

theories discussed above, Wallace (1980) proposed

three hypotheses for explaining the role of the audit in

free and regulated markets:

1. the monitoring hypothesis,

2. the information hypothesis and

3. the insurance hypothesis.

22.

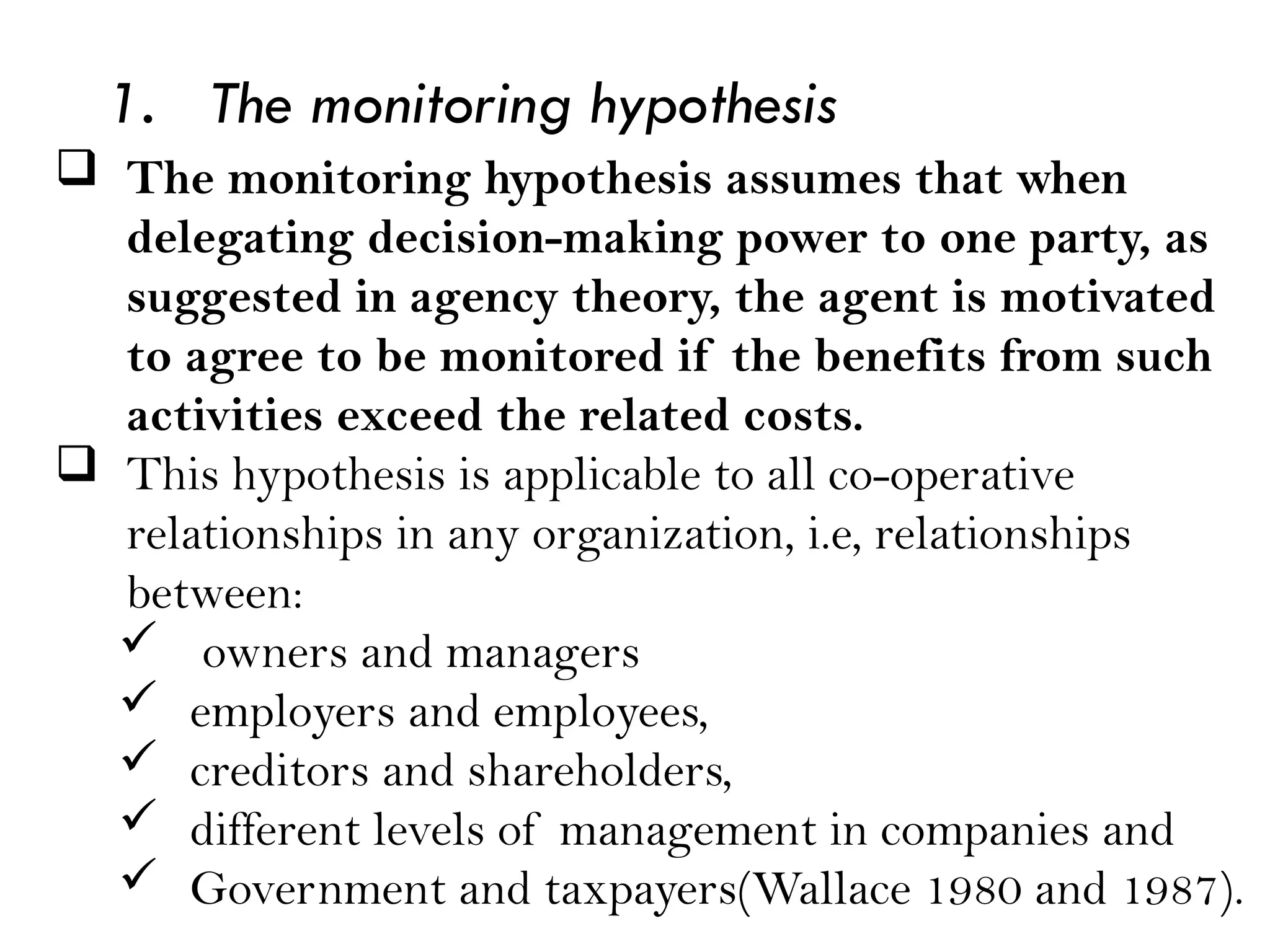

1. The monitoringhypothesis

The monitoring hypothesis assumes that when

delegating decision-making power to one party, as

suggested in agency theory, the agent is motivated

to agree to be monitored if the benefits from such

activities exceed the related costs.

This hypothesis is applicable to all co-operative

relationships in any organization, i.e, relationships

between:

owners and managers

employers and employees,

creditors and shareholders,

different levels of management in companies and

Government and taxpayers(Wallace 1980 and 1987).

23.

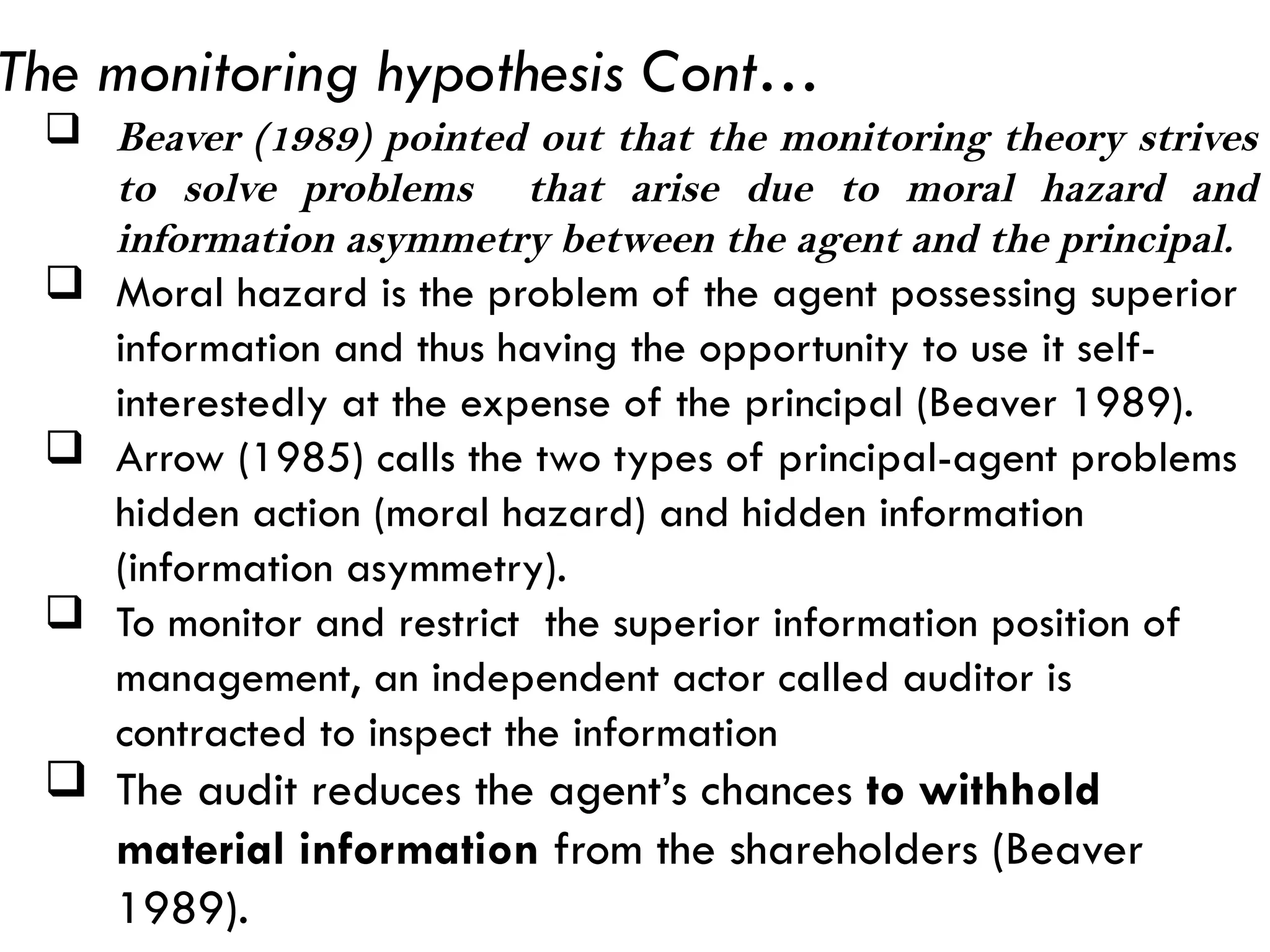

Beaver (1989)pointed out that the monitoring theory strives

to solve problems that arise due to moral hazard and

information asymmetry between the agent and the principal.

Moral hazard is the problem of the agent possessing superior

information and thus having the opportunity to use it self-

interestedly at the expense of the principal (Beaver 1989).

Arrow (1985) calls the two types of principal-agent problems

hidden action (moral hazard) and hidden information

(information asymmetry).

To monitor and restrict the superior information position of

management, an independent actor called auditor is

contracted to inspect the information

The audit reduces the agent’s chances to withhold

material information from the shareholders (Beaver

1989).

The monitoring hypothesis Cont…

24.

2. The informationhypothesis

Financial reporting was earlier seen to be central to the

monitoring purposes

Since the 1960’s the focus moved towards the need and

the provision of information to enable users to take

economic decisions (Higson 2003) which is the focus of the

information hypothesis

One argument regarding the demand for audited

financial statements is that they provide information

that is useful in investors’ decision-making

25.

Fama andLaffer (1971) discuss three major benefits of

information:

reduction of risk,

improvement of decision-making and

Provide gains from stock trade by investors

The information hypothesis emphasizes that financial

information is needed by investors to determine market

values, which are the basis for rational investment

decisions in the absence of an explicit contract with the

agent (Wallace 1980).

2. The information hypothesis

26.

3. The insurancehypothesis

The third hypothesis on how the demand for audits

evolves relates to management’s liability exposure

(Wallace 1980).

The auditor and the auditee are jointly and severally

liable to third parties for losses attributable to defective

financial statements.

The ability to shift financial responsibility for reported

data to an auditor lowers the expected loss from

litigation or related settlements to managers, creditors

and other professionals involved in the securities market.

The shift made is for high audit premium in exchange for

a guarantee or insurance from the auditor

27.

There arefour explanations why managers and other

professionals look for insurance from auditors rather

than an insurance company

3. The insurance hypothesis

First, the audit function is so firmly established in society

that the decision of management not to hire an auditor

would strongly imply negligence or fraud on the part of

the managers of other professionals.

Second, accounting firms have established in-house

legal departments to defend them in professional

liability suits.

Third, the auditor facing a litigation suit is concerned

about his/her reputation

Fourth, auditors have “deep pockets” relative to a

bankrupt or failing company that cannot pay.

28.

Auditing profession

Tounderstand the importance of a code of ethics to auditors and

other professionals, one must understand the nature of a profession.

Unfortunately there is no universally accepted definition of what

constitutes a profession. Yet for generations, certain types of

activities have been recognized as professions while others have not.

Medicine, law, engineering, theology are examples of disciplines

having long accorded professional status. Auditing is a relatively

newcomer to the ranks of the profession, but it has achieved

widespread recognition in recent times.

A profession is a discipline that involves a responsibility to serve the

public.

29.

Auditing profession

Auditing asa profession and just like other professions has some

common characteristics. The most important of these characteristics

are:

1. Responsibility to serve the public: Certified public accountants or

simply auditors are the representatives of the public -creditors,

stockholders, consumers, employees and other users of financial

reports.

The role of the independent auditor is to assure that financial

statements are fair to all parties and not biased to benefit one

group at the expense of another.

This responsibility to serve the public interest must be a basic

motivation for the professional.

There is a saying in public accounting that “The public is our

only client.”

30.

Auditing profession

Ithas been claimed by public accountants that Auditing is more

responsible to the public than any other professions.

This is because millions of clients might be affected if the

auditor is negligent in his professional act.

Usually one client might be affected if the Physician or attorney

is negligent in his professional act.

That is why public accountants say no profession is more

responsible to the public like auditing.

Public accountant must maintain a high degree of independence

from their client if they are to serve the large community.

31.

Auditing profession

2. ComplexBody of Knowledge: Auditing as a profession has

specialized body of knowledge that every member of the profession

should acquire through formal education.

Auditing like other professions has complex accumulated body of

knowledge.

Any practitioner or student of accounting and auditing has only to look

at the abundance of authoritative pronouncements governing financial

reports to realize that accounting and auditing are complex body of

knowledge.

As the environment changes, accounting and auditing principles and

practices must adapt.

The need for technical competence and familiarity with current

standards of practice is embodied in the code of professional conduct

32.

Auditing profession

3. Standardsof admission to the profession:

Obtaining a license to practice as certified public

accountant requires an individual to meet minimum

standards for education and experience.

The individual must also pass the CPA examination

showing mastery of the body of knowledge.

The admission to practice as public accountant is

restricted by legal and educational requirements so as

to provide quality service to the society.

33.

Auditing profession

4. ProfessionalAssociations: There are a number of

professional associations which are devoted them selves

with the development of auditing principles and standards.

The ten generally accepted auditing standards are the

guidelines developed by AICPA.

5. Need for public confidence: Certified public accountants

must have the confidence of the public to be successful.

The CPAs product is credibility and hence the public

confidence is of special significance. With out public

confidence the attest function serves no useful purpose.

34.

6. Professional Ethics

Ethics can be defined broadly as a set of moral

principles or values.

Each of us has such a set of values.

We may or may not have considered them explicitly.

Need for Ethics

Ethical behavior is necessary for a society to function

in an orderly manner.

The need for ethics in society is sufficiently

important that many commonly held ethical values

are incorporated into laws.

35.

Professional Ethics: professionalethics refers to the basic

principles of right action for the member of a profession.

Professional ethics may be regarded as a mixture of moral and

practical concepts.

Professional ethics in public accounting as in other professions

have been developed gradually and are still in a process of

change as the practice of accounting it self changes.

The fundamental purpose of such codes is to provide

members with guidelines for maintaining a professional

attitude and conducting themselves in a manner that will

enhance the professional status of their discipline.

36.

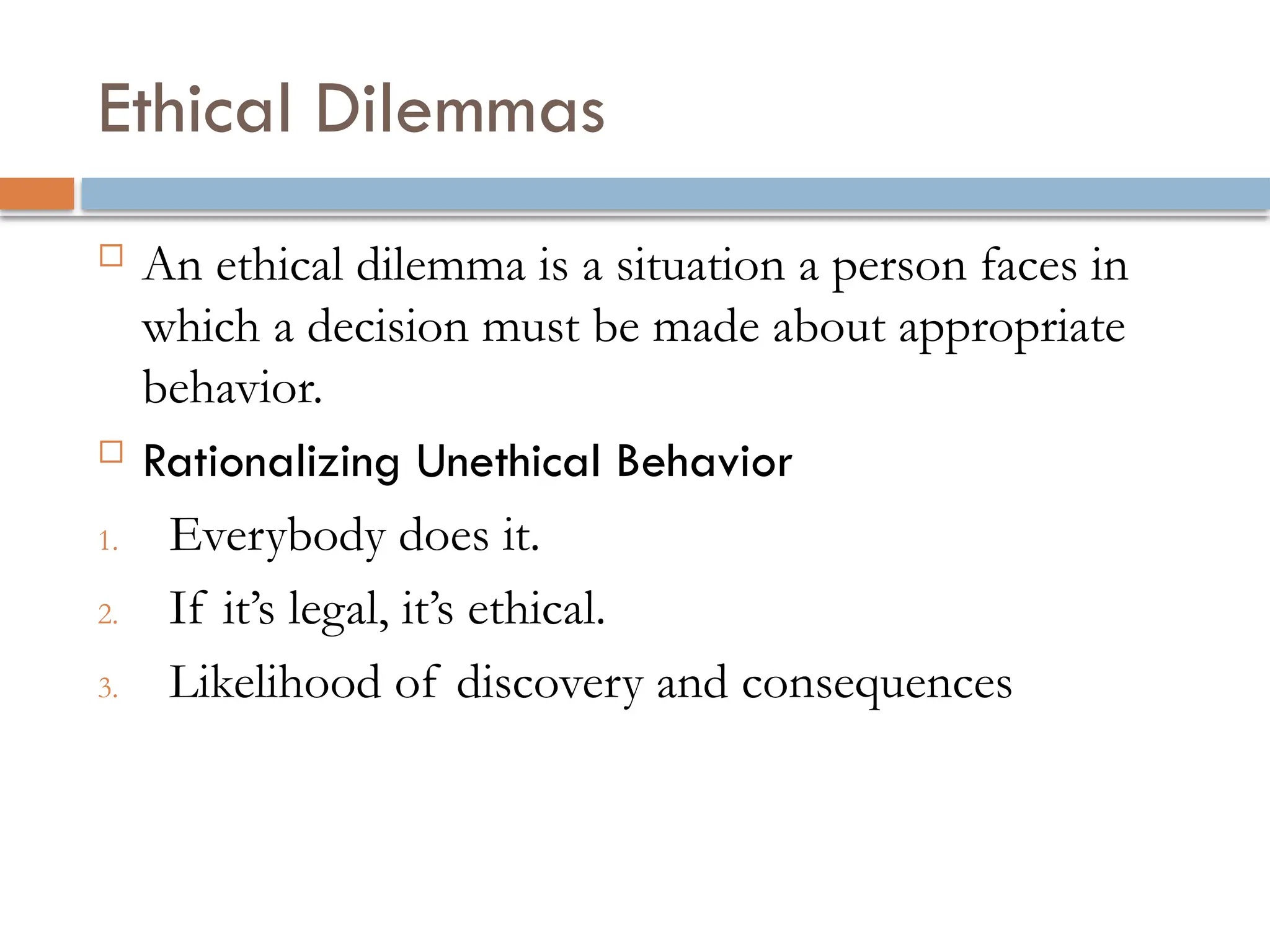

Ethical Dilemmas

Anethical dilemma is a situation a person faces in

which a decision must be made about appropriate

behavior.

Rationalizing Unethical Behavior

1. Everybody does it.

2. If it’s legal, it’s ethical.

3. Likelihood of discovery and consequences

37.

Special Need forEthical Conduct in Professions

Our society has attached a special meaning to the

term professional.

A professional is expected to conduct himself or

herself at a higher level than most other members

of society.

38.

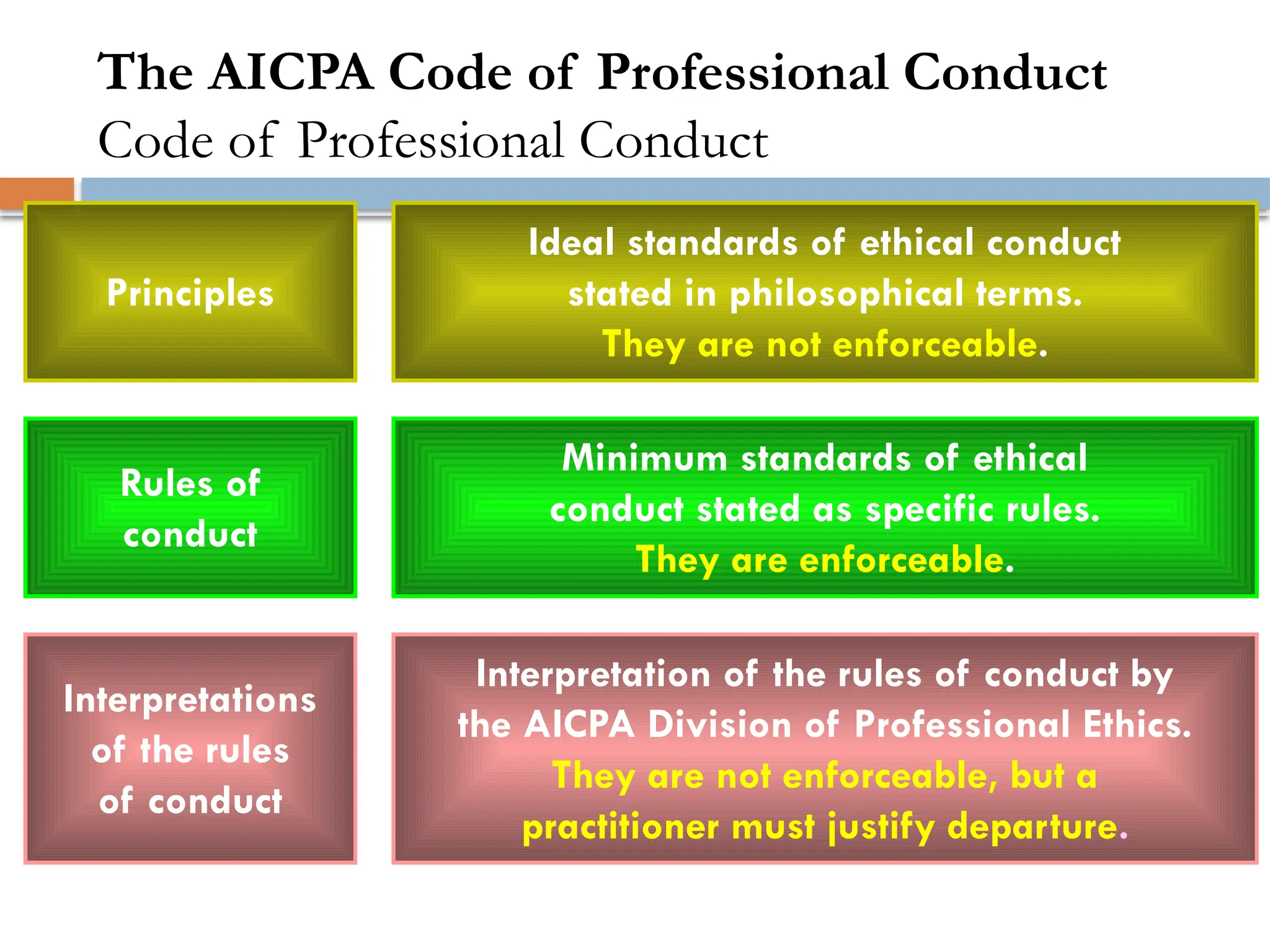

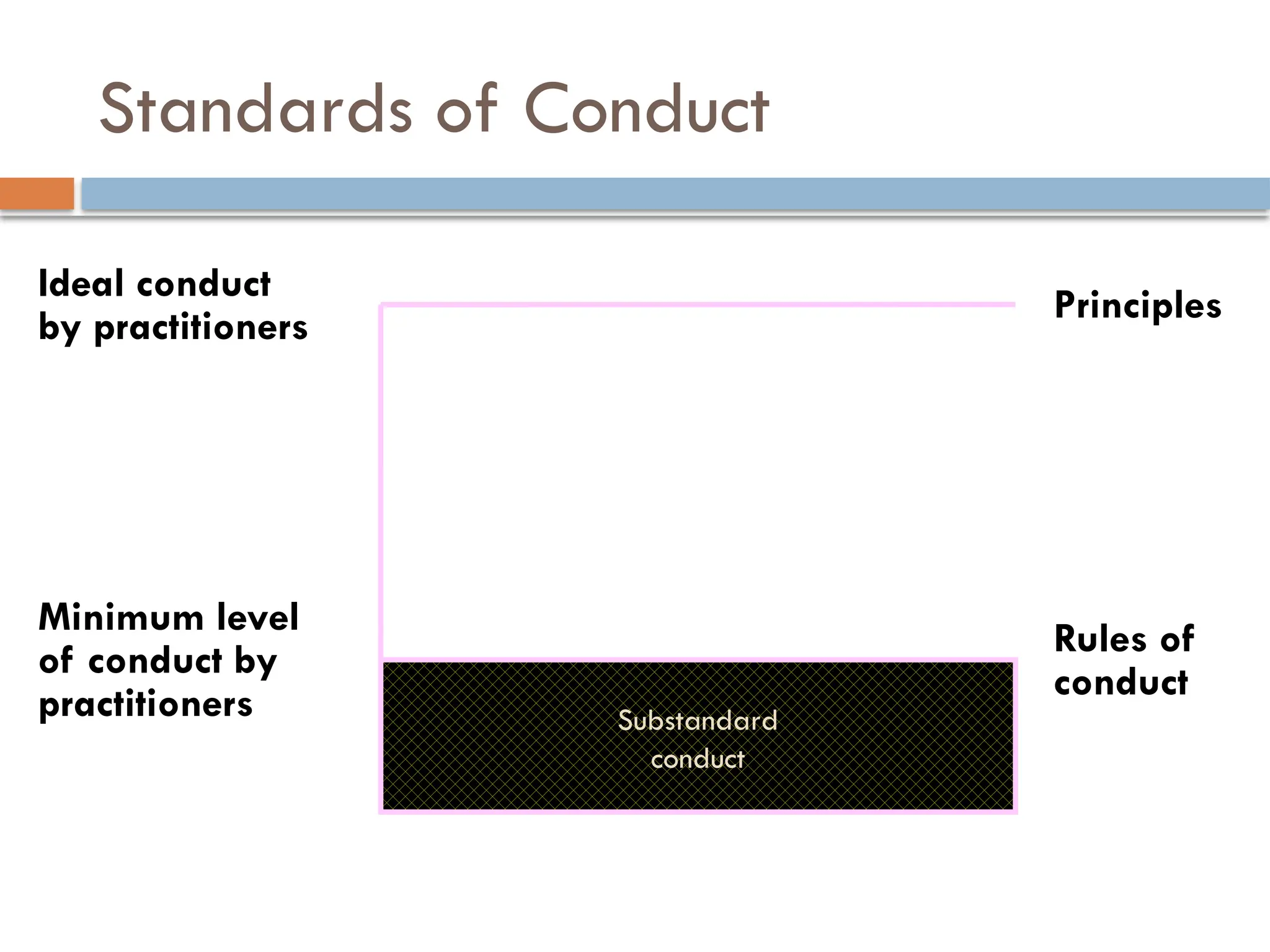

The AICPA Codeof Professional Conduct

Code of Professional Conduct

Principles

Ideal standards of ethical conduct

stated in philosophical terms.

They are not enforceable.

Rules of

conduct

Minimum standards of ethical

conduct stated as specific rules.

They are enforceable.

Interpretations

of the rules

of conduct

Interpretation of the rules of conduct by

the AICPA Division of Professional Ethics.

They are not enforceable, but a

practitioner must justify departure.

39.

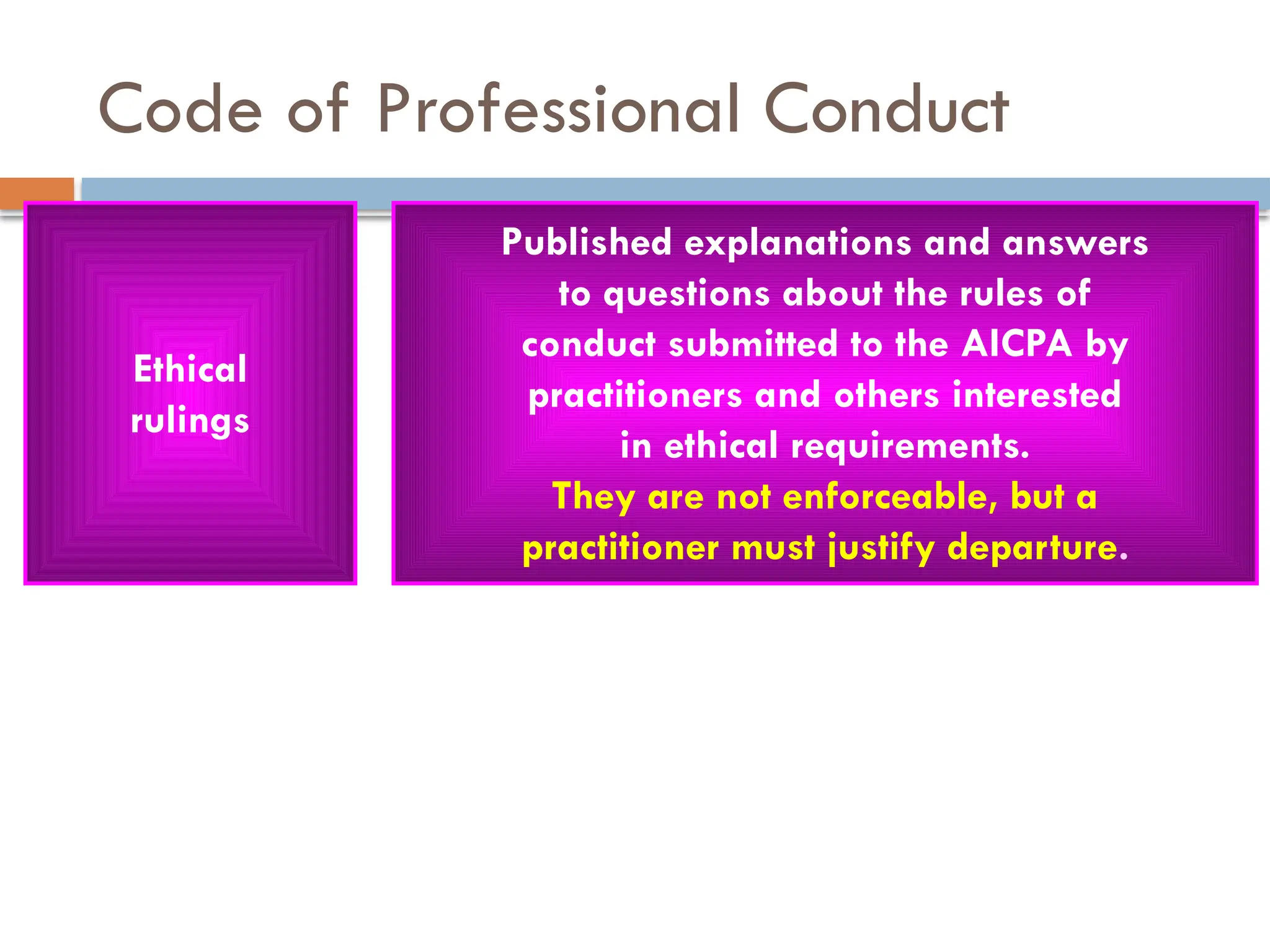

Code of ProfessionalConduct

Ethical

rulings

Published explanations and answers

to questions about the rules of

conduct submitted to the AICPA by

practitioners and others interested

in ethical requirements.

They are not enforceable, but a

practitioner must justify departure.

40.

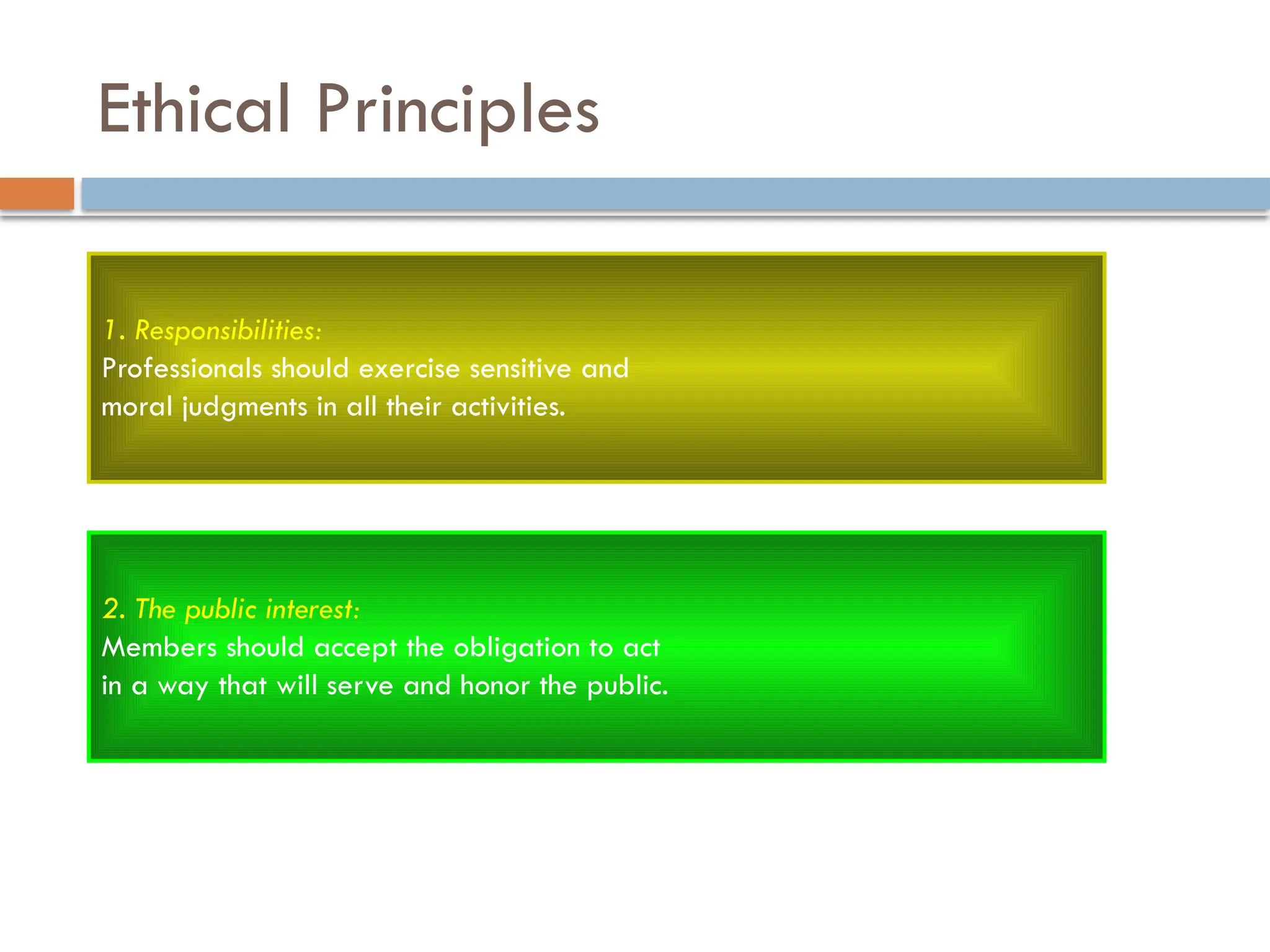

Ethical Principles

1. Responsibilities:

Professionalsshould exercise sensitive and

moral judgments in all their activities.

2. The public interest:

Members should accept the obligation to act

in a way that will serve and honor the public.

41.

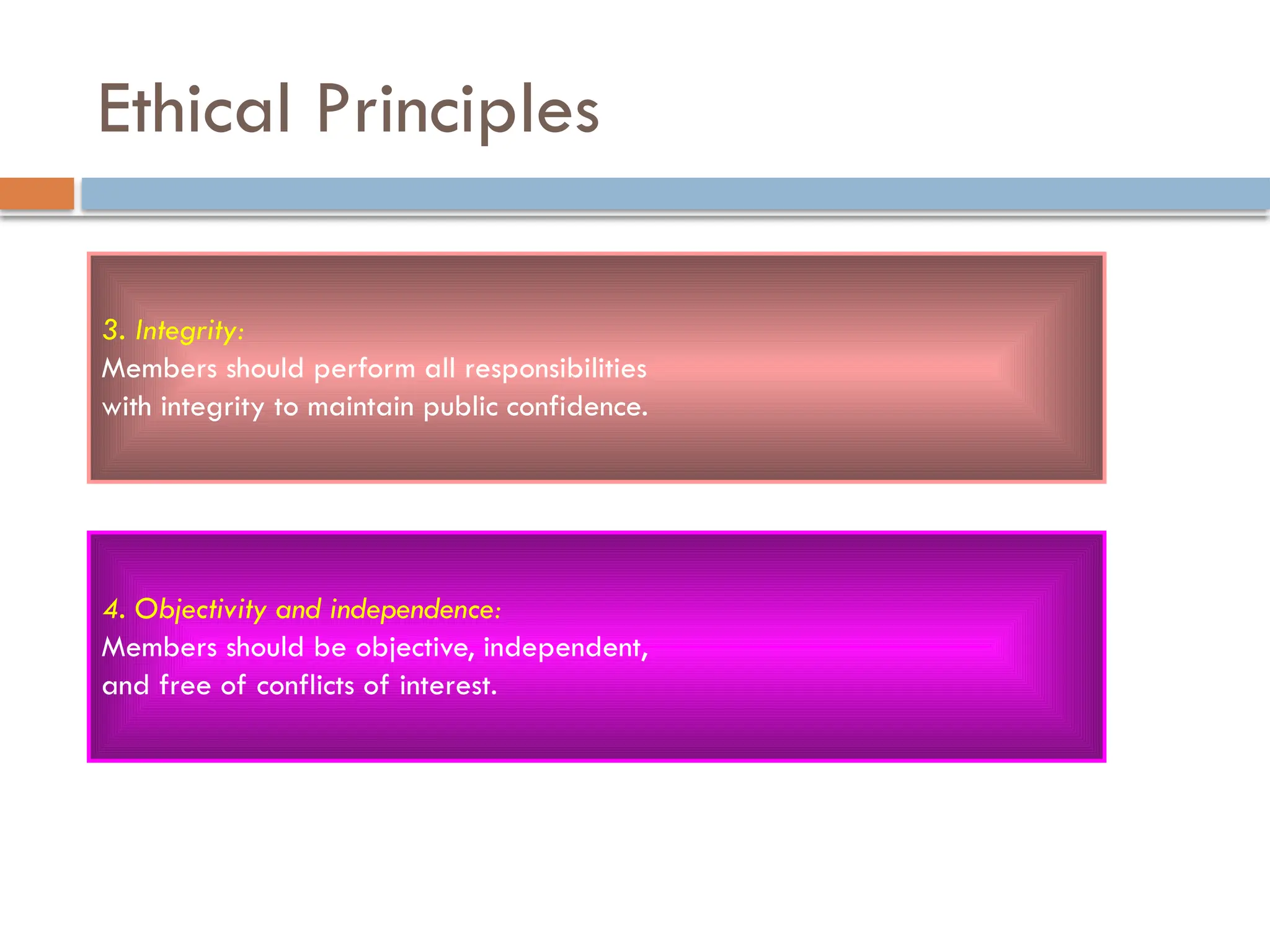

Ethical Principles

3. Integrity:

Membersshould perform all responsibilities

with integrity to maintain public confidence.

4. Objectivity and independence:

Members should be objective, independent,

and free of conflicts of interest.

42.

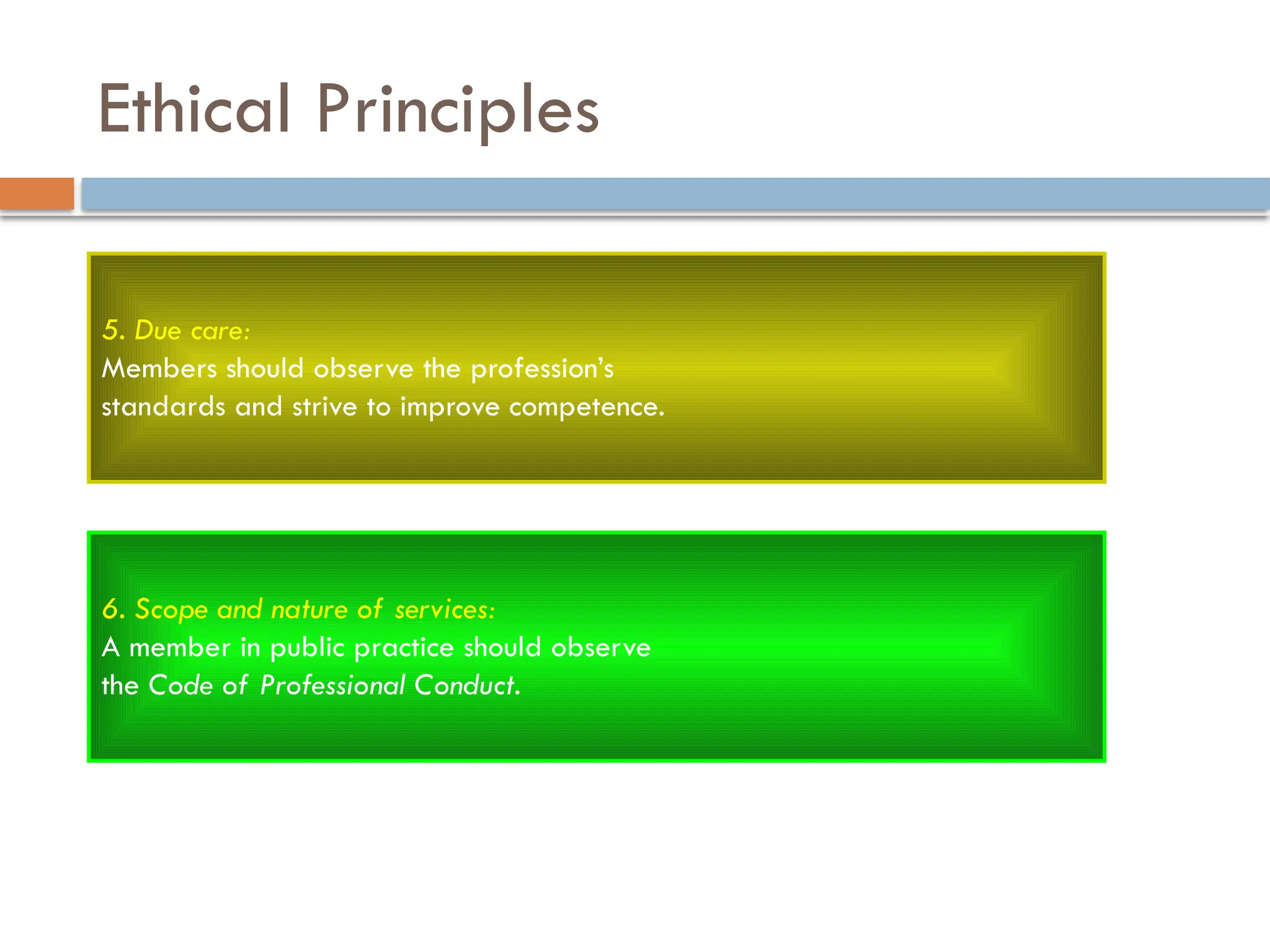

Ethical Principles

5. Duecare:

Members should observe the profession’s

standards and strive to improve competence.

6. Scope and nature of services:

A member in public practice should observe

the Code of Professional Conduct.

Auditing profession

The AICPAcode of professional ethics considers the following to be

followed by auditors in the conduct of professional relations with

others.

1. Integrity: An auditor should be straight forward, honest and

sincere in his approach to his professional work. By integrity it means

honorable, upright, courageous and not being two faced.

2. Objectivity: An auditor should be fair and should not allow bias to

override his objectivity when reporting his opinion. He should

maintain an impartial attitude.

He obtains the evidence needed to form an opinion and his

opinion is based on that evidence alone. He is not subjective in

forming his opinion.

45.

3. Confidentiality: Usuallyauditors have unrestricted access,

even to the confidential documents, of the client while they

are conducting an audit.

Thus an auditor should respect the confidentiality of the

information acquired in the course of his work and should not

disclose any such information to a third party with out specific

authority or unless there is a legal or professional duty to

disclose.

A member acquiring information in the course of professional

work should neither use nor appear to use that information for

his personal advantage or for the advantage of any third party.

46.

Auditing profession

4. Independence:When in public practice, an auditor

should both be and appear to be free of any interest

which might be regarded, what ever its actual effect,

as being incompatible with integrity and objectivity.

Auditor is independent of management i.e. he is not

under the control or influence of management.

5. Caring for others: Be caring, kind and passionate, be

of service to others; help those in need and avoid

harming others.

47.

Auditing profession

6. Accountability:An auditor should be accountable,

accept responsibility for decisions, setting an

example for others.

7. Due care: This requires competence, and diligence.

Competence is the product of education and

experience, and diligence involves steady, earnest and

energetic application and effort in performing

professional services.

48.

Generally Accepted Auditingstandards

In order to maintain high level of quality work,

auditors need to have some standards in accordance

with which they perform their activities.

This section discusses the authoritative rules for

measuring the quality of audit work.

Standards are authoritative rules for measuring

the quality of performance.

49.

Generally Accepted Auditingstandards

The existence of generally accepted auditing standards

is evidence that auditors are very concerned with the

maintenance of a uniformly high quality of audit work

by all independent public accountants

Auditing standards are general guidelines to aid

auditors in fulfilling their professional

responsibilities in the audit of financial statements.

What are the standards developed for the public

accounting profession?

50.

Generally Accepted Auditingstandards

AICPA has set forth ten generally accepted auditing

standards: These ten auditing standards are classified in

to three major groups as general standards, field

work standards and reporting standards.

1. General standards: The general standards relate to

the personal integrity and professional

qualifications of the auditors.

These standards stress on competence,

independence and due professional care by the

auditor. These standards are:

51.

Generally Accepted Auditingstandards

A) Technical Training and proficiency: An audit

examination should be performed by a person or

persons having adequate technical training and

proficiency as an auditor.

This requirement is usually interpreted to mean college

or university education in accounting and auditing,

substantial public accounting experience, ability to use

procedures suitable for computer based systems and

technical knowledge of the industry being audited.

52.

Generally Accepted Auditingstandards

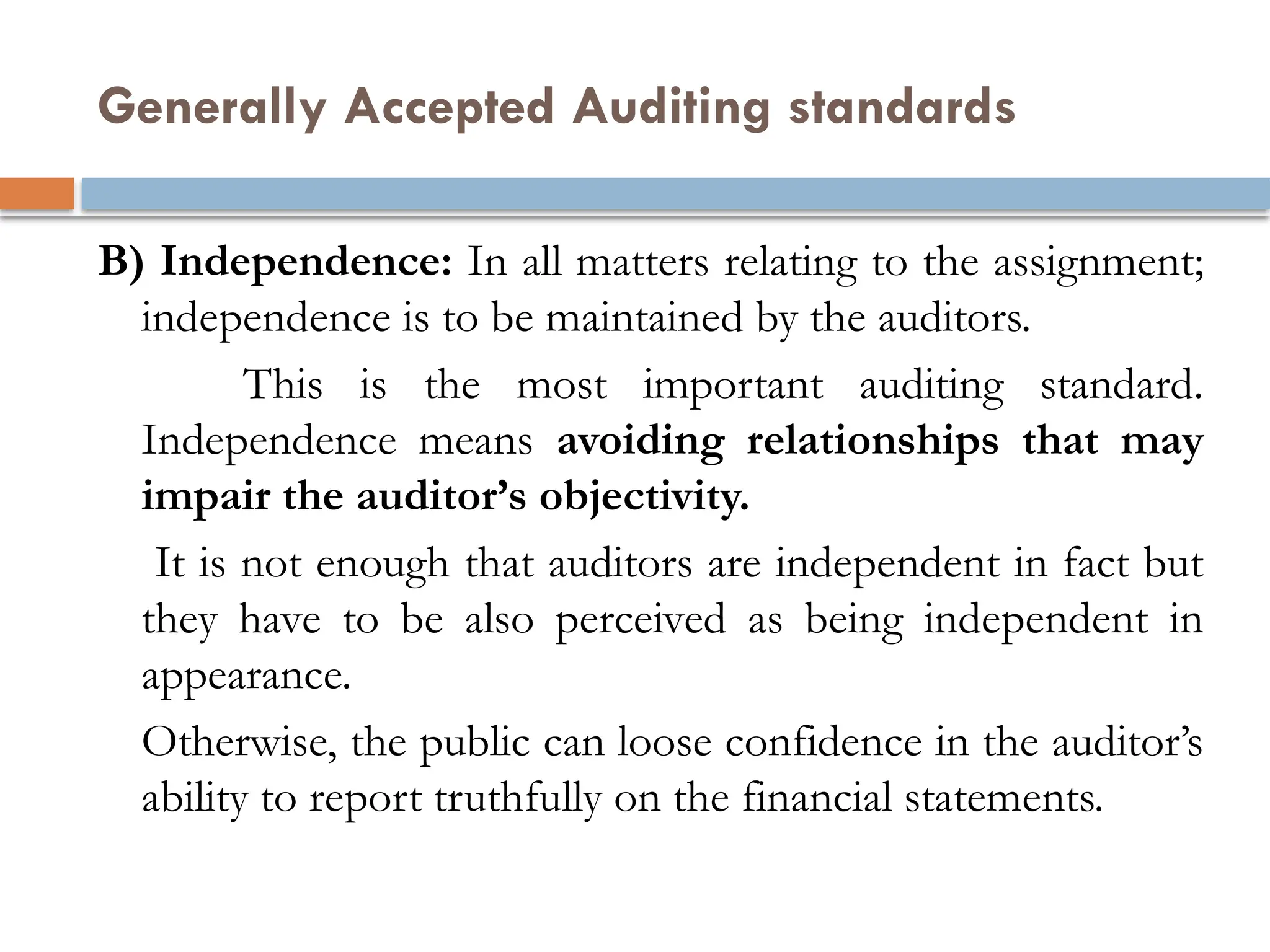

B) Independence: In all matters relating to the assignment;

independence is to be maintained by the auditors.

This is the most important auditing standard.

Independence means avoiding relationships that may

impair the auditor’s objectivity.

It is not enough that auditors are independent in fact but

they have to be also perceived as being independent in

appearance.

Otherwise, the public can loose confidence in the auditor’s

ability to report truthfully on the financial statements.

53.

Generally Accepted Auditingstandards

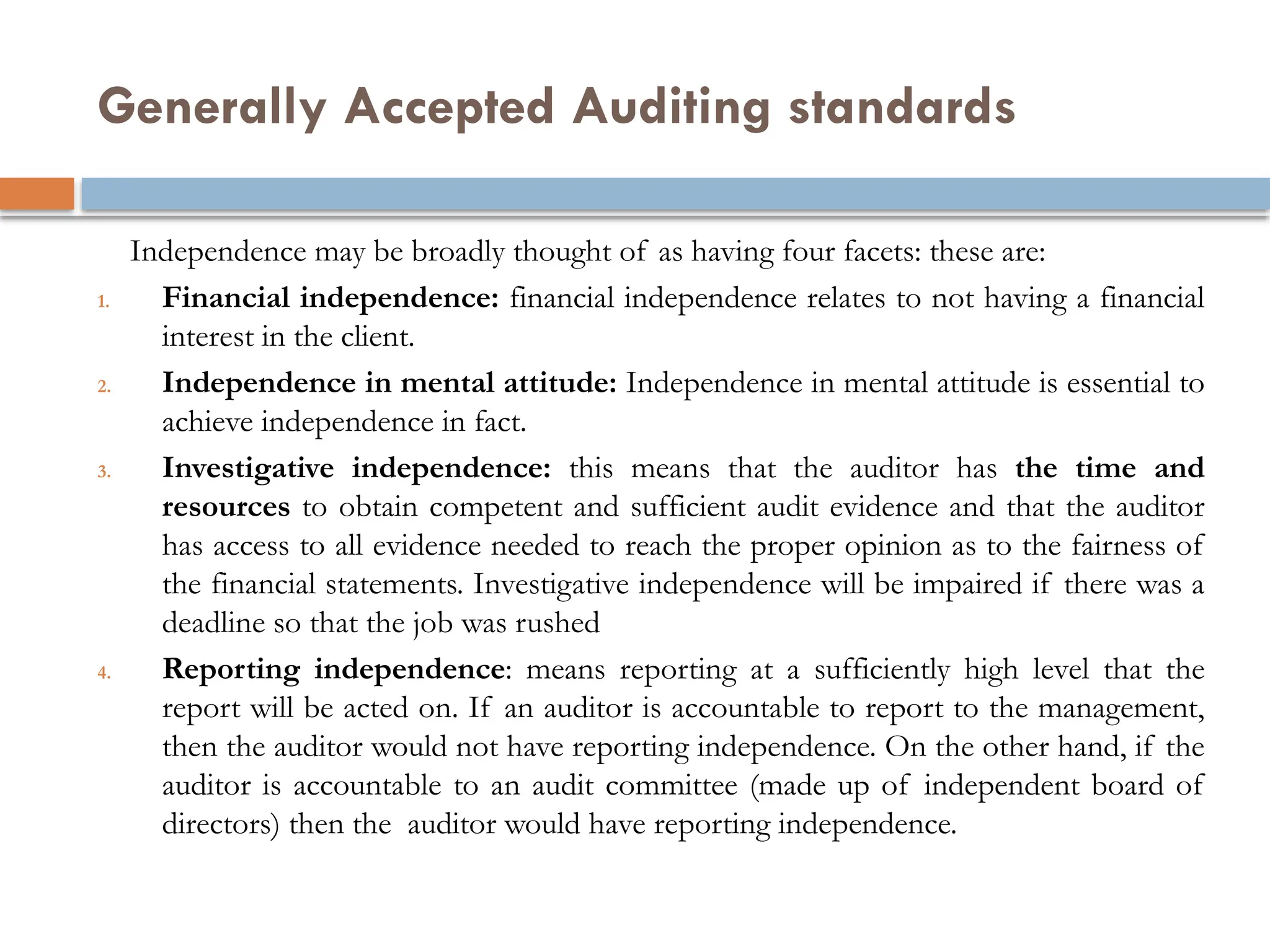

Independence may be broadly thought of as having four facets: these are:

1. Financial independence: financial independence relates to not having a financial

interest in the client.

2. Independence in mental attitude: Independence in mental attitude is essential to

achieve independence in fact.

3. Investigative independence: this means that the auditor has the time and

resources to obtain competent and sufficient audit evidence and that the auditor

has access to all evidence needed to reach the proper opinion as to the fairness of

the financial statements. Investigative independence will be impaired if there was a

deadline so that the job was rushed

4. Reporting independence: means reporting at a sufficiently high level that the

report will be acted on. If an auditor is accountable to report to the management,

then the auditor would not have reporting independence. On the other hand, if the

auditor is accountable to an audit committee (made up of independent board of

directors) then the auditor would have reporting independence.

54.

Generally Accepted Auditingstandards

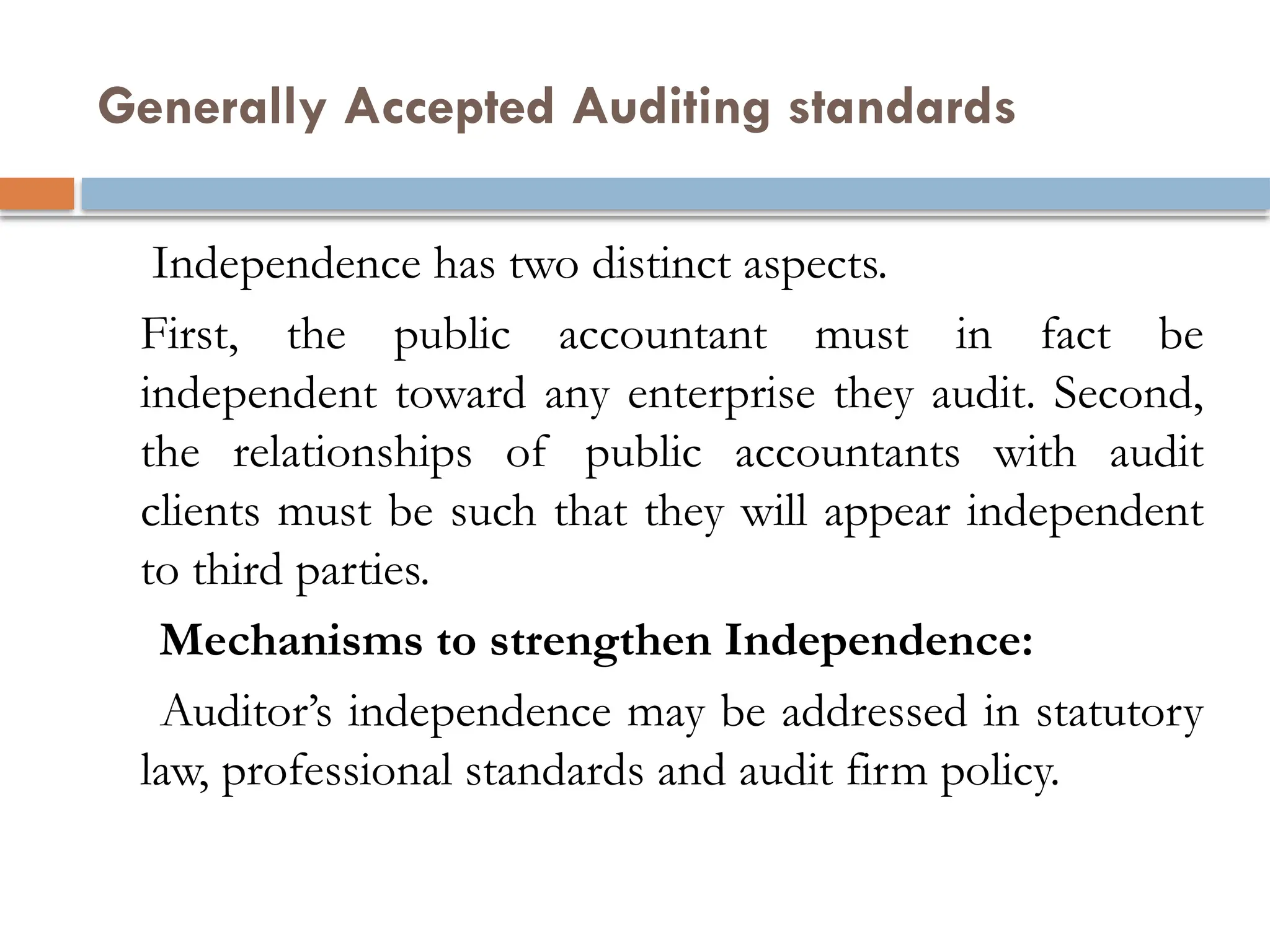

Independence has two distinct aspects.

First, the public accountant must in fact be

independent toward any enterprise they audit. Second,

the relationships of public accountants with audit

clients must be such that they will appear independent

to third parties.

Mechanisms to strengthen Independence:

Auditor’s independence may be addressed in statutory

law, professional standards and audit firm policy.

55.

Generally Accepted Auditingstandards

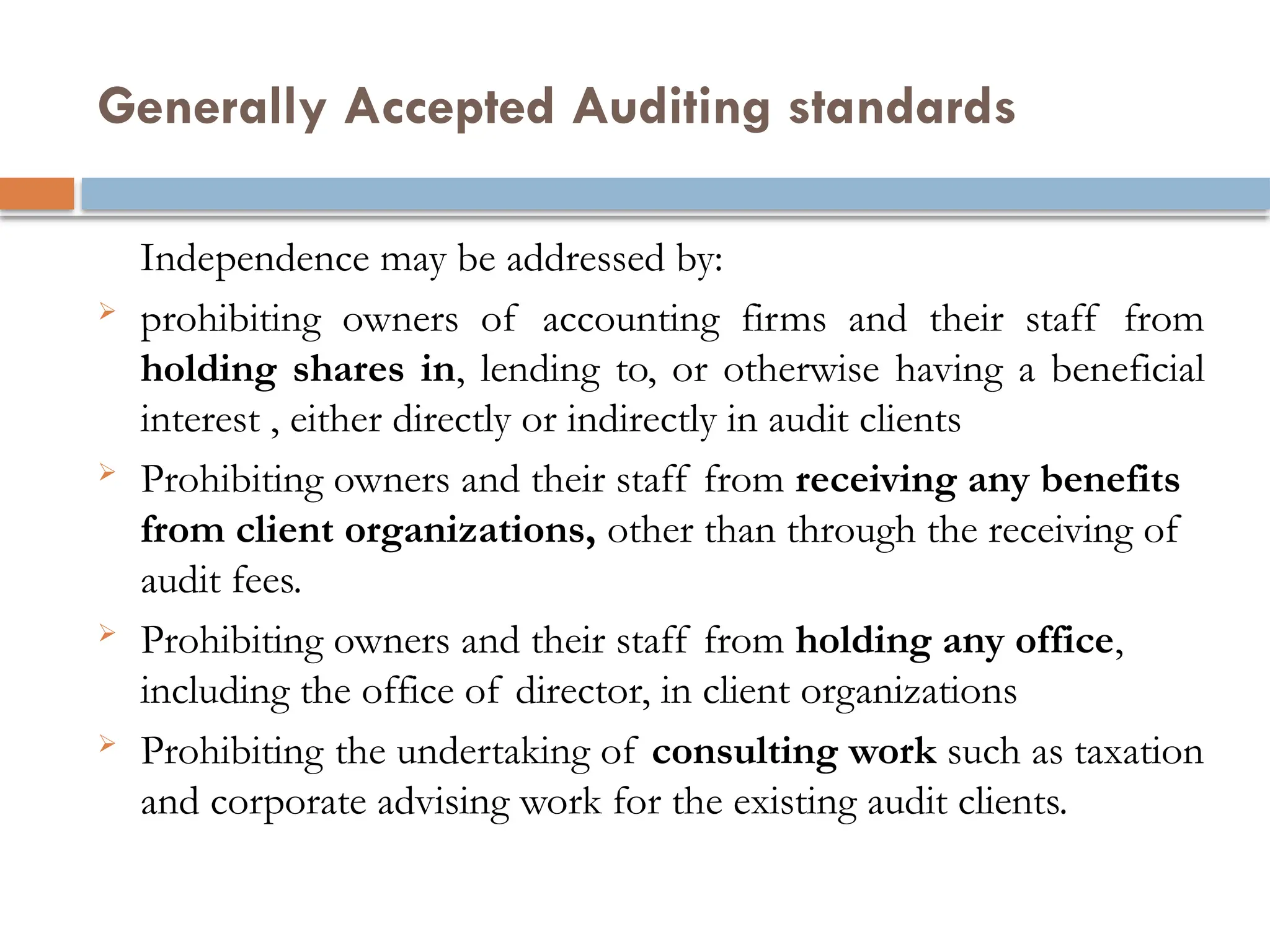

Independence may be addressed by:

prohibiting owners of accounting firms and their staff from

holding shares in, lending to, or otherwise having a beneficial

interest , either directly or indirectly in audit clients

Prohibiting owners and their staff from receiving any benefits

from client organizations, other than through the receiving of

audit fees.

Prohibiting owners and their staff from holding any office,

including the office of director, in client organizations

Prohibiting the undertaking of consulting work such as taxation

and corporate advising work for the existing audit clients.

56.

Generally Accepted Auditingstandards

C) Due professional care: The third general standard

requires due care in the performance of all aspects of

auditing. Simply stated the auditor is professionally responsible

for fulfilling his /her duties diligently and carefully.

Due care includes consideration of the completeness

of the working papers, the sufficiency of the audit

evidence, and the appropriateness of the audit report.

As a professional, the auditor must avoid negligence

and bad faith. This standard requires auditors to carry

out their work in an alert and diligent manner

57.

Generally Accepted Auditingstandards

2- Field work standards: The three standards of field work

relate to accumulation and evaluating evidence sufficient

for the auditors to express an opinion on the financial

statements.

Auditors cannot effectively satisfy the general standards

requiring due professional care if they have not also satisfied

the standards of field work.

The field work standard involves

adequate planning,

sufficient understanding of internal control and

sufficient and competent evidence.

58.

Generally Accepted Auditingstandards

A) Sufficient understanding of internal control: One of the

most widely accepted concepts in the theory and practice of

auditing is the importance of the client’s internal control

structure to generate reliable financial information.

An excellent internal control structure provides strong

assurance that the client’s records are dependable and

that its assets are protected.

A proper understanding of the internal control helps the

auditor to determine the appropriate amount and quality

of evidence.

Thus, the auditor’s assessment of internal control has great

impact on the length and nature of the audit process.

59.

Generally Accepted Auditingstandards

B) Adequate planning and supervision: The first standard

of field work deals with ascertaining that the engagement is

sufficiently planned to ensure an adequate audit and

adequate supervision of assistants.

Proper planning can help to effectively detect material

misstatements on the financial statements and to

complete the audit engagement in a reasonable

amount of time.

Supervision is essential in auditing because a considerable

portion of the field work is done by less experienced staff

members.

60.

Generally Accepted Auditingstandards

C) Sufficient and competent evidence: The third standard

of fieldwork requires that the auditors should gather

sufficient and competent evidence to have a basis for

expressing an opinion on the financial statements.

The decision as to how much evidence to accumulate in a

given set of circumstances requires professional judgment.

The term sufficient refers to the quantity of

information to be gathered while competency refers to

the quality of evidences, as some forms of evidence

are stronger and more convincing than others.

61.

Generally Accepted Auditingstandards

3-Standards of Reporting: The ultimate objective of

independent auditors is to report on the findings of the

audit.

The reporting is guided by reporting standards of

GAAS.

The standards of reporting deals with

Generally accepted accounting principles (GAAP),

consistency,

adequate disclosure and

report content.

62.

Generally Accepted Auditingstandards

These reporting standards can be explained as follows:

1. The report shall state whether the financial statements are

presented in accordance with GAAPs.

2. The report shall identify those circumstances in which such

principles have not been consistently observed in the current

period in relation to the preceding period.

3. Informative disclosures in the financial statements are to be

regarded as reasonably adequate unless otherwise stated in the

report.

4. The report shall either contain an expression of opinion

regarding the financial statements, taken as a whole, or an

assertion to the effect that an opinion can not be expressed.

63.

When anover all opinion can not be expressed, the

reasons should be stated. In all cases where an

auditor’s name is associated with financial statements,

the report shall contain a clear-cut indication of the

extent of the auditor’s examination and the degree of

responsibility he/she is taking.

64.

Generally Accepted Auditingstandards

Case 1: Assume Mr. Dawud, general manager of AB trading,

applied for a bank loan and was informed by the banker that

audited financial statements of the business must be submitted

before the bank could consider the loan application.

Mr.Dawud agreed with Tomas, CPA, to perform an audit.

Mr. Dawud informed Tomas that audited financial statements

were required by the bank and that the audit must be

completed within two weeks and Mr. Dawud promised to pay

Tomas a fixed fee plus a bonus if the audit is completed with

in two weeks and the bank approved the loan. Tomas, CPA,

agreed and accepted the engagement.

65.

Generally Accepted Auditingstandards

The CPA, Tomas, hired two fresh accounting graduates to

conduct the audit and spent several hours telling them exactly

what to do and he told them not to spend time reviewing

internal control but instead, to concentrate on proving the

mathematical accuracy of the ledger accounts and

summarizing the data in the accounting records that support

the company’s financial statements. The audit was completed

with in two weeks and Tomas issued audit report.

Instruction: Exhaustively identify the auditing principles that

were violated By Tomas and support your answer with

justification.

66.

Audit reports

The auditreport is the final step of the audit process.

The financial statements on which you prepare an audit

report are the balance sheet, the income statement, the

statement of retained earnings and the statements of

cash flow.

The auditing profession recognizes the need for

uniformity in reporting as a means of avoiding

confusion.

To avoid confusion and misrepresentation of an audit

report there should be uniformity in reporting.

67.

Audit reports

The AICPAhas developed the following reporting standards.

1. The report shall state whether the financial statements are presented in

conformity with Generally Accepted Accounting Principles.

2. The report shall state whether or not such principles have been consistently

followed or not.

3. Informative disclosures in the financial statements are to be regarded as

reasonably adequate unless otherwise stated in the report.

4. The report shall contain either an expression of an opinion regarding the

financial statements taken as a whole, or an assertion to the effect that an

opinion cannot be expressed.

When an overall opinion cannot be expressed, the reasons should be stated. In

all cases where an auditor’s name is associated with the financial statements, the

report should contain a clear-cut indication of the character of the auditor’s

examination, if any, and the degree of responsibility he/she is taking.

68.

Audit reports

Theprofession recognizes the need for uniformity

in reporting as a means of avoiding confusion.

The professional standards have defined and

enumerated the types of audit reports that should be

included with the financial statements.

The wording of audit reports is reasonably

uniform, but different audit reports are

appropriate for different circumstances.

69.

Components of auditreport

Auditors issue different types of reports based on their

findings. Later, in this chapter, we shall see the types of

reports issued by auditors.

One of the reports auditors issue is the standard unqualified

audit report. The standard audit report (Unqualified)

contains three paragraphs, namely the introductory

paragraph, the scope paragraph, and the opinion

paragraph.

Each part of the auditor report is significant in terms of the

information conveyed to the user and the responsibility

assumed by the auditor.

70.

Components of auditreport

standard unqualified report has seven parts.

Report Title: The auditing standard requires that the report be

titled and that the title include the word Independent. The

appropriate title would be “Independent auditor’s report, or

Report of independent auditors.” The requirement that the title

include the word “independent” is intended to convey to users

that the audit was unbiased in all aspects of the engagement.

Address: The report is usually addressed to the company, its

stockholders or the board of directors or combinations of

these. If you are appointed by the stockholders at the annual

meeting, you have to write the audit report addressing to them.

71.

Components of auditreport

Introductory paragraph: This is the first paragraph of the audit

report and it does three things:

It makes the simple statement that the audit firm has done an audit.

This is intended to distinguish the report from a compilation or

review report.

It lists the financial statements that were audited, including the

balance sheet, income statement, statement of retained earnings

and cash flow statements.

The introductory paragraph states that the statements are the

responsibility of management and that the auditor’s responsibility is

to express an opinion on the financial statements based on an audit.

72.

Components of auditreport

Scope paragraph: The scope paragraph describes what

the auditor has performed during the audit.

Specifically, it states whether the audit was conducted in

accordance with Generally Accepted Auditing Standards

(GAAS). It also states that the GAAS requirement that an

audit be planned to provide reasonable assurance that the

financial statements are free of material misstatement.

The scope paragraph states that the audit is designed to

obtain reasonable assurance about whether the statements

are free of material misstatements.

73.

Components of auditreport

The inclusion of the word “material” conveys that auditors are

responsible only to search for significant misstatements; not

minor errors that do not affect users’ decisions.

The use of the term “reasonable assurance” is intended to

indicate that an audit cannot be expected to eliminate completely

the possibility that a material error or irregularity will exist in the

financial statements. In other words, an audit provides a high

level of assurance, but it is not a guarantee.

The scope paragraph also discusses the audit evidence

accumulated and states that the auditor believes the evidence

accumulated was appropriate for the circumstances to express the

opinion presented.

The word test-basis indicates that sampling was used rather than

an audit of every transaction and amount on the statements.

74.

Components of auditreport

Opinion Paragraph: The final paragraph in the standard report

states the auditor’s conclusions based on the results of the audit

examination.

This paragraph contains the auditor’s opinion on whether the financial

statements are in conformity with GAAP.

Management is responsible for preparing the financial statements. The

responsibility of the auditor is to audit and express an opinion on

their fairness. This paragraph describes the auditor’s findings. These

findings are expressed in terms of whether the financial statements are

presented in accordance with generally accepted accounting principles.

The audit report must contain either an expression of opinion or

an assertion to the effect that an opinion can not be rendered

and the reasons for this.

75.

Components of auditreport

Name of the audit firm and signature: The name and the

signature identify the audit firm or practitioner that has

performed the audit. Typically, the firm’s name is used, since

the entire audit firm has the legal and professional

responsibility to make certain the quality of the audit meets

professional standards.

Date of audit report: The appropriate date of the audit

report is the one on which the field work has been completed.

This date is important because it represents the time limit on

the auditors’ responsibility. The auditor does not have any

responsibility to make any enquiries after this date.

76.

Audit reports

Types ofaudit report: There are four types of audit

reports that might be issued by the auditors.

These are:

1. An unqualified opinion

2. Qualified opinion

3. An adverse opinion

4. Disclaimer opinion

77.

Audit reports

TheUnqualified report: The most common type of

audit report is the standard unqualified audit report.

This report represents a “clean bill of health” and

may be issued when

there are no material departures from generally

accepted accounting principles,

no significant scope limitations preventing the

gathering of necessary evidence and

when no conditions requiring explanatory language

exist.

78.

Audit reports

The unqualifiedreport is issued when the following conditions have been met:

All statements- balance sheet, income statement, statement of retained

earnings and cash flow statements are included in the audited financial

statements

When standards of auditing are applied in all respects of the engagement.

When sufficient evidence has been accumulated and the auditor has

conducted the audit in a manner that enables him to conclude that three

standards of field work have been met.

The financial statements are presented in accordance with generally

accepted accounting principles. This also means that the adequate

disclosures have been included in the footnotes and other parts of the

financial statements.

There are no circumstances requiring the addition of an explanatory

paragraph or modification of the wording of the report.

Audit reports

Qualified opinion:This type of opinion is still a positive

opinion and may result from limitations on the scope of the

audit or failure to follow generally accepted accounting

principles.

Auditors may issue this type of opinion when:

They do not agree with the accounting principles used in

preparing financial statements or when they believe that the

disclosures in the financial statements are inadequate.

A change in accounting principles is not applied properly as per

GAAP and is not adequately disclosed in the financial statements

There are limitations on scope of examination

There is major uncertainty affecting a client’s business.

81.

Audit reports

Ingeneral qualified opinion is issued when the auditors’

examination is restricted as to its scope or the financial

statements depart from generally accepted accounting principles.

A qualified opinion is still a positive opinion; it asserts that the

presentation in the financial statements, viewed as a whole is fair.

The qualified opinion has a separate explanatory paragraph

before the opinion paragraph disclosing the reasons for the

qualification.

When ever the auditor issues a qualified report, he/she must use

the term except for in the opinion paragraph. The implication is

that the auditor is satisfied that the overall financial statements

are fairly stated except for a particular aspect of them

Audit reports

Adverse opinion:this is a negative opinion, asserting that the

financial statements are not fairly presented.

It is issued when the exceptions to the presentations in the

financial statements are so significant that a qualified opinion

would be an inadequate warning to the users of those

statements.

This is a stronger form of except-for opinion – the disagreement

is so material that the financial statements as a whole are

misleading.

This type of statement is used only when the auditor believes the

overall financial statements are so materially or extremely misstated or

misleading that they do not present fairly the financial position or

results of operations and cash flows in conformity with generally

accepted accounting principles.

84.

Audit reports

Theadverse opinion report can arise only when the auditor has the

knowledge, after adequate and satisfactory investigation, of the

absence of conformity.

That is when the auditors express an adverse opinion; they must

have accumulated sufficient appropriate evidence to support their

unfavorable opinion.

Presumably creditors and stockholders would not provide debt or

equity capital to the client if the auditor issues adverse opinion to

the financial statements of the client.

Thus, the client usually will make whatever changes in the financial

statements that the auditors require in order to avoid receiving an

adverse opinion.

85.

Audit reports

Theadverse opinion like the qualified opinion has a

separate explanatory paragraph, before the opinion

paragraph to state the reasons for issuing an adverse

opinion and the principal effect of the adverse

opinion on the client’s financial position and

operating results.

In the opinion paragraph of adverse opinion the

auditors use the negative word “do not present

fairly”.

Audit reports

DisclaimerOpinion: This opinion is also called denial opinion.

This type of audit opinion is issued whenever the auditor has been

unable to satisfy him self or her self that the overall financial

statements are fairly presented.

The necessity for disclaiming an opinion may arise under the

following conditions:

If there has been a severe scope limitation that prevents the

auditor from obtaining sufficient and competent audit evidence;

If the auditor cannot satisfy him self or herself by applying other

procedures;

If the effect of the scope limitation is so significant that the auditor

can not form an opinion as to the fairness of the financial

statements.

88.

Audit reports

Eitherof these situations prevents the auditor from expressing an opinion on

the financial statements as a whole. A very significant scope limitation may be

caused by the client or by the timing of the auditors’ appointment and their

audit work or by the factors beyond the control of the client or the auditors,

rather than by restrictions imposed by the client.

A disclaimer is distinguished from an adverse opinion in that it can arise only

from a lack of knowledge by the auditor, where as to express an adverse

opinion the auditor must have knowledge that the financial statements are not

fairly stated.

When the auditor expresses a disclaimer of opinion, he/she has to make sure

that the following conditions are met:

An introductory paragraph is modified

The scope paragraph is omitted-since the auditor does not undertake auditing.

An explanatory paragraph is included after introductory paragraph

A third paragraph contains a denial of opinion.

89.

Discussion

1. Auditing hasbeen claimed by many as a

profession which is more responsible to the public

than any other professions. Describe the elements

of a profession and explain why auditing is more

responsible to the public

2. List out the Auditing standards governing auditors

(Make a group of four, discuss and present the

results of your group discussion to the class

(Time allowed for discussion 10 min.

![Brennan, Niamh [2003] Accounting in crisis: A story of auditing, accounting, ...](https://cdn.slidesharecdn.com/ss_thumbnails/0414brennanaccountingincrisisastoryofauditingaccountingcorporategovernanceandmarketfailures-121116102706-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)