Download to read offline

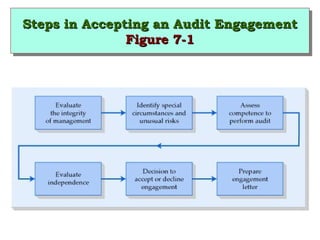

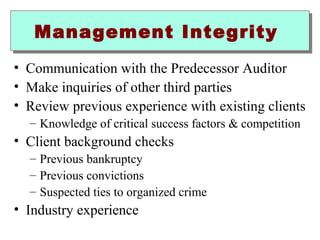

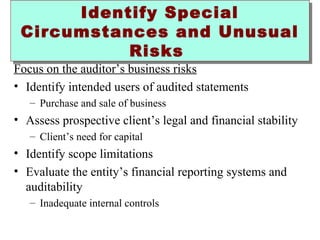

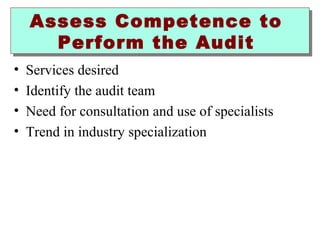

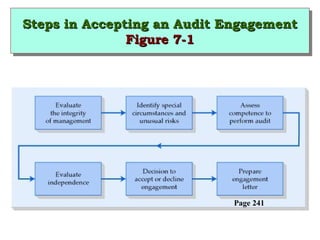

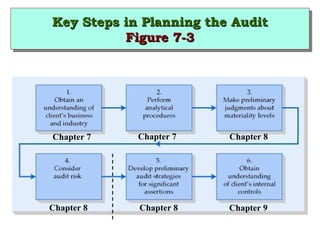

This chapter discusses accepting audit engagements and planning audits. It covers the key steps in client acceptance, which include evaluating management integrity, identifying special risks, assessing competence to perform the audit, and evaluating independence. Planning the audit involves understanding the client's business, industry, and business cycle. Analytical procedures are used in planning to help identify areas of risk, and involve developing expectations, performing calculations, and investigating differences.