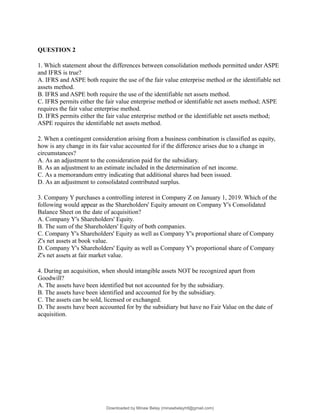

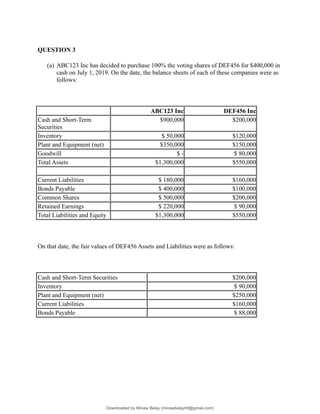

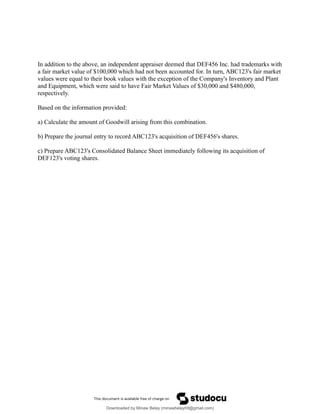

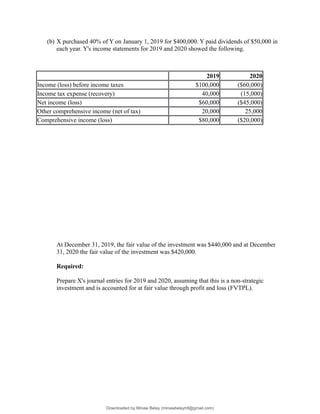

This document contains an exam for an advanced financial accounting course. It includes 3 questions assessing understanding of consolidation methods, business combinations, and accounting for investments. Question 1 has 6 parts related to applying consolidation methods to a sample business acquisition. Question 2 contains 5 multiple choice questions about consolidation standards. Question 3 has two parts: the first asks to calculate goodwill and prepare consolidation journal entries and balance sheet for a business purchase, and the second provides financial information for an investment and asks to prepare the relevant journal entries.