Ch 7 -3

“Thegreatest strategy is doomed if it’s

implemented badly.”

– Bernard Reimann

4.

Ch 7 -4

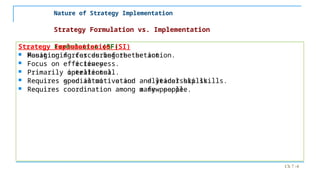

StrategyFormulation vs. Implementation

Strategy Formulation (SF)

Positioning forces before the action.

Focus on effectiveness.

Primarily intellectual.

Requires good intuitive and analytical skills.

Requires coordination among a few people.

Strategy Implementation (SI)

Managing forces during the action.

Focus on efficiency.

Primarily operational.

Requires special motivation and leadership skills.

Requires coordination among many people.

Nature of Strategy Implementation

5.

Ch 7 -5

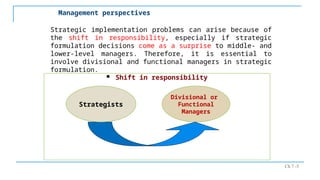

Shift in responsibility

Management perspectives

Strategic implementation problems can arise because of

the shift in responsibility, especially if strategic

formulation decisions come as a surprise to middle- and

lower-level managers. Therefore, it is essential to

involve divisional and functional managers in strategic

formulation.

Divisional or

Functional

Managers

Strategists

6.

Ch 7 -6

ManagementIssues Central to Strategy Implementation

Establish annual

objectives

Devise policies

Allocate resources

Alter existing

organizational structure

Restructure & reengineer

Revise reward &

incentive plans

Minimize resistance to

change

Match managers to strategy

Develop a strategy-

supportive culture

Adapt

production/operations

processes

Develop an effective human

resources function

Downsize & furlough as

needed

Link performance & pay to

strategies

Ch 7 -8

Purposeof Annual Objectives

Basis for resource allocation;

Mechanism for management evaluation;

Major instrument for monitoring progress

toward achieving long-term objectives;

Establish priorities (organizational, divisional,

and departmental);

Guidelines for action, directing and channeling

efforts and activities of organization members;

They serve as standards of performance.

Ch 7 -13

ResourceAllocation

1. Financial resources

2. Physical resources

3. Human resources

4. Technological resources

Strategic management itself is sometimes referred to as a “resource

allocation process.”

14.

Ch 7 -14

ManagingConflict

Conflict – a disagreement between two or more

parties. Interdependency of objectives and

competition for limited resources can cause

conflict.

Conflict not always “bad”.

Lack of conflict may signal apathy.

Can energize opposing groups to action.

May help managers identify problems.

15.

Ch 7 -15

MATCHINGSTRUCTURE WITH STRATEGY

Changes in strategy often require changes in the way an

organization is structured because: (1) structure largely

dictates how objectives and policies will be established (e.g.,

objectives and policies established under a geographic

organizational structure are couched in geographic terms) and

(2) structure dictates how resources will be allocated (e.g., if an

organization’s structure is based on customer groups, then

resources will be allocated in that manner).

Structure should be designed to facilitate the strategic pursuit

of a firm and, therefore, follow strategy.

When a firm changes its strategy, the existing organizational

structure may become ineffective. For example, new strategies

to reduce payroll costs may require a change in span of control.

16.

Ch 7 -16

BasicForms of Structure

Functional Structure (centralized)

Divisional Structure (decentralized)

Strategic Business Unit Structure (SBU)

Matrix Structure

17.

Ch 7 -17

Restructuring

Restructuring - reducing the size of an

organization. Also called:

Downsizing

Rightsizing

Delayering

These methods involve, respectively, reducing the

number of employees, number of divisions, and

number of hierarchical levels in a firm’s

organizational structure. Reducing the size of an

organization is intended to improve its efficiency

and effectiveness.

18.

Ch 7 -18

Creatinga Strategy-Supportive Culture

1. Formal statements of organizational philosophy

2. Design of physical spaces

3. Deliberate role modeling, teaching, and coaching

4. Explicit reward and status system

5. Stories, legends, myths, and parables

19.

Ch 7 -19

Creatinga Strategy-Supportive Culture

6. What leaders pay attention to

7. Leader reactions to critical incidents and crises

8. Organizational design and structure

9. Organizational systems and procedures

10. Criteria for recruitment, selection, promotion,

leveling off, retirement, and “excommunication” of

people.

20.

Ch 7 -20

Production/OperationsDecision Examples

Plant size

Inventory / Inventory control

Quality control

Cost control

Technological innovation

Ch 8 -24

The best formulated and best implemented

strategies become obsolete as a firm’s

external and internal environments change.

Therefore, it is essential for strategists

to systematically review, evaluate, and

control the execution of strategies.

Strategy Review, Evaluation, and Control

25.

Ch 8 -25

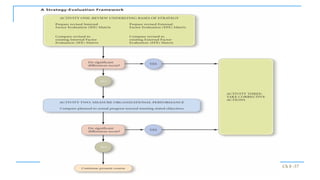

StrategyReview, Evaluation, and Control

Strategy Evaluation

Strategy Evaluation is vital to an organization’s well

being.

Timely evaluations can alert management to potential or

actual problems before a situation becomes critical.

Strategy Evaluation includes three basic activities:

(1) Examining the underlying bases of a firm’s

strategy.

(2) Comparing expected results to actual results.

(3) Taking corrective actions to ensure that

performance conforms to plans.

26.

Ch 8 -26

StrategyReview, Evaluation, and Control

Adequate and timely feedback is the cornerstone of effective

Strategy Evaluation.

Strategy Evaluation is important because organizations face

dynamic environments in which key external and internal factors

can change quickly and dramatically.

Strategy Evaluation is essential to ensure that the stated

objectives of an organization are being achieved.

27.

Ch 8 -27

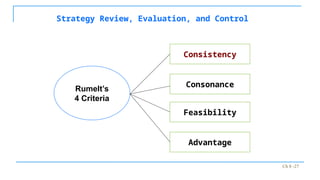

StrategyReview, Evaluation, and Control

Consonance

Consistency

Feasibility

Advantage

Rumelt’s

4 Criteria

28.

Ch 8-28

Strategy Review,Evaluation, and Control

Strategy should not present inconsistent

goals and policies.

Consistency

29.

Ch 8-29

Strategy Review,Evaluation, and Control

Need for strategists to examine sets of

trends, as well as individual trends.

Consonance

30.

Ch 8 -30

StrategyReview, Evaluation, and Control

Neither overtax resources nor create

unsolvable sub-problems.

Feasibility

31.

Ch 8 -31

StrategyReview, Evaluation, and Control

Creation or maintenance of competitive

advantage.

Advantage

32.

Ch 8 -32

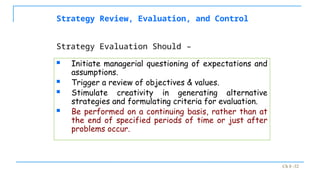

StrategyReview, Evaluation, and Control

Initiate managerial questioning of expectations and

assumptions.

Trigger a review of objectives & values.

Stimulate creativity in generating alternative

strategies and formulating criteria for evaluation.

Be performed on a continuing basis, rather than at

the end of specified periods of time or just after

problems occur.

Strategy Evaluation Should –

33.

Ch 8 -33

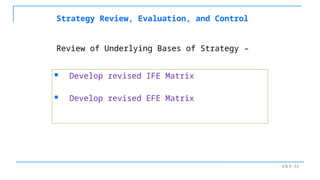

StrategyReview, Evaluation, and Control

Develop revised IFE Matrix

Develop revised EFE Matrix

Review of Underlying Bases of Strategy –

34.

Ch 8 -34

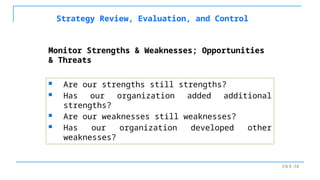

StrategyReview, Evaluation, and Control

Are our strengths still strengths?

Has our organization added additional

strengths?

Are our weaknesses still weaknesses?

Has our organization developed other

weaknesses?

Monitor Strengths & Weaknesses; Opportunities

& Threats

35.

Ch 8 -35

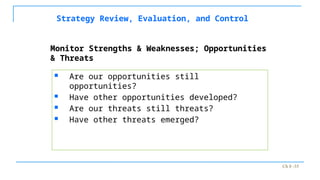

StrategyReview, Evaluation, and Control

Are our opportunities still

opportunities?

Have other opportunities developed?

Are our threats still threats?

Have other threats emerged?

Monitor Strengths & Weaknesses; Opportunities

& Threats

36.

Ch 8 -36

StrategyEvaluation Framework

Note that corrective actions are needed

except when (1) external and internal

factors have not changed significantly and

(2) the firm is making satisfactory

progress toward achieving its objectives.

Ch 8 -38

StrategyReview, Evaluation, and Control

Compare expected to actual results.

Investigate deviations from plan.

Evaluate individual performance.

Examine progress toward stated

objectives.

Measuring Organizational Performance

39.

Ch 8 -39

StrategyReview, Evaluation, and Control

Strategists use financial ratios to:

Compare a firm’s performance over different

time periods.

Compare a firm’s performance to competitors’

performance.

Compare a firm’s performance to industry

averages.

Quantitative Criteria for Strategy

Evaluation

40.

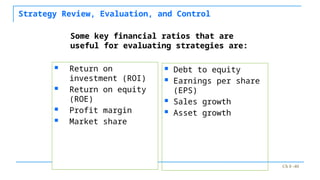

Ch 8 -40

StrategyReview, Evaluation, and Control

Return on

investment (ROI)

Return on equity

(ROE)

Profit margin

Market share

Debt to equity

Earnings per share

(EPS)

Sales growth

Asset growth

Some key financial ratios that are

useful for evaluating strategies are:

41.

Ch 8 -41

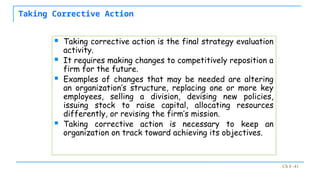

TakingCorrective Action

Taking corrective action is the final strategy evaluation

activity.

It requires making changes to competitively reposition a

firm for the future.

Examples of changes that may be needed are altering

an organization’s structure, replacing one or more key

employees, selling a division, devising new policies,

issuing stock to raise capital, allocating resources

differently, or revising the firm’s mission.

Taking corrective action is necessary to keep an

organization on track toward achieving its objectives.

42.

Ch 8 -42

StrategyReview, Evaluation, and Control

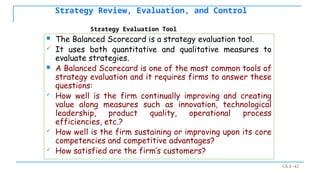

The Balanced Scorecard is a strategy evaluation tool.

It uses both quantitative and qualitative measures to

evaluate strategies.

A Balanced Scorecard is one of the most common tools of

strategy evaluation and it requires firms to answer these

questions:

How well is the firm continually improving and creating

value along measures such as innovation, technological

leadership, product quality, operational process

efficiencies, etc.?

How well is the firm sustaining or improving upon its core

competencies and competitive advantages?

How satisfied are the firm’s customers?

Strategy Evaluation Tool

43.

Ch 8 -43

TheBalanced Scorecard

Note that in this example the firm examines

six key issues in evaluating its strategies:

(1) customers, (2) managers/employees, (3)

operations/processes, (4) community/social

responsibility, (5) business ethics/natural

environment, and (6) financial.

The basic form of a Balanced Scorecard may

differ for different organizations.