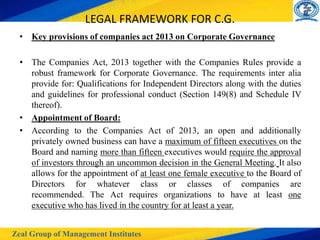

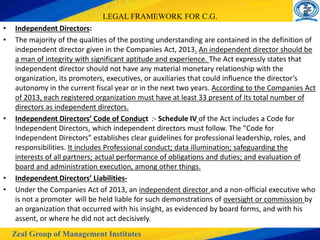

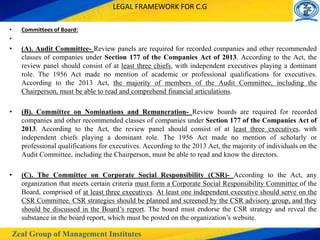

The document discusses the legal framework for corporate governance in India according to the Companies Act 2013. It outlines key provisions regarding board composition and qualifications for directors, requirements for independent directors and committees, related party transactions, and prohibitions on insider trading. It also describes differences in governance requirements for listed versus unlisted companies, with listed companies regulated by SEBI and subject to more stringent laws. Recent amendments to SEBI's LODR regulations aim to strengthen disclosure standards and governance for listed entities.