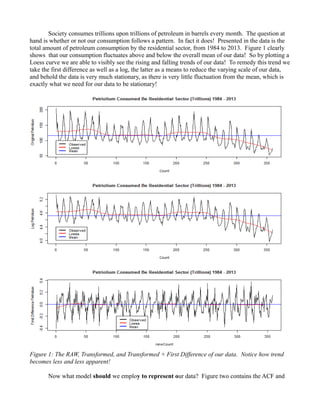

1. Society consumes trillions upon trillions of petroleum in barrels every month. The question at

hand is whether or not our consumption follows a pattern. In fact it does! Presented in the data is the

total amount of petroleum consumption by the residential sector, from 1984 to 2013. Figure 1 clearly

shows that our consumption fluctuates above and below the overall mean of our data! So by plotting a

Loess curve we are able to visibly see the rising and falling trends of our data! To remedy this trend we

take the first difference as well as a log, the latter as a means to reduce the varying scale of our data,

and behold the data is very much stationary, as there is very little fluctuation from the mean, which is

exactly what we need for our data to be stationary!

Now what model should we employ to represent our data? Figure two contains the ACF and

Figure 1: The RAW, Transformed, and Transformed + First Difference of our data. Notice how trend

becomes less and less apparent!

2. the PACF plots of our transformed and differenced data, and quite clearly we can see that neither an

auto regressive model nor would a moving average model be able to represent our model, so we must

use an ARMA model, and because we have taken a first difference we must employ the use of an

ARIMA(q,d,p) model! Using R's forecast package I employ the use of auto.arima() function to

determine our parameters, which come out to be ARIMA(5,1,4).

We now have a model to fit our data to! The next step to see if this model fits very well is to

perform a number of diagnostics to ensure our model is a good fit! First we look at the ACF and PACF

of our residuals, and there happen to significant values at particular lags, which tells me that the 5,1,4

model may not have been the best model to represent our data. Next we look to see if our residuals

fluctuate about a mean of 0, and quite certainly they in fact do. The next question is: are the residuals

normal and independent? The normal plot shows that they are indeed normal, and the Box-Ljung test

gives us a significantly large p-test (p = .94), which implies that our residuals are independent.

Figure 2: The ACF and PACF of our transformed and differenced data, notice that both do not cut off.

Implying that an ARMA model is appropriate! We also have our periodogram of our data! Notice that

a large peak occurs around .833! This is our frequency which relates to a cycle of 1.2 months!

3. However do take notice of the Ljung-Box test plot clearly shows that after two lags our model no

longer shows independent residuals. What does this mean? It implies any lag higher than two may be

of poor representation, in other words our model is only decent at examining two future values. Figure

three represent our conclusions graphically. Our results on the residuals are as follows:

1. Independent for lags up to 2

2. Constant variance

3. Fluctuate about mean

4. Residuals are normal

Our residuals do not represent only white noise, there are other errors being accounted for. So the

question is now then how effective is our model in predicting our future consumption of petroleum?

Using our suggested model, ARIMA(5,1,4) we attempt to predict the last 12 months of our

Figure 3: Our residual lots concerning residual analysis for our model. Notice how our model fails the

Ljung Box test and clearly shows significant values in it's ACF and PACF! This implies our model is

not the BEST!

4. observed data. Figure 4 shows our forecasted values, our observed values, as well as our prediction

bands (our standard error.) Our predicted values are actually quite spot on! Our observed and

forecasted values are well within range of one another and lie within our prediction bands, so our

model, ARIMA(5,1,4) turned out to be a decent fit for representing future values!

Using time series methods we observed that we were able to draw successful predictions to how

much petroleum the residential sector will consume per month! This example shows time series's

effectiveness in predicting the future. However what I must take note of is that our prediction were for

the next year only, not the year afterward or the year after that one. What should be taken with a grain

of salt is that though we can successfully predict the future to a relatively good degree, we are still

unable to account for possibly shocks in the future with the methods presented here. FIGURE clearly

shows how large our room for error is! Nevertheless time series remains to be a powerful tool in

predicting the future based on past observations.

Figure 4: Our predicted values and the observed values. Take note of how well our model actually

predicted the values!

5. Figure 6: Our periodogram of our final model, notice that it still retains the same significant frequency

(.899), which is made even more apparent in it's smoothed counter part!

6. Explicit R Code & Output:

> data <- read.table("Data.txt", header = TRUE)

>

> #Determine if the Series is stationary.

>

> #Plot the original data

> par(mfrow=(c(3,1)))

> Petro <- data$Petro

> Count = (1:359)

>

> plot(Petro~Count, type = "l",main = "Petriolium Consumed Be Residential Sector (Trillions) 1984 -

2013", ylab = "Original Petrolium")

> fitO = loess(Petro~Count, span = .25, family = "gaussian")

> lines(Count,fitO$fitted,col="red")

> abline(h = mean(Petro), col = 'blue')

> legend(0,100, c("Observed", "Loess", "Mean"), lty = c(1,1), lwd=c(2.5,2.5),col = c("black","red",

"blue"))

>

> #Transform the Data

> transData <- log(Petro)

> plot(transData ~ Count, type = "l", main = "Petriolium Consumed Be Residential Sector (Trillions)

1984 - 2013",ylab = "Log Petrolium")

> fitL = loess(transData ~ Count, span = .25, family = "gaussian")

> lines(Count,fitL$fitted,col="red")

> abline(h = mean(transData), col = 'blue')

> legend(0,4.4, c("Observed", "Loess", "Mean"), lty = c(1,1), lwd=c(2.5,2.5),col = c("black","red",

"blue"))

>

> #Take the First difference

> transDif <- diff(transData,differences=1)

> newCount = (1:358)

>

> #Plot the transformed data.

> plot(transDif~newCount, type = "l", main = "Petriolium Consumed Be Residential Sector (Trillions)

1984 - 2013",ylab = "First Difference Petrolium")

> fitD = loess(transDif ~ newCount, span = .25, family = "gaussian")

> lines(newCount,fitD$fitted,col="red")

> abline(h = mean(transDif), col = 'blue')

> legend(100,-.2, c("Observed", "Loess", "Mean"), lty = c(1,1), lwd=c(2.5,2.5),col = c("black","red",

"blue"))

>

> #This will make our Data stationary.

> #I will choose the Log + first difference of the Data.

> par(mfrow=c(2,2))

> acf (transDif, lag = 400)

> pacf (transDif, lag = 400)

> dataPeriod <-spec.pgram(transDif, taper = 0, fast=FALSE, detrend=FALSE,demean

8. > library('forecast')

Loading required package: zoo

Attaching package: ‘zoo’

The following objects are masked from ‘package:base’:

as.Date, as.Date.numeric

Loading required package: timeDate

This is forecast 5.2

> library('astsa')

> library("FitAR")

Loading required package: lattice

Loading required package: leaps

Loading required package: ltsa

Loading required package: bestglm

Loading required package: lars

Loaded lars 1.2

Loading required package: ElemStatLearn

Attaching package: ‘FitAR’

The following object is masked from ‘package:forecast’:

BoxCox

>

> #I choose an ARIMA model, d = 0 since the data is already differenced.

>

> #Select the final model using ID Criterion

> auto.arima(transDif, max.p = 8, max.q = 8, stationary = TRUE, ic = c("aicc", "aic", "bic"), trace =

TRUE)

ARIMA(2,0,2) with non-zero mean : -439.6081

ARIMA(0,0,0) with non-zero mean : -390.096

ARIMA(1,0,0) with non-zero mean : -414.5041

ARIMA(0,0,1) with non-zero mean : -401.6552

ARIMA(1,0,2) with non-zero mean : -435.8972

ARIMA(3,0,2) with non-zero mean : -590.5202

ARIMA(3,0,1) with non-zero mean : -553.3992

ARIMA(3,0,3) with non-zero mean : -624.6525

ARIMA(4,0,4) with non-zero mean : -641.8194

ARIMA(4,0,4) with zero mean : -643.3304

ARIMA(3,0,4) with zero mean : 1e+20

ARIMA(5,0,4) with zero mean : -654.9737

ARIMA(5,0,3) with zero mean : -636.1066

9. ARIMA(5,0,5) with zero mean : -629.8412

ARIMA(4,0,3) with zero mean : -636.4764

ARIMA(6,0,5) with zero mean : 1e+20

ARIMA(5,0,4) with non-zero mean : -653.4301

ARIMA(6,0,4) with zero mean : 1e+20

Best model: ARIMA(5,0,4) with zero mean

Series: transDif

ARIMA(5,0,4) with zero mean

Coefficients:

ar1 ar2 ar3 ar4 ar5 ma1 ma2 ma3 ma4

-0.2040 1.0071 0.1723 -0.9667 -0.1743 -0.0248 -1.2324 -0.1158 0.8848

s.e. 0.0613 0.0171 0.0601 0.0152 0.0599 0.0335 0.0319 0.0293 0.0282

sigma^2 estimated as 0.008753: log likelihood=336.29

AIC=-652.58 AICc=-651.95 BIC=-613.78

>

> #My model is going to be of order (5,1,4)

>

>

> #Perform residual analysis, show that our model is good. Make sure our error is white noise.

> par(mfrow = c(4,2))

>

> #Plot of Residuals

> fit <- Arima(transDif, order = c(5,0,4))

> plot(fit$residual, type = "p")

>

> abline(h=0, col = "red")

>

> #Normally Distributed?

> hist(fit$residuals)

>

> #AutoCorrelations present?

> acf(fit$residuals)

> pacf(fit$residuals)

>

> #Are they Normal?

> qqnorm(fit$residuals)

>

> #Does the Test say it is a good fit?

> Box.test(fit$residuals, type = c("Ljung-Box"))

Box-Ljung test

data: fit$residuals

X-squared = 0.0056, df = 1, p-value = 0.9402

10. > LBQPlot(fit$residuals, lag.max = 30)

> mean(fit$res)

[1] -0.001070552

>

> #Smoothed periodgram of residuals

> k = kernel("modified.daniell", c(6,6))

> spec.pgram(fit$residuals, k, taper=0, detrend=FALSE, demean=TRUE, log="no")

>

>

> par(mfrow = c(2,1))

> #Plot Spec Density of the Final MOdel as well as the Smoothed

> finalModel <- fitted(fit)

> spec.pgram(finalModel, taper = 0, fast=FALSE, detrend=FALSE,demean =TRUE,log="no")

> k = kernel("modified.daniell", c(6,6))

> spec.pgram(finalModel, k, taper=0, detrend=FALSE, demean=TRUE, log="no")

>

> #Refit The final model

>

> refit <- Arima(Petro[1:348], order = c(5,1,4))

> pred <- predict(refit, n.ahead = 12, d =1)

> pred$pred

Time Series:

Start = 349

End = 360

Frequency = 1

[1] 96.98064 96.96685 94.07727 82.66665 75.30919 63.93817 59.73830 59.37145 62.29238 72.78900

79.44755 90.20105

> pred$pred + pred$se

Time Series:

Start = 349

End = 360

Frequency = 1

[1] 109.44587 112.64558 111.26915 100.66319 93.42068 82.07828 77.88662 77.55500 80.87230

92.11042 100.52580 113.21682

> forePlus <- c(109.44587, 112.64558 ,111.26915 ,100.66319 , 93.42068 , 82.07828 , 77.88662,

77.55500, 80.87230 , 92.11042 ,100.52580, 113.21682)

>

> pred$pred - pred$se

Time Series:

Start = 349

End = 360

Frequency = 1

[1] 84.51540 81.28813 76.88539 64.67011 57.19769 45.79806 41.58997 41.18790 43.71247 53.46758

58.36930 67.18528

> foreMins <- c(84.51540, 81.28813, 76.88539, 64.67011, 57.19769, 45.79806, 41.58997 ,41.18790,

43.71247, 53.46758 ,58.36930 ,67.18528)

>

> index <- c(348:359)

> fore <- c(96.98064 ,96.96685, 94.07727, 82.66665, 75.30919, 63.93817, 59.73830, 59.37145,

11. 62.29238, 72.78900, 79.44755, 90.20105)

> par(mfrow=c(2,1))

> which.max(fore)

[1] 1

>

> par(mfrow = c(1,1))

>

> plot(Petro[348:359]~index, type = 'l', col = 'black', main = 'Plot of Forecasted and Observed Values',

xlab = "Time", ylab = "Petrolium Consumption", ylim = c(35,130))

> lines(fore~index, col = "red")

> lines(forePlus~index, col = "blue")

> lines(foreMins~index, col = "blue")

> legend(348,130, c("Observed","Predicted", "Prediction Bands"), lty = c(1,1), lwd=c(2.5,2.5),col =

c("black","red", "blue"))