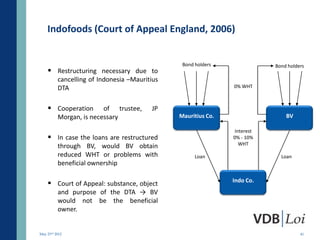

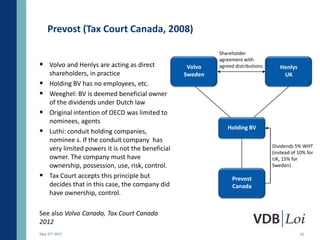

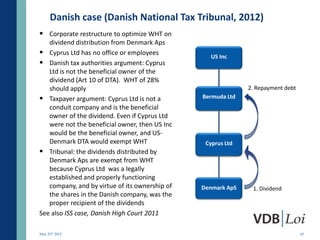

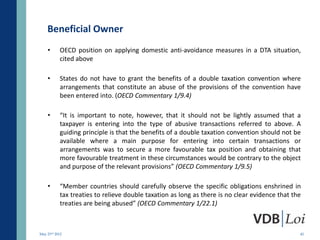

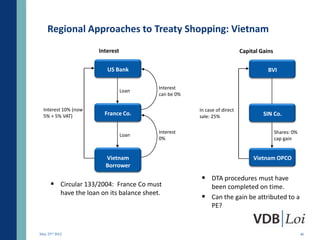

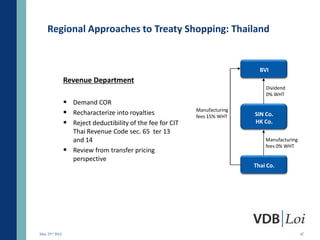

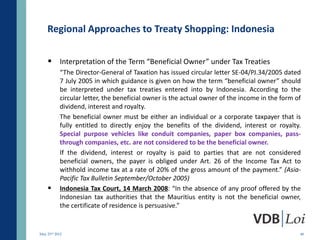

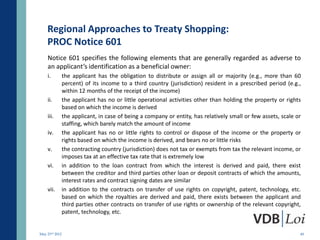

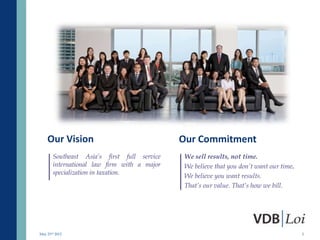

This document summarizes a presentation given by a Southeast Asian law firm specializing in taxation. The firm operates across 4 countries in Southeast Asia, employing over 40 staff including 4 partners. The firm provides tax advisory, legal advisory, government relations, and compliance & accounting services. The partners and advisers have extensive experience with major projects across the region involving taxation, mergers & acquisitions, corporate finance, and real estate.

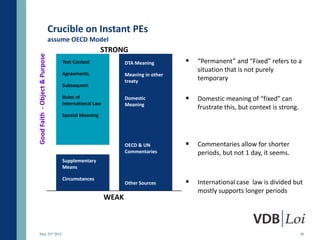

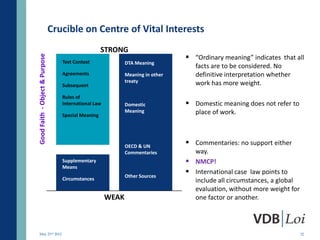

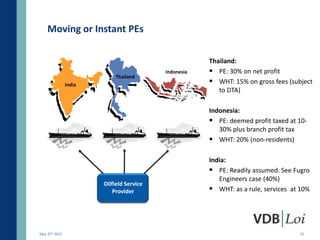

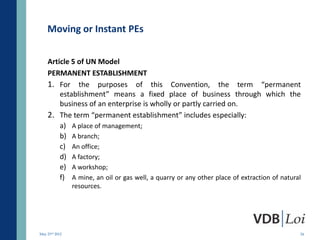

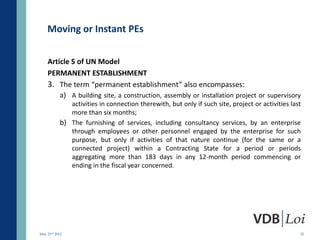

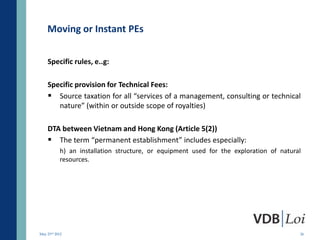

![Moving or Instant PEs

Key approaches:

1. Physical PE – how long is long enough?

2. Furnishing of Services PE

“The furnishing of services, including consultancy services, by a resident of one of the

Contracting States through employees or other personnel, provided activities of that nature

continue (for the same or a connected project) within the other Contracting State for a period

or periods aggregating more than six months[1] within any twelve-month period”.

3. Art. 3 (2)

a. “Fixed”

b. “Place of business”

c. “Permanent”

4. OECD and UN Commentary

a. A PE may not be purely temporary

b. Special type of activity?

“A place of business may, however, constitute a permanent establishment even though it

exists, in practice, only for a very short period of time because the nature of the business is

such that it will only be carried on for that short period of time. It is sometimes difficult to

determine whether this is the case” (OECD Commentary 5/6).

May 23rd 2012 27](https://image.slidesharecdn.com/casestudiesintaxtreatyinterpretationpostfinal-13454685372029-phpapp01-120820081650-phpapp01/85/Case-Studies-In-Tax-Treaty-Interpretation-Post-Final-27-320.jpg)