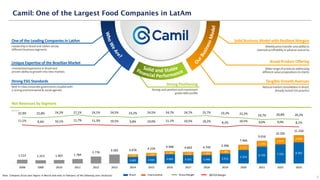

The document presents the financial results of Camil Alimentos S.A. for May 2024, detailing its compliance with international financial standards and highlighting its consolidated results. It describes Camil as one of the largest food companies in Latin America, emphasizing its diversified product offerings and strong market position across various segments. Additionally, the document contains forward-looking statements regarding future performance, which may differ due to various risks and uncertainties.