Download to read offline

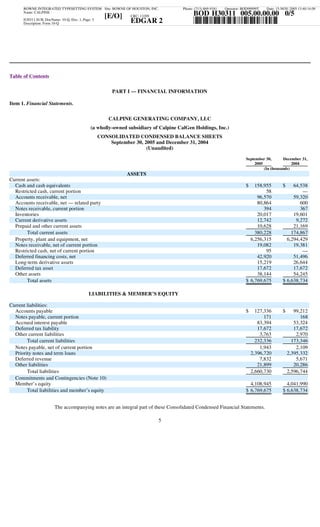

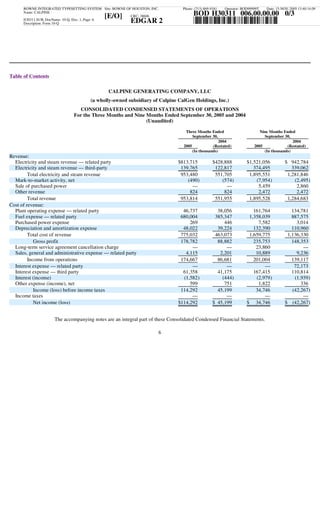

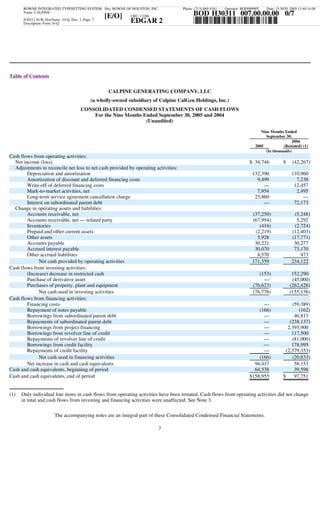

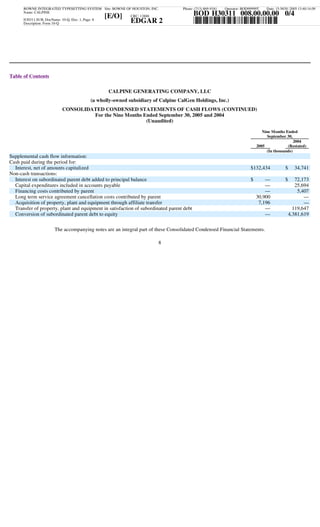

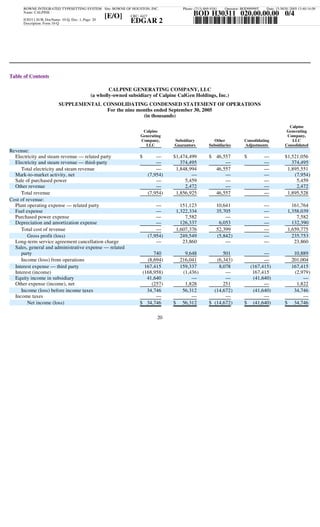

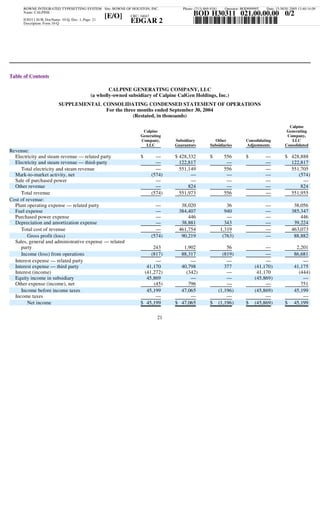

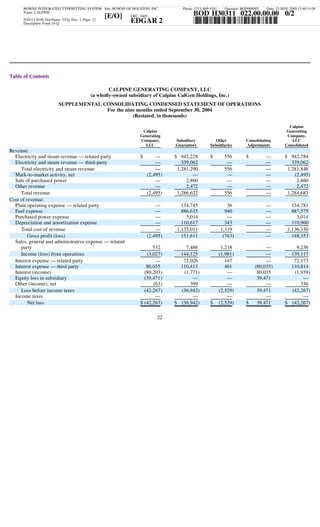

This document is a Form 10-Q quarterly report filed with the SEC by Calpine Generating Company, LLC. It includes an unaudited consolidated condensed balance sheet comparing assets and liabilities as of September 30, 2005 to December 31, 2004, as well as unaudited consolidated condensed statements of operations and cash flows for the three and nine month periods ended September 30, 2005 and 2004. The document also includes notes to the financial statements and sections for management's discussion of financial condition and results of operations, market risk, controls and procedures, legal proceedings, and certifications.