Downloaded 948 times

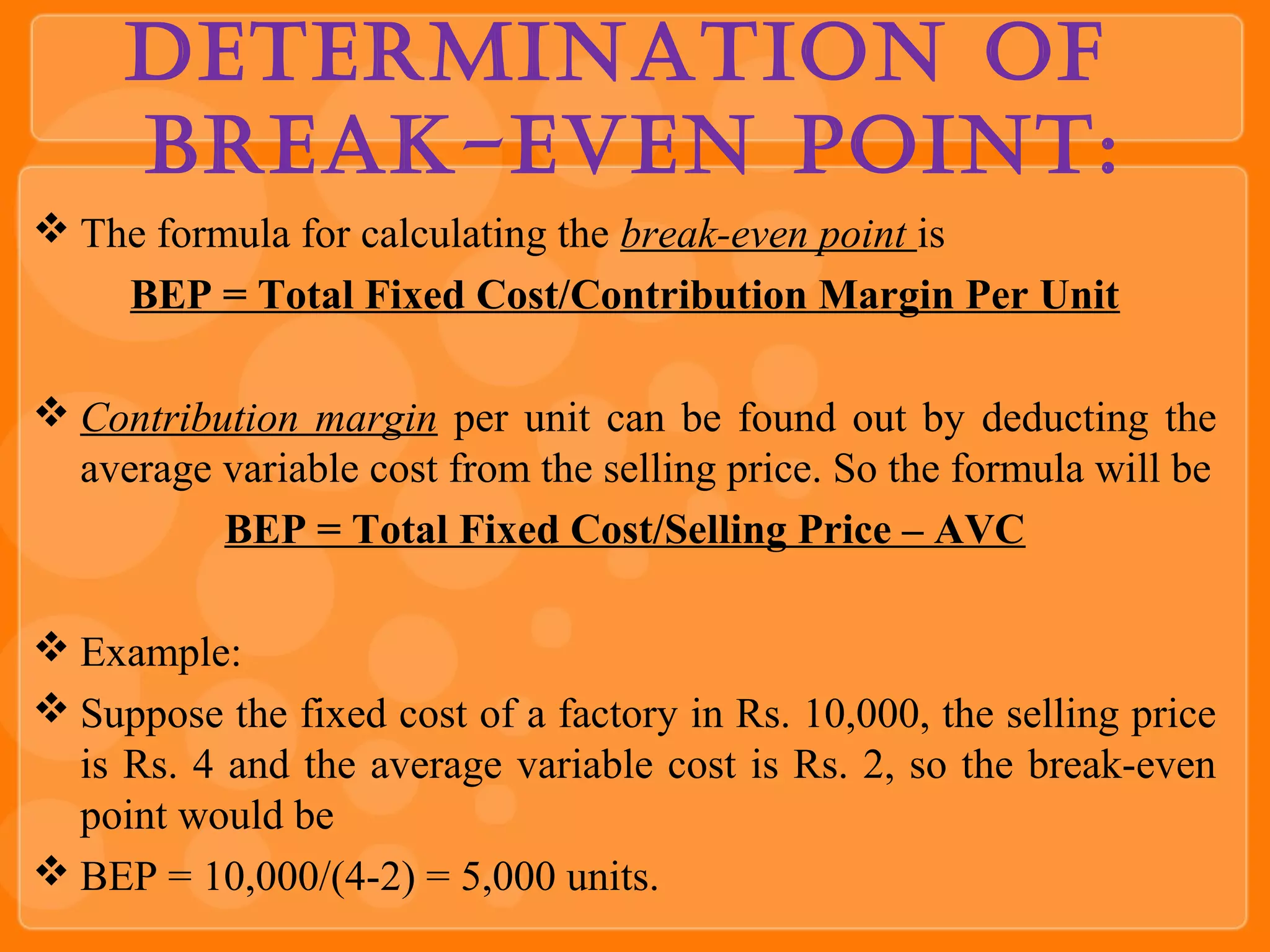

The document discusses break-even analysis, which determines the sales volume needed for a company to cover its total costs. It defines break-even point as the sales level where total revenue equals total costs, resulting in no profit or loss. The document provides examples of calculating break-even point using tables and charts. It also outlines the assumptions and limitations of break-even analysis, and explains its uses for management decision making like determining a target profit level or the effect of a price change.